|

Interested in learning techniques that will virtually guarantee you success, regardless of your field of interest? Of course you are!

On that front, todays show will not disappoint! Brandon and David interview bestselling author Robert Greene, whose latest book is titledThe Laws of Human Nature. Robert discusses brilliant concepts regarding earning the trust of others, determining who you can trust in an interaction, and developing the super power of reading other peoples non-verbal cues. He also shares valuable insight that will help you positively impact the emotions of others around you, put yourself in a peak state of performance, and activate the power of your own emotional connection to things you are passionate about. And do not miss Roberts advice on making sure others cannot manipulate or deceive you, or what hes learned studying Leonardo da Vinci and others who have mastered their crafts! If you want to become the investor who gets deals first, gets the best prices on rehabs, and is less likely to be fooled in a transaction, download this episode right now! Click hereto listen on iTunes. Listen to the Podcast HerePodcast: Play in new window | Download Subscribe: Apple Podcasts | Android | RSS Watch the Podcast Here [embedded content] Help Us Out! Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it! This Show Sponsored By  Fundriseenables you to invest in high-quality, high-potential private market real estate projects. Im talking anything from high rises in D.C. to multi-families in L.A. institutional-quality stuff. And each project is carefully vetted and actively managed by Fundrises team of real estate pros. Fundriseenables you to invest in high-quality, high-potential private market real estate projects. Im talking anything from high rises in D.C. to multi-families in L.A. institutional-quality stuff. And each project is carefully vetted and actively managed by Fundrises team of real estate pros.Their high-tech, low-cost online platform lets you track the progress of every single project, and keep more of the money you make. Oh, and by the way, you dont have to be accredited. VisitFundrise.com/biggerpocketsto have your first 3 months of fees waived. Deep Dive Sponsor  If youve been thinking about getting a SimpliSafe Home Security System, but have been If youve been thinking about getting a SimpliSafe Home Security System, but have beenwaiting for the holidays when all the tech deals come outyouve made a smart move! If you go to SimpliSafe.com/biggerpocketsyoull get 25% off any new system. Thats an amazing deal. They rarely do anything like this but theyre doing it just for us! Fire Round Sponsor Blinkist has a special offer for YOU. Its a FREE 7 day trial just go toBlinkist.com/pockets In This Episode We Cover:Roberts mentor-mentee relationship with Ryan HolidayWhat a mentor is looking for a menteeWhat are the laws of human natureUnderstanding human nature and why its the most important skillSeeing through people beyond the surfaceValidating the good in peopleFlattery vs. recognizing somebodys strengthThe different biases and how were governed by emotions Conviction bias Appearance bias Group biasTechniques to resist these biasesHow to present yourselfMastery and being emotionally connected to what you doAnd SO much more!Links from the ShowBooks Mentioned in this ShowTweetable Topics:The most important thing you are looking for is not a glittering resume, its not charm, but their character. (Tweet This!)The most important skill you can develop in life is understanding people. (Tweet This!)The energy that you present people, is how theyre going to see you.(Tweet This!)Connect with Robert https://www.biggerpockets.com/renewsblog/biggerpockets-podcast-315-read-human-nature-succeed-life-robert-greene/

0 Comments

Due diligence may be boring, but its absolutely critical to get it right.

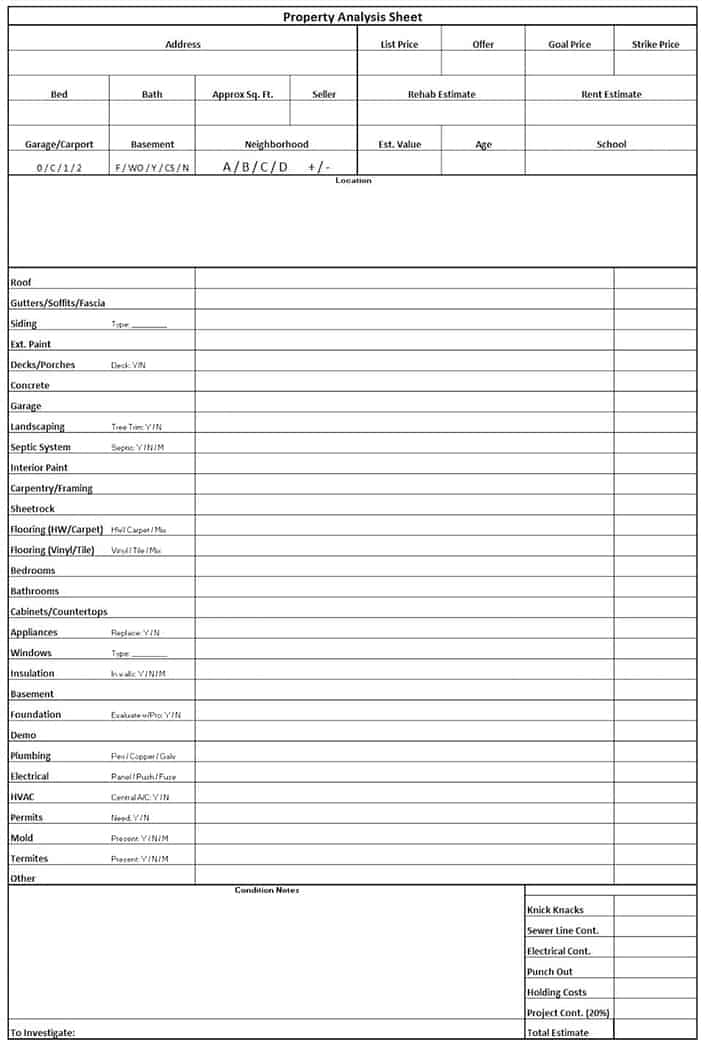

Here well take a deep dive into what is perhaps the least fun but most indispensable part of real estate investing: the dreaded due diligence. What Is the Meaning of Due Diligence? While an entire book could be written on all the ins and outs of this subject, the definition ofdue diligence is rather simple. Its the investigation or audit of a potential investment or product to confirm all facts, according to Investopedia. Basically, the purpose of performing due diligence in real estate is to confirm what you believed to be true about a property when you got it under contract. While it can be arduous, following the steps outlined below will help you avoid any unwanted surprises and greatly increase your confidence in the investment. And what do new investors need more than confidence? Checklist: The Process Performing due diligence can be broken down into several distinct stages. Pre-Offer Due DiligenceArea AnalysisValue and Financial EstimateRehab EstimatePost-Acceptance Due DiligencePhysical Due DiligenceFinancial Due DiligenceLegal Due DiligenceInspectionsRetrading (if necessary)Final Decision and Walking Away (if necessary) Use this as your due diligence checklist. Make sure you never to skip a step! Note that while there are differences in how to approach houses and apartments (as well as commercial), the fundamentals are the same. Lets take a closer look at each part. Pre-Offer Due DiligenceArea Analysis Before any analysis of value should be done, you want to make sure the area youre looking to invest in meets your criteria. Some of the most important things to consider are: Crime RateMedian IncomeOccupancy RatesPopulation GrowthSchool Rankings People generally want to avoid high crime areas, and families are extremely particular about which school district the home is in. If you intend to invest in low-income housing, thats one thing. (In my opinion, newbies shouldshy away from this sort of investment.) Regardless, you should know what you are getting into before you buy. Fortunately, there are some very good free sources you can look to for information (in addition to just talking to people in the neighborhood). City-Data.com and CLRSearch.com are good for demographics, and GreatSchools.org can help you evaluate the school district. There are also more advanced, albeit expensive, tools available. Value and Financial Estimate The next step is to determine a propertys after repair value (ARV). This is best done by looking at comparable sales. I wont go into too much detail here, but a wealth of ARV guidance is available on BiggerPockets. Related:The Ultimate Guide to Quickly Estimating a Propertys ARV (After Repair Value) You will also want to make sure the property will cash flow by creating a pro forma. This is particularly true for multifamily properties but is helpful for houses, too. Review the actual financials of those properties (particularly the T-12 operating statement) as seller-provided pro formas (future estimate) are almost always too optimistic. The best way to create your own pro forma is to base it off the propertys actual performance. With regard to pro formas (at least for apartments), you will have three income categories and 10 expense categories: Income ItemsGross Rental IncomeOther Income (i.e., laundry, utility chargebacks, late fees, etc.)Vacancy Loss (include both vacant units and economic vacancy)Expense ItemsProperty TaxesInsuranceUtilitiesManagement FeeRepairs and MaintenanceContract Services (i.e., lawn care, snow removal, etc.)General Administration (i.e., phone lines, eviction processing, etc.)MarketingPayroll (for larger properties with on-site staff)Recurring Capital Improvements (i.e., roof replacement, HVAC replacement, etc.) Related:Building a Pro Forma: an Essential Skill for Real Estate Investors After subtracting the gross expenses from the gross income, you will get the net operating income. From this, you subtract any debt service you expect to have in order to come up with the anticipated cash flow. It should also be noted that, with apartments and commercial properties, you will use the cap rate to compare to other recent sales. Why? Because it is usually too difficult to find properties that are similar enough for a direct comparison. More on cap rates and other financial calculations can be found here: AGuide to Internal Rate of Return & Other Must-Know Financial Metrics. Overall, your pro forma will look something like this:  Finally, youll want to evaluate the rent. Rentometer.com is a good place to start but shouldnt be relied upon exclusively. In addition,RentRange.com offers helpful reports for a reasonable fee. But Ive found the best way to assess rent is to look at the map feature on Craigslist or Trulia for similar properties that are for rent in the area. Calling the numbers listed on lawn signs of nearby rentals or asking neighbors what they pay can also help. Rehab Estimate There are simply not enough hours in the day, nor days in the year, to do a thorough inspection of every property you make an offer on. That being said, throwing out blind offers is usually a big waste of the sellers time, as well as yours. What you want is a down and dirty sort of due diligence pre-offer. The question to ask is, roughly speaking, what is the general condition and an approximation of the required repairs for this property? For this, I designed a one-page estimation sheet based on J. ScottsThe Book on Estimating Rehab Costs. Typical rehab expenses are broken into 25 categories; however, I added a 26th by splitting the foundation from the basement. Here is what my sheet looks like:  As you can see, when I initially go through a house, I make a quick estimate of all the repairs required for each major category. (For apartments, depending on the size, I will either use several sheets, or for something over four units, take broader notes about the general condition.) Then, I add a little bit for the knickknacks, estimate the holding costs (which are often forgotten), and throw in a 20 percent contingency for unforeseen expenses. (If the electrical looks questionable or the property is older, I may throw in an additional contingency for the electric and/or sewer line.) I should stress that this is not the only way to do this. There arent any real estate dictionaries that define due diligence by laying out the perfect method to go about it. For example, J. Scott doesnt add a broad contingency.Instead, for each line item, he rounds his estimate up to either the next $100 or next $500 (depending on how big the expense is). The important part is to get the basic idea of due diligence and create a system that works for you. Then, use that system every time to the T. Key Things to Look for When Estimating Rehab Costs There are a lot of things to look for when doing your initial (as well as post-contract) walkthrough. The first thing is to simply get a good feel for the property. Would you grade it as being close to rent ready or bulldozer bait? Maybe somewhere in between? You should always note a propertys general condition. More specifically, the following items should be on your radar: Furnace and A/C:Are they old or rusty?Fuse Box:These really need to be replaced with an electric panel.     Ungrounded Electrical Outlets:You can use a plug tester from Home Depot or Lowes to test for this.Plumbing Leaks:Run the water, check each of the faucets, and look in the basement (if accessible).Galvanized Plumbing:Lookout for steel pipes, which have a tendency to rust.Foundation Cracks:These could be signs of bad grading or roots pushing on the wall and should be epoxied and likely shored up with braces.  Foundation Movement:Anything over four inches should probably be braced or have dead men added. Much more than that and the wall might need to be pushed back, which is very expensive. (Pro tip: If you cant tell how much the wall has moved, go outside and run you finger along the bottom of the siding. It should go about to your knuckle. But just running it along the foundation wall should give you an idea of where and how much the wall has moved.)Mold:This usually occurs in the basement. Also look for the bottom half of the drywall missing (like in the second picture below). This virtually always means mold was torn out. Mold isnt hard to remove, but the key is to find out where water is getting in so new mold doesnt grow back. This could be easy or very difficult, depending on the house.   Roof Leaks or Damage:It will be hard to tell if the roof leaks unless its raining, but you can see damage by getting on the roof. How many layers are there? More than one is a problem. Check from a side view, too. If the edges of shingles are lipping up, that means the roofs old and on borrowed time. If you see what look like small, discolored impact craters on it and granules are missing, thats probably hail damage.  Help With Estimating Rehab Costs Unfortunately, learning how to estimate rehab costs isnt an easy thing to do. And doubly unfortunate, the best way to learn is through experience. Ive found that comparing the costs of previous projects that were of equivalent size is the best way to get a feel for the costs of upcoming projects. This goes for individual expenses, too, like gutting a bathroom. Newbies dont have this luxury, though. In the meantime, one of the best alternatives to experience is to use contractor bids to get an idea of various costs. For instance, a standard toilet is around $150 and a standard medicine cabinet will cost around $100. Youll start to learn this as you look at more and more bids. You can ask a contractor to give a you bid up front, and many will do so. But dont abuse this privilegetheyll quickly stop returning your calls if they dont get any actual work from you. You can also ask seasoned investors to share their thoughts. (Maybe offer them a free lunch for it.) Plus, J. Scott has some good tips in his previously mentioned book. There are also websites like HomeAdvisor.com that can helpalthough their estimates should be taken with a grain of salt. Post-Acceptance Due Diligence When people think of due diligences meaning, this is what they really think of. Post-acceptance due diligence is when the rubber hits the (very tedious) road. First and foremost, its critical to understand the timetable youre under, which depends on whats in the purchase and sales agreement. Every contract is negotiable, but most residential contracts have a 30-day period to close and will allow 15 days for inspections before your earnest money goes hard (is no longer refundable). With most contracts for apartments and other commercial properties, there is a 30-day inspection period and the close is in 60 days. However, its possible to add a clause that extends the contract an additional 30 days with another earnest money payment, just in case. I would recommend adding something like that, particularly for larger transactions. You can always ask for extensions if something comes up during your due diligence (although you may not receive them without a clause like the one mentioned above). The critical thing is to know exactly what the contract says so you can plan your due diligence accordingly. Physical Due Diligence First things first. When you walk a property, walk all of it. As I mentioned in a previous article on apartment due diligence, Many sellers and even some real estate agents will tell you its OK to walk every second or third unit. Ignore this advice with extreme prejudice. If you only view every other unit, do you think the seller will show you the best or the worst units? How many hidden problems are you leaving behind closed doors, only to find out later once the property is in your name? It is critical to know the condition of each unit, even if there are 100 of them. In order to do this properly, you will need to turn the utilities on if they are currently off. This is not always possible (say, if the copper was stolen out of the basement). In those cases, make sure to add an extra contingency in your rehab budget to protect yourself from unknowns. When going through a house, I use the following sheet to put together a detailed scope of work that includes every line item I believe will need to be done. The document is six pages in its entirety, but heres the gist:  I then transcribe these items and budget them individually using a spreadsheet program designed for project management. It ends up looking like this:  I break out the categories into four major subheadings: Pre-Construction Work: Work that must be done before the main work can start (i.e., removing trash or repairing electrical issues).Construction:Everything you plan on having done by the main contractor.Vendors:Anything that will be done by a vendor other than the main contractor (i.e., painting, flooring, plumbing, etc.).Punchout:Last items to be done to button up the property (i.e., install appliances, put up blinds, install outlet covers, etc.). I recommend taking pictures of each issue. The project management software I use (called Smartsheet) even allows you to attach the photos to that items cell within the spreadsheet. This way, I dont have to be there when each contractor goes through to create a bid. I can show them photos of the issue instead. Heres an example of a picture I attached to a line item called Replace supply vent white.  Once you have a detailed scope of the work thats needed, its a good time to re-assess your rehab estimate. Budgeting for each line item provides a much fuller picture of the costs. Then, you can compare the new budget to the previous quick and dirty estimate to double-check whether it was right. And with the property under contract and a line-item scope, you can ask a contractor to get a full bid for you to verify your estimate. I must once again emphasize that there is no perfect way to do this. For example, if the contractor will do all the work, you wont need a vendor list. But the method Ive described fits within a general outline of an effective system. Amend it to fit your own needs and follow it dutifully. Now, returning to the walkthrough, you should also evaluate anything you questioned during your original pre-offer walkthrough and make sure it is up to snuff. This likely requires paying for professional inspections (discussed below). Finally, evaluate the tenants, if there are any. If you encounter a lot of meeth (what I call meth teeth), thats something to be concerned about. If the house or several units of a property have been treated horribly by the tenant, you can surmise the quality of that tenant quite easily. For apartments, I also recommend driving by at night to see if it looks safe and tranquil or more akin to a war zone. Heres a tenant watching example of properdue diligence that comes to mind. Once, a friend of mine was walking a fourplex just before the close. He got into a conversation with a neighbor about the property, and it turned out she had a lot to complain about! Most notable amongst her complaints was that shed gathered many of the tenants were drug dealers and prostitutes. Needless to say, my friend walked away from that deal. The key takeaway? Yes, talking to tenants and neighbors is a good idea. The seller will usually not want you to mention you are buying the property, but you can ask broad questions like, How do you like it here? Or say, Have you had any maintenance problems? Financial Due Diligence Just as important as the physical due diligence is the financial due diligence. This is especially true of apartments and commercial properties, but it is also something you should look for with occupied houses. Sometimes, a seller wont provide some or all of the financials on a property until after its under contract. The seller is all but begging for you to retrade in these cases (discussed below), but you should absolutely demand the financials once the property is under contract. When you receive them, go through them with a fine-tooth comb. The key documents you will want are: T-12 Operating Statement:Minimally for the past 12 monthsparticularly for apartmentsbut preferably for the last three years.Current Rent RollAged Receivables Report:A list of whos behind on their rent and by how much.List of Recent Capital Improvements There are two major things to watch out for when reviewing financials, specifically with larger properties: Bad DebtsMisallocated Capital Expenses If a property uses accrual accounting, then it is deemed that all the rents are received until the bad debts (rent not collected) are charged off. Make sure that all the debts have been charged off when reviewing financials and you arent looking at phantom income. The bigger problem Ive found, however, is misallocated capital expenses. Many owners will put operating expenses (i.e., maintenance, turnovers, etc.) under capital expenses so they dont show up on the operating statement. This makes the propertys performance look a lot better than it actually is. For this reason, I plead with new investors to consider recurring capital expenses (usually called replacement reserves by banks) as a line item on their pro formas. Yes, you only need to replace the roof once every 30 years or so, but you should understand such costs are an ongoing part of owning the property. Make sure to demand a list of all the owners capital improvements in the last year (or, even better, the last three years) and their costs. Unless they were genuinely upgrading the property (i.e., installed central air when it previously had window units) or were rehabbing an underperforming property, these expenses should be considered recurring capital expenses and included as part of the profit and loss statement. Many a time I have had to reconstruct a sellers operating statement from the various pieces theyve provided (which are often poorly kept in the first place). Its no fun, but it isessential! When performing due diligence, youll also want to get a copy of each lease thats currently in place. Make sure to demand this immediately upon getting the property under contractsellers notoriously drag their feet. Youll want to carefully look at the following: Rent: Make sure its the same amount listed on the rent roll.Type:Month-to-month or a year-long lease? When does that lease end?Deposit:Again, make sure its the same as what the rent roll says.Utilities:Who is responsible for paying what?Pets:Do tenants have them? Is there pet rent?Late Fee:When is it applied, and how much?Special or Odd Arrangement:Do any tenants get a discount for doing maintenance or something similar? If youre under contract on a commercial property (office, retail, or industrial), you should also get anestoppel certificate. An estoppel certificate goes to the tenants of the building and asks them to confirm the rent, deposit, and other terms of the lease. With commercial properties, you usually only have a couple of big tenants who often have long leases, so its very important to know exactly what the terms of the agreement are. One final note is that, oftentimesparticularly with housesthere wont be much (if any) financial due diligence to do. If its a vacant, bank-owned house for example, there wont be any documentation to review. In those cases, just double-check your area, rent, and ARV analysis, and move on. Legal Due Diligence Lets start by discussing homeowner associations (HOAs). Many houses and all condos have HOAs, and you will want to review their bylaws to make sure theyre in accord with your plans. In the case of condos, you will also want to make sure the HOA has sufficient money in reserve for capital improvements. If they dont, the association can impose a special assessment and charge owners a portion of the cost to cover repairs. Key things to look for in the HOA bylaws include verifying that the HOA fee is what the seller says; checking that there arent restrictions on pets or other such things; and, most importantly, ensuring that you are actually allowed to rent out the property. I once bought a condo in an HOA that didnt allow renters. I had requested the bylaws but never received them and foolishly forgot to follow up. We had to flip that one and made a healthy profit of $1,700. (HOA fees can eat up profits like you wouldnt believe.) Another consideration: is the property odd in some way? For example, is it a house that was converted into a duplex? If the property is odd, you will want to verify that it is legally permitted. Ask if conversions were done legally. If not, it may be grandfathered in and considered legal nonconforming. This classification shouldnt necessarily be a deal breaker, but it can come with added restrictions and/or decrease resale value. Laws vary by region. In Independence, Mo., for example, any legal non-conforming unit can continue to be rented unless it sits vacant for six months, at which point it can no longer be rented. If you intend to add more units or convert the property (say, from residential to commercial), check to make sure the property is zoned correctly or whether it can likely be rezoned. This may require a trip to the zoning department. In addition, verify property taxes with the county. Usually you can do this on the countys website. Finally, it is critical to always close with a lawyer or title company. They will run a title report to make sure you are getting a clear titlenot picking up some random mortgage or mechanics lien from way back when. If a lien is overlooked, title insurance will pick up the tab so you dont have to. Again, there is no gray area here. ALWAYS close with an attorney or title company, no matter what. Inspections If youre just starting out, in my opinion, always get a property inspection. Even seasoned investors would be wise to get them. Property inspections can be a bore to read, but go through each point anyway. An inspection will look something like this:  Some issues, like the above, are rather small. Others, like the one below, definitely need to be addressed.  You shouldnt rely entirely on an inspector either. As mentioned earlier, thoroughly walk through the property yourself, as well. But inspectors can certainly catch things you missed and will generally know a lot more about building and safety requirements than you. Furthermore, inspections can be used to verify your rehab expectations, realize you need to look deeper into something, or be used for retrading. Many buyers demand a seller fix all or some of the problems an inspection brings to light before they are willing to close. Additional inspections you may want to consider, depending on the property, include: Lead, Asbestos and Radon Inspections:Lead inspections are only necessary if the property was built prior to 1978.Termite Inspection:Particularly if you see signs of termite damage, like damaged joists or mud tunnels.   Roof Inspection:If the roof is older, appears damaged, or you arent sure about it.Phase One: Environmental survey required for apartments and commercial properties.ALTA Survey:Usually for larger properties with unclear easements, boundaries, etc. Unsure of something? Ask a specialist. For example, you could ask an HVAC technician to look at the furnace in a property if youre unsure of its condition. Lastly, get the sewer line scoped on any property over 30 years old. Replacing a sewer line can be an expensive proposition (usually over $4,000), so you want to find out whether the line has collapsed or is ridden with roots. You should be able to get a plumber to scope it for around $200.Make sure to view it with them. Some will try to convince you to replace a line just because there are a few roots in it. However, these lines can be snaked out. Either way, you want to know what youre dealing with ahead of time. Youre not going to win the adoration of any tenants if they have raw sewage back up into their home. When Is Retrading Necessary? There are two major reasons for due diligence. The first is to make sure the property is what you thought it was. The second is to give you the chance to renegotiate if its not. With due diligence, real estate is not only safer but also more profitable. For larger deals, I like to list my assumptions up front. Examples of assumptions might be that approximately 90% of tenants are paying, the HVAC is in pretty good working order, the roof needs to be replaced, and so on. By documenting this, if assumptions are proven inaccurate when performing due diligence, they can be referenced when asking for a price reduction. But even without such a list, you can always ask for a price reduction or amend other terms if you find something amiss. Remember, everything is negotiable. Aside from a price discount, problems discovered during due diligence might be resolved by asking for certain issues to be fixed, asking for financing, asking to extend the closing or inspection period, or some other way. That being said, you shouldnt plan on retrading from the get-go or retrade over something trivial. If you do, youll quickly get a reputation and sellers will be less likely to want to do business with you. Final Decision and When to Walk Away When all the hay is in the barn (as my old football coach would say), I like to play devils advocate. I do this right before the inspection period expires, and I only do it for larger acquisitions. But Id recommend that newbies definitely consider iteven for a house! The problem were often fighting is our own confirmation bias. The tendency is to want to be consistentor to simply be right. If you have thought the deal makes sense from the beginning, you may ignore contrary evidence to maintain your initial belief. To fight this tendency, I make the best case I can to not go through with the deal.Remember, the person who usually wins a negotiation is the one whos willing to walk away. Always be willing to walk away, and never become emotionally attached to a property. At the end of the day, its just an investment. No one becomes emotionally attached to their GE stock. (I hope.) And despite being under contract, until the ink is dry on the settlement statement and the deal is funded, youre still in negotiations. Summary of the Process Some parts of real estate investing are a lot of fun. Some arent. Due diligence requires time, effort, and attention to detailbut its absolutely worth it. Not only will it save you from costly mistakes, but it will also provide you with opportunities to get even better deals. Furthermore, many new investors struggle with confidence and are scared to death going into their first deal. Knowing how to perform thorough due diligence can alleviate much of that fear. Nothing is entirely certain in real estate investing (or life!), but due diligence can provide a much higher level of assurance.  Do you have anything to add about due diligence?Or would you like copies of any of the documents Ive referenced? Id be happy to share! Comment below. https://www.biggerpockets.com/renewsblog/due-diligence-ultimate-guide Whether youre buying or selling vacation rental real estate, success often comes down to good seasonal timing. There are benefits to buying and selling across all times of the year. Identifying the economic conditions and seasonal considerations that best align with your goals will help you know when its the right time to make your move.

Knowing When the Markets Right Determining the right economic conditions to buy or sell a vacation rental depends on your motivations. For example, its common to see a rush of investor and cash buyers step up activity during periods of residential slowdown. As a seller of a vacation home, you stand a good chance of beating a national residential buyers marketespecially if you market your homes cap rate and revenue potential. Unlike with their primary homes, buyers planning to finance a second home might see a silver lining to a spike in interest rates. Financial institutions seeking to balance a dip in mortgages may decide to offer better HELOC and home refinancing options to broaden their customer base. Familiarizing yourself with vacation rental-specific market trends can help you decide if the time is right to buy or sell. After determining that market conditions are trending in your favorand even if theyre not but youve decided to forge aheadits time to consider the impact of seasonality.  Related: 7 Tips for Financing Your First Vacation Rental Property Buying Before Peak Season When shopping for a home thats in good condition in a high-traffic market, its a good idea to close before peak season. Youll have the opportunity to purchase and receive advance deposits at the closing table for reservations already on the books. Since you didnt have any expenses generating the bookings, thats like money in your pocket. But all those free bookings come with a cost: Youre less likely to negotiate a discount on the purchase price. Buying before peak season brings the benefit of a lot of guests on the books, but those guests are expecting the home to come furnished as listed. And you likely wont have a lot of time to decorate. To avoid poor reviews, try to purchase furnished (unless your furniture is a major upgrade and you can get it all into the home in time). Selling Before Peak Season Most buyers looking to close prior to peak season want to see reservations on the books. Having a backlog of reservations gives them a revenue-driving window to get acquainted with the property management company and get settled. It also gives you more negotiation power. Selling before peak season leads to a likely higher purchase price since you paid to get all those bookings and revenue in place. Since buyer demand tends to peak right before peak season, you will likely get to negotiate more than just price. Closing times, closing costs, financing terms, etc. are all on the table. Youre also likely to be able to sell the home fully furnished, which is typically in the buyers best interest as well. Related: Does Your Vacation Home Qualify for a 1031 Exchange? Heres What Tax Code Says Buying After Peak Season If youre willing to buy a home that needs work, it can pay to wait until after peak season. With fewer guests on the books, youll have time to conquer all those updates that will increase revenue during peak season. You also wont feel the same pressure to purchase furnished as you would when buying prior to peak season. In most markets, buying after peak season improves your ability to negotiate a better purchase price. But you will need to start marketing the property quickly to ensure you get maximum bookings prior to peak season, so the pressure is on to get the property in rentable condition and advertised to guests. One often under-looked benefit to buying after peak season is that its easier for you to compare more properties, because there arent any guests staying in them. Youd be surprised how difficult it can be for realtors to find time to show great vacation homes because theyre booked so far out.  Selling After Peak Season The major benefit to selling after peak season is that the unit will have more availability for you to give it a facelift. With fewer bookings to work around, you can make any necessary updates and repairs to get the property in great selling condition. Lower guest occupancy means it will be easier to show the property and encourage potential buyers to stay there. As peak season slows, purchase prices tend to drop. With fewer reservations on the books, you have less power to negotiate. Sellers who can use this time to make upgrades and sell prior to peak season tend to command higher purchase prices. That said, were seeing an occupancy trend in many markets (especially mountain markets) where seasonality matters less to guests, meaning down season is becoming a thing of the past and its always a good time to sell. Whether youre looking to buy or sell a vacation rental, timing is everythingand the right timing is unique to every buyer and sellers situation. While this post covered some basic considerations to keep top-of-mind when deciding if the time is right to buy or sell a vacation home, its by no means comprehensive. When youre serious about taking the next step, find a vacation real estate expert who can share insights about regional and market-specific nuances. Do you have experience buying and selling vacation rentals? How have you found time of year affects the process? Comment below! https://www.biggerpockets.com/renewsblog/times-year-buying-selling-vacation-rental/ Unless you live under a rock, you know all too well that there is an affordable housing crisis underway. And indications are that it is going to get worse before it gets better. I recently ran across some stats that paint a pretty dismal picture. One study estimates well need an additional4.6 million new apartment unitsby 2030. This equates to 325,000 new apartments needed annually to keep up with demand. Unfortunately, the number of new apartments projected to come online is about 70% of what is needed. Add to that an already low supply of affordable units and minimal government incentives, and weve got an ever-widening affordability gap.

However, as is often the case, where there are challenges, there are also opportunities. The affordable housing shortage presents not only opportunities for good investments, but also the opportunity to make an impact (that is, investments that will make you money and do good socially and environmentally). If you have a genuine concern about the affordable housing crisis and want to be a part of the solution, read on. Here are four ideas on ways real estate investors can help alleviate the affordable housing crisisand make money in the process. 4 Ways Investors Can Help Alleviate the Affordable Housing Crisis1. Crowdfunding Real estate crowdfunding is relatively new but gaining in popularity. Most readers of this article are likely to think of direct investment when it comes to real estatebuying a property ourselves to do a fix and flip or long-term rental, or investing in a specific project via private money loans. But most of us are limited in the number of projects we can invest in at any one time. Crowdfunding expands the reach of individual investors and opens real estate investing to a much broader range of individuals. Some platforms have minimum investments as low as five dollars. With crowdfunding, the investor can often specifically invest in projects that will bring more affordable housing online. So, even though you may not have the funds to fix and flip a new affordable housing project on your own, with crowdfunding you can be one of several investors who help get the project off the ground. Also, unlike direct investment that involves owning and managing property (and all the headaches that come with), crowdfunding is passive so you put your money to work without the stress and sweat equity that comes with owning property.  Related: Why Im Investing in Affordable Housing for the Long Haul 2. Investing in Homeownership Another take on crowdfunding, these funds are made up of pools of distressed mortgages. These funds use investor money to purchase pools of distressed mortgages and then work with homeowners to find solutions that will keep them in their homes. When you invest, you are helping not only individual homeowners but also the community by positively impacting affordable housing in the neighborhood. You make money by receiving returns from the profits. 3. Tax Reform and the Opportunity Zones Program Youve probably heard about Opportunity Zones, but just in case you arent up to speed on this program, here is a quick overview. Opportunity Zones are a new economic and community development program established by Congress in the Tax Cut and Jobs Act of 2017. The purpose is to encourage long-term economic development and housing investments in low-income communities nationwide. The law provides for the creation of Opportunity Zones, which use tax incentives to attract long-term investment to neighborhoods that are continuing to grapple with high poverty and lackluster job and business growth. Housing experts and government officials believe investment in Opportunity Zones will help prompt development of affordable housing.  Related: How the Dire Future of the Retail Market Could Solve the Housing Affordability Crisis Projects in Opportunity Zones will be eligible for funding through Opportunity Funds. Opportunity Funds are investment vehicles set up specifically for investing in eligible property located in an Opportunity Zone. To obtain the tax break, Opportunity Funds require that the investor use the gain from a prior investment for funding the Opportunity Fund. Opportunity Funds create benefits for both investor and community. Investors who are socially conscious can put their money into the communities that need it most. Investors also benefit from tax advantages. Opportunity Funds allow investors to defer federal taxes on any recent capital gains until December 31, 2026, reduce that tax payment by up to 15%, and pay as little as zero taxes on potential profits from an Opportunity Fund if the investment is held for 10 years. You can invest in an Opportunity Zone anywhere in the country, but if you are interested in keeping it local, you can find Opportunity Zones in your area by going to Opportunity Zones Resources and in the Federal Register at IRB Notice 2018-48. In Minnesota, where I live, 128 Census Tracts have been designated as Opportunity Zones. 4. Affordable Housing via Fix and Flips and Long-Term Rentals There are direct opportunities for real estate agents, investors, and builders to be more socially conscious and to have a positive impact on affordable housing through regular business dealings. With a little forethought and planning, a lot can be done to help reduce expenses when building and rehabbing homes. Homes can be made more energy efficient, safer, and designed to incur less tax. All of these can benefit potential homeowners and make housing more affordable to more people.  What other investments have you come across that could help create more affordable housing? Comment below! https://www.biggerpockets.com/renewsblog/alleviate-affordable-housing-crisis Wondering how the new The Tax Cuts and Jobs Act Section 199A regulations will affect you and your investments? Lets take a deep dive into the newly released final regulations surrounding the20% pass-through deduction, including:

What IRS Section 199A is and who exactly it applies toWho is excluded from deductions laid out under Section 199AHow the 20% pass-through deduction affects real estate investmentsRevenue Procedure 2019-7, a new release thatprovides a Safe Harbor for certain rental activityInformation you can take to your CPA to better understand how your taxes are affectedImportant advice regarding why you might need form 1099s At the end of 2017, Congress passed The Tax Cuts and Jobs Act, which was a sweeping tax reform bill, one of the largest Ive ever seen. One of the many changes was a new tax break meant for business owners operating as a sole proprietor or through a pass-through entity such as an LLC or S corporation. This tax break allows certain taxpayers to deduct 20% of the net qualified business income (QBI) for purposes of calculating their taxable income. The question many CPAs and real estate investors asked was, Will my rental real estate income count as QBI for the purposes of this 20% deduction? On January 18th, 2019, the IRS released final regulations on Section 199A, giving us our long-awaited answer. What is the IRS Code Section 199A Pass-Through Deduction?Section 199A allows business owners to take a tax deduction on their QBI. Per IRC Sec 199A(c), QBI means, for anytaxable year,the net amount ofqualified items of income, gain, deduction, and losswith respect to anyqualified trade or businessof thetaxpayer. This income must beeffectively connected with the conduct of atrade or businesswithin theUnited States, and there are exceptions to the types of income that qualify [see IRC Sec 199A(c)(3)(B)]. The term qualified trade or business means any trade or business other than a specified service trade or business (SSTB), or the trade or business of performing services as an employee. If you are single and your taxable income is below $157,500 ($315,000 if married), youll qualify for the full 20% deduction on your QBI even if you are running an SSTB. Its important to note that these thresholds areregardingtaxable income, which takes into account your standard or itemized deductions. There is a phase-out of the 20% deduction after your taxable income increases above those two thresholds. Once your taxable income exceeds $207,000 ($415,000 if married), the 20% deduction will be completely phased out for SSTB owners, and all other business owners will be subject to a limitation calculation to determine their QBI deduction. The limitation calculation is the lesser of 20% of QBI and the greater of: 50% of the taxpayers share of the W-2 wages with respect to the qualified trade or business, or25% of the taxpayers share of the W-2 wages with respect to the qualified trade or business, plus 2.5% of the taxpayers share of the unadjusted basis of the qualified property immediately after acquisition. For example, Joe is single and has taxable income of $240,000 and QBI income from his qualified business of $300,000. Joe owns 100% of the business and paid $100,000 in W-2 wages through the course of his business. Because Joes taxable income is above $207,000, Joe is subject to the limitation calculation, and his QBI deduction is calculated as follows: The lesser of: 20% of QBI = $60,000The greater of:50% of W-2 wages paid = $50,00025% of W-2 wages paid ($25,000) + 2.5% of the unadjusted basis of property ($0) = $25,000 The greater of sub-items #1 and #2 is $50,000. The lesser of #1 ($60,000) and #2 ($50,000) is $50,000. Thus, Joes QBI deduction would be $50,000.  What Are SSTBs as Related to Section 199A? A specified service trade or business (SSTB) is not considered a qualified business under Section 199A. This means that income generated by SSTBs will not be allowed a QBI deduction once the owners taxable income exceeds $207,000 ($415,000 if married). The final regulations provided clarity as to what SSTBs are and are not within each of the following fields: health, accounting and law, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, investing and investment management, and dealing/trading. If you are running a business that falls into these categories, I recommend getting with your CPA and combing through the final regulations starting on page 73 to determine if your facts and circumstances make your business an SSTB. Related: How to Gift Properties to Your Family (Not the IRS) Important for readers of BiggerPockets is that brokerage services relates to the trading of financial securities, so real estate brokers and agents will not be considered SSTBs. Additionally, real estate developers and property managers are not considered SSTBs. How Does Section 199A Apply to Rental Real Estate? Ive explained what the QBI deduction is and how/when it applies to SSTBs and business owners. But what about rental real estate? Before the final regulations dropped, there was confusion as to whether rental real estate would qualify for the QBI deduction. The source of the confusion was in determining how rental real estate activities could rise to the level of a trade or business under Section 162. If rental activities could be classified as Section 162 trades or businesses, the income produced by such activities would qualify for the QBI deduction under Section 199A. The problem is that the analysis of whether or not rentals qualify for a Section 162 trade or business is challenging due to murky regulations and case law. We needed (hoped) for some form of a bright line test to tell us whether rentals would qualify as a trade or business and thus allow us to use the QBI deduction against net rental income. Revenue Procedure 2019-7: A Safe Harbor Along with releasing the final regulations on Section 199A, the IRS also releasedRevenue Procedure 2019-7. This Revenue Procedure provides a Safe Harbor that allows a rental activity to rise to the level of a Section 162 trade or business if: Separate books and records are maintained to reflect income and expenses for each rental real estate enterprise;250 or more hours of rental services are performed per year with respect to the rental enterprise; andThe taxpayer maintains contemporaneous records, including time reports, logs, or similar documents, regarding the following: (i) hours of all services performed; (ii) description of all services performed; (iii) dates on which such services were performed; and (iv) who performed the services. This requirement will not apply to taxable years beginning prior to January 1, 2019. For item #1, a rental real estate enterprise is an interest in property held for the production of rents. An individual or a relevant pass-through entity (RPE) must hold the interest in property directly or through a disregarded entity. An RPE is a partnership or an S corporation that is owned, directly or indirectly, by at least one individual, estate, or trust. For item #2, rental services includes: Advertising to rent or lease the real estate;Negotiating and executing leases;Verifying information contained in prospective tenant applications;Collection of rent;Daily operation, maintenance, and repair of the property;Management of the real estate;Purchase of materials; andSupervision of employees and independent contractors. Rental services may be performed by owners or by employees, agents, and/or independent contractors of the owners. The term rental servicesdoes not include financial or investment management activities, such as: Unfortunately, certain forms of real estate investing are excluded from using this safe harbor. For instance, any property in which you rent and also use as a personal residence for more than 14 days per year cannot qualify for this safe harbor. Additionally, any property rented under a triple net lease (NNN) will not qualify. That is bad news for many BiggerPockets investors. If your rental activity qualifies for the Safe Harbor under Revenue Procedure 2019-7, the income will be considered QBI and will qualify for the pass-through deduction.  What if My Rentals Dont Qualify for the Safe Harbor? Its important to note that if your rental activity does not meet the criteria for the Safe Harbor under Revenue Procedure 2019-7, you may still be able to take a QBI deduction by qualifying as a trade or business under Section 162. It is difficult to know whether your rental activities qualify as a trade or business under Section 162. There are no uniform standards, and the determination of whether a landlords rentals qualify as a trade or business is made on a case-by-case basis. Thats why this safe harbor is so great for landlords and their CPAsit provides bright lines needed to make a determination. Interpreting Safe Harbor Regulations Related to Real Estate Investments Regardless, if you cant use the Safe Harbor, youll have to resort to interpreting complex and confusing case law in determining whether your rental real estate activities rise to the level of a Section 162 trade or business. The Supreme Court held inCommissioner v. Groetzingerthat, We accept the fact that to be engaged in a trade or business, the taxpayer must be involved in the activity with continuity and regularity and that the taxpayers primary purpose for engaging in the activity must be for income or profit. However, this is a broad standard and left lower courts struggling to interpret the ruling. In an attempt to shed light on the matter, the IRS discussed the concept of a rental trade or business in Private Letter Ruling 9840026: The issue of whether the rental of property is a trade or business of a taxpayer is ultimately one of fact in which the scope of a taxpayers activities, either personally or through agents, in connection with the property, are so extensive as to rise to the stature of a trade or business. Qualifying as a Real Estate Professional Doesnt Cut it Many landlords and their advisors then thought that qualifying as a real estate professional would allow their rental activities to rise to the level of a trade or business. However, courts have held that qualifying as a real estate professional merely allows one to overcome the presumption that their rental activities are not passive. This means that simply qualifying as a real estate professional will not allow you to claim that your rental activities rise to the level of a trade or business. The above is not meant to be an in-depth discussion on how to qualify your rental real estate activities. It is intended to provide you with high-level information that you can take to your CPA to start a dialogue. Watch Out for the Requirement to Issue Form 1099s So youve gone through Section 199A and determined that your rentals either qualify for the safe harbor or rise to the level of a trade or business. This means that they qualify for the QBI deduction and youll enjoy sweet tax savings as a result. Just make sure your tax savings dont get wiped out by penalties for not issuing Form 1099s. Whats that? You didnt know of this requirement? Of course not, because landlords arent necessarilyrequired to issue Form 1099s for their passive activities. But taxpayers engaged in a trade or business are required to issue Form 1099s. So if you are claiming that your rental real estate activities rise to the level of a trade or business, youll have to issue Form 1099s for payments youve made throughout the year. If your rental activities rise to the level of a trade or business, the only time you dont need to issue a Form 1099 to a vendor is when the payment was made to another business that is incorporated,but was not for medical or legal services or the sum of all payments made to the person or unincorporated business is less than $600 in one tax year. In order to collect the information you need to issue a Form 1099, you should request a Form W-9 from the vendor. We encourage our clients torequire a Form W-9 be provided to them by the vendor before any work starts on a rental property. This includes contractors, property managers, and even your CPA! Summary: Speak With Your CPA Regarding Section 1099A Rules What a load of information. The good news is that much clarity was provided with the issuance of final regulations for Section 199A. A Safe Harbor was provided for landlords via Revenue Procedure 2019-7 that provide bright-line tests for qualifying your rental activities as a trade or business. The bad news is that the 250-hour requirement of the Safe Harbor may be tough for some small landlords to meet. Additionally, investors leasing on a triple net basis seemed to have gotten the worst of it all. Speak with your CPA and get a plan in place for 2019. There are many strategies that you can now confidently tap into in order to make the Section 199A rules work in your favor. Any questions about IRS Code Section 1099A or the 20% pass-through deduction? Does this bode well for your investments? Weigh in with a comment! https://www.biggerpockets.com/renewsblog/irs-code-section-199a-20-pass-through-deduction Wondering how the new The Tax Cuts and Jobs Act Section 199A regulations will affect you and your investments? Lets take a deep dive into the newly released final regulations surrounding the20% pass-through deduction, including:

What IRS Section 199A is and who exactly it applies toWho is excluded from deductions laid out under Section 199AHow the 20% pass-through deduction affects real estate investmentsRevenue Procedure 2019-7, a new release thatprovides a Safe Harbor for certain rental activityInformation you can take to your CPA to better understand how your taxes are affectedImportant advice regarding why you might need form 1099s At the end of 2017, Congress passed The Tax Cuts and Jobs Act, which was a sweeping tax reform bill, one of the largest Ive ever seen. One of the many changes was a new tax break meant for business owners operating as a sole proprietor or through a pass-through entity such as an LLC or S corporation. This tax break allows certain taxpayers to deduct 20% of the net qualified business income (QBI) for purposes of calculating their taxable income. The question many CPAs and real estate investors asked was, Will my rental real estate income count as QBI for the purposes of this 20% deduction? On January 18th, 2019, the IRS released final regulations on Section 199A, giving us our long-awaited answer. What is the IRS Code Section 199A Pass-Through Deduction?Section 199A allows business owners to take a tax deduction on their QBI. Per IRC Sec 199A(c), QBI means, for anytaxable year,the net amount ofqualified items of income, gain, deduction, and losswith respect to anyqualified trade or businessof thetaxpayer. This income must beeffectively connected with the conduct of atrade or businesswithin theUnited States, and there are exceptions to the types of income that qualify [see IRC Sec 199A(c)(3)(B)]. The term qualified trade or business means any trade or business other than a specified service trade or business (SSTB), or the trade or business of performing services as an employee. If you are single and your taxable income is below $157,500 ($315,000 if married), youll qualify for the full 20% deduction on your QBI even if you are running an SSTB. Its important to note that these thresholds areregardingtaxable income, which takes into account your standard or itemized deductions. There is a phase-out of the 20% deduction after your taxable income increases above those two thresholds. Once your taxable income exceeds $207,000 ($415,000 if married), the 20% deduction will be completely phased out for SSTB owners, and all other business owners will be subject to a limitation calculation to determine their QBI deduction. The limitation calculation is the lesser of 20% of QBI and the greater of: 50% of the taxpayers share of the W-2 wages with respect to the qualified trade or business, or25% of the taxpayers share of the W-2 wages with respect to the qualified trade or business, plus 2.5% of the taxpayers share of the unadjusted basis of the qualified property immediately after acquisition. For example, Joe is single and has taxable income of $240,000 and QBI income from his qualified business of $300,000. Joe owns 100% of the business and paid $100,000 in W-2 wages through the course of his business. Because Joes taxable income is above $207,000, Joe is subject to the limitation calculation, and his QBI deduction is calculated as follows: The lesser of: 20% of QBI = $60,000The greater of:50% of W-2 wages paid = $50,00025% of W-2 wages paid ($25,000) + 2.5% of the unadjusted basis of property ($0) = $25,000 The greater of sub-items #1 and #2 is $50,000. The lesser of #1 ($60,000) and #2 ($50,000) is $50,000. Thus, Joes QBI deduction would be $50,000. What Are SSTBs as Related to Section 199A? A specified service trade or business (SSTB) is not considered a qualified business under Section 199A. This means that income generated by SSTBs will not be allowed a QBI deduction once the owners taxable income exceeds $207,000 ($415,000 if married). The final regulations provided clarity as to what SSTBs are and are not within each of the following fields: health, accounting and law, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, investing and investment management, and dealing/trading. If you are running a business that falls into these categories, I recommend getting with your CPA and combing through the final regulations starting on page 73 to determine if your facts and circumstances make your business an SSTB. Related: How to Gift Properties to Your Family (Not the IRS) Important for readers of BiggerPockets is that brokerage services relates to the trading of financial securities, so real estate brokers and agents will not be considered SSTBs. Additionally, real estate developers and property managers are not considered SSTBs. How Does Section 199A Apply to Rental Real Estate? Ive explained what the QBI deduction is and how/when it applies to SSTBs and business owners. But what about rental real estate? Before the final regulations dropped, there was confusion as to whether rental real estate would qualify for the QBI deduction. The source of the confusion was in determining how rental real estate activities could rise to the level of a trade or business under Section 162. If rental activities could be classified as Section 162 trades or businesses, the income produced by such activities would qualify for the QBI deduction under Section 199A. The problem is that the analysis of whether or not rentals qualify for a Section 162 trade or business is challenging due to murky regulations and case law. We needed (hoped) for some form of a bright line test to tell us whether rentals would qualify as a trade or business and thus allow us to use the QBI deduction against net rental income. Revenue Procedure 2019-7: A Safe Harbor Along with releasing the final regulations on Section 199A, the IRS also releasedRevenue Procedure 2019-7. This Revenue Procedure provides a Safe Harbor that allows a rental activity to rise to the level of a Section 162 trade or business if: Separate books and records are maintained to reflect income and expenses for each rental real estate enterprise;250 or more hours of rental services are performed per year with respect to the rental enterprise; andThe taxpayer maintains contemporaneous records, including time reports, logs, or similar documents, regarding the following: (i) hours of all services performed; (ii) description of all services performed; (iii) dates on which such services were performed; and (iv) who performed the services. This requirement will not apply to taxable years beginning prior to January 1, 2019. For item #1, a rental real estate enterprise is an interest in property held for the production of rents. An individual or a relevant pass-through entity (RPE) must hold the interest in property directly or through a disregarded entity. An RPE is a partnership or an S corporation that is owned, directly or indirectly, by at least one individual, estate, or trust. For item #2, rental services includes: Advertising to rent or lease the real estate;Negotiating and executing leases;Verifying information contained in prospective tenant applications;Collection of rent;Daily operation, maintenance, and repair of the property;Management of the real estate;Purchase of materials; andSupervision of employees and independent contractors. Rental services may be performed by owners or by employees, agents, and/or independent contractors of the owners. The term rental servicesdoes not include financial or investment management activities, such as: Unfortunately, certain forms of real estate investing are excluded from using this safe harbor. For instance, any property in which you rent and also use as a personal residence for more than 14 days per year cannot qualify for this safe harbor. Additionally, any property rented under a triple net lease (NNN) will not qualify. That is bad news for many BiggerPockets investors. If your rental activity qualifies for the Safe Harbor under Revenue Procedure 2019-7, the income will be considered QBI and will qualify for the pass-through deduction. What if My Rentals Dont Qualify for the Safe Harbor? Its important to note that if your rental activity does not meet the criteria for the Safe Harbor under Revenue Procedure 2019-7, you may still be able to take a QBI deduction by qualifying as a trade or business under Section 162. It is difficult to know whether your rental activities qualify as a trade or business under Section 162. There are no uniform standards, and the determination of whether a landlords rentals qualify as a trade or business is made on a case-by-case basis. Thats why this safe harbor is so great for landlords and their CPAsit provides bright lines needed to make a determination. Interpreting Safe Harbor Regulations Related to Real Estate Investments Regardless, if you cant use the Safe Harbor, youll have to resort to interpreting complex and confusing case law in determining whether your rental real estate activities rise to the level of a Section 162 trade or business. The Supreme Court held inCommissioner v. Groetzingerthat, We accept the fact that to be engaged in a trade or business, the taxpayer must be involved in the activity with continuity and regularity and that the taxpayers primary purpose for engaging in the activity must be for income or profit. However, this is a broad standard and left lower courts struggling to interpret the ruling. In an attempt to shed light on the matter, the IRS discussed the concept of a rental trade or business in Private Letter Ruling 9840026: The issue of whether the rental of property is a trade or business of a taxpayer is ultimately one of fact in which the scope of a taxpayers activities, either personally or through agents, in connection with the property, are so extensive as to rise to the stature of a trade or business. Qualifying as a Real Estate Professional Doesnt Cut it Many landlords and their advisors then thought that qualifying as a real estate professional would allow their rental activities to rise to the level of a trade or business. However, courts have held that qualifying as a real estate professional merely allows one to overcome the presumption that their rental activities are not passive. This means that simply qualifying as a real estate professional will not allow you to claim that your rental activities rise to the level of a trade or business. The above is not meant to be an in-depth discussion on how to qualify your rental real estate activities. It is intended to provide you with high-level information that you can take to your CPA to start a dialogue. Watch Out for the Requirement to Issue Form 1099s So youve gone through Section 199A and determined that your rentals either qualify for the safe harbor or rise to the level of a trade or business. This means that they qualify for the QBI deduction and youll enjoy sweet tax savings as a result. Just make sure your tax savings dont get wiped out by penalties for not issuing Form 1099s. Whats that? You didnt know of this requirement? Of course not, because landlords arent necessarilyrequired to issue Form 1099s for their passive activities. But taxpayers engaged in a trade or business are required to issue Form 1099s. So if you are claiming that your rental real estate activities rise to the level of a trade or business, youll have to issue Form 1099s for payments youve made throughout the year. If your rental activities rise to the level of a trade or business, the only time you dont need to issue a Form 1099 to a vendor is when the payment was made to another business that is incorporated,but was not for medical or legal services or the sum of all payments made to the person or unincorporated business is less than $600 in one tax year. In order to collect the information you need to issue a Form 1099, you should request a Form W-9 from the vendor. We encourage our clients torequire a Form W-9 be provided to them by the vendor before any work starts on a rental property. This includes contractors, property managers, and even your CPA! Summary: Speak With Your CPA Regarding Section 1099A Rules What a load of information. The good news is that much clarity was provided with the issuance of final regulations for Section 199A. A Safe Harbor was provided for landlords via Revenue Procedure 2019-7 that provide bright-line tests for qualifying your rental activities as a trade or business. The bad news is that the 250-hour requirement of the Safe Harbor may be tough for some small landlords to meet. Additionally, investors leasing on a triple net basis seemed to have gotten the worst of it all. Speak with your CPA and get a plan in place for 2019. There are many strategies that you can now confidently tap into in order to make the Section 199A rules work in your favor. Any questions about IRS Code Section 1099A or the 20% pass-through deduction? Does this bode well for your investments? Weigh in with a comment! https://www.biggerpockets.com/renewsblog/irs-code-section-199a-20-pass-through-deduction If youre looking for a job thats stress-free, your best bet might be to find a gig where you crunch numbers in a cubicle and dont have to deal with people. But heads up, jobs like that can get old quickly.

Landlording is pretty far on the other end of the spectrum. Its definitely not a stress-free job, but it doesnt have to be overwhelming. If you understand what stresses you out and develop a plan for mitigating those factors, you can carve out a successful career as a real estate investor/landlordand genuinely love what you do! Major Causes of Stress Your personality and other situational factors will dictate the level of stress you experience as a landlord. If youre anything like most people, youre likely to be impacted by the following: Poor cash flow. Nothing is more stressful than dealing with cash flow problems and wondering if youll be able to pay the mortgage, taxes, and bills to keep the property above water.Late payments. One of the biggest frustrations landlords have with tenants is late and/or irregular payments. Not only does it impact cash flow, but it also causes the landlord to waste time and energy tracking the money down.Legal issues. Real estate can be complicated. If you arent careful, you could end up in legal trouble for even the simplest of mistakes or oversights.Careless tenants. Bad tenants have a tendency to be irresponsible with a property, causing damage or problems that stick around long after theyre gone. These are the hot button issues for most landlords. Being able to pinpoint them and wrap your mind around why they stress you out is a good starting point toward resolution. Related:The Rookie Landlording Mistake Most New Investors Make 4 Tips for Overcoming Stress Once you know what stresses you out, you can develop a proactive plan for overcoming these issues and finding peace. Here are some suggestions: 1. Hire a Property Manager There are certain relationships in life that function best when there is a third party go-between to separate the emotions and eliminate the pitfalls that can occur when two parties work directly with one another, explains Green Residential,a Houston-based property management company. The relationship between a landlord and a tenant is one of these relationships. If you want to avoid some of the friction that comes with interacting directly with tenants, hire a property manager. Its usually worth every penny. 2. Carefully Screen Tenants Good tenants equal stress-free landlording. If you want the rest of your experience to go well, it all starts with the screening process. Screening your tenant means looking into the information they provided, as well as analyzing outside information you can discover, and coming to a reasonable estimate on the kind of tenant they will be, veteran RE investor Brandon Turner explained in his step-by-step tenant screening guide.I say reasonable estimate because there are no surefire ways to know the future quality of a tenant. As a landlordit is our job to simply screen effectively and choose the best possible applicant for the property.  Turner looks for six specific qualities in a tenant: ability to afford the rent payment, willingness to pay on time, job stability, cleanliness and housekeeping skills, aversion to drugs and criminal activity, and a low stress quotient (how much stress theyll cause you). 3. Automate Rent Collection Manually collecting renteither face-to-face or through the mailis slow, inefficient, and cumbersome. If you want to limit the amount of effort it takes (and lower the stress quotient) try automating rent collection through an online platform. Better yet, require your tenants to set up direct deposit. Related:5 Practical Solutions For Landlords With Rent Payment Drama 4. Keep an Emergency Fund In an effort to prevent cash flow and money-related stress, you should create an emergency fundfor each rental property you own. The fund should essentially be a dedicated cash savings account that has enough money to bankroll your property for three to six months. This will give you something to fall back on in the event of a worst-case scenario.  Above All, Enjoy What You Do The role of landlord doesnt have to be daunting. When done right, it can be exciting! But in order to enjoy the perks of the job, you have to address the pain points that so often frustrate people in your position. Implementing the strategies above will hopefully pave the way for greater freedom and enjoyment during your tenure as a landlord. Do you have experience landlording? How have you dealt with the stress? Are you apprehensive about landlording-related stress? What are your major concerns? Id love to learn from your experience. Comment below! https://www.biggerpockets.com/renewsblog/reduce-landlord-stress Would your real estate business benefit from better rehab/construction knowledge or tactics? Well, thats the focus of todays show, where Andresa shares her story of moving from Brazil to America and crushing it in the real estate space!

Andresa excels in an area many of us find extremely challenging: managing rehabs. In this episode, she pulls back the curtain and shares tips for how you can do the same. Andresa gives great advice for finding excellent contractors (and vetting them), the three things she puts in every contract, and how she makes sure shes never ripped off. You wont want to miss her advice on finding the perfect team, determining the scope of work for your project, and learning your market. Andresa also shares a killer tip about challenging low appraisals shes used successfully three separate times! Andresa is able to skillfully manage several rehab projects at a time while also running a side Airbnb business and gives great guidance on how you can do the same. Download this one now! Click hereto listen on iTunes. Listen to the Podcast HerePodcast: Play in new window | Download Subscribe: Apple Podcasts | Android | RSS Watch the Podcast Here [embedded content] Help Us Out! Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it! This Show Sponsored By To sign up for a free account and start browsing cash flowing rental homes, visitroofstock.com/biggerpockets. Deep Dive Sponsor If youve been thinking about getting a SimpliSafe Home Security System, but have beenwaiting for the holidays when all the tech deals come outyouve made a smart move! If you go to SimpliSafe.com/biggerpocketsyoull get 25% off any new system. Thats an amazing deal. They rarely do anything like this but theyre doing it just for us! Fire Round Sponsor Fundriseenables you to invest in high-quality, high-potential private market real estate projects. Im talking anything from high rises in D.C. to multi-families in L.A. institutional-quality stuff. And each project is carefully vetted and actively managed by Fundrises team of real estate pros.Their high-tech, low-cost online platform lets you track the progress of every single project, and keep more of the money you make. Oh, and by the way, you dont have to be accredited. VisitFundrise.com/biggerpocketsto have your first 3 months of fees waived. In This Episode We Cover:How Andresa got into real estateHow she finds great contractorsThe three things she puts in her contractHow she pays her contractorsHer advice for finding the perfect teamHow she embraces what shes good atWhy you should be humble enough to partner with othersHow she determines her scope of workTips for understanding your marketHow she challenges appraisalsHer advice for Airbnb investingAnd SO much more!Links from the ShowBooks Mentioned in this ShowTweetable Topics:Theres somebody for every role.(Tweet This!)Get the no first because that is when the negotiation starts. (Tweet This!)Partner up with somebody that is willing to share to you the entire process.(Tweet This!)Connect with Andresa https://www.biggerpockets.com/renewsblog/biggerpockets-podcast-314-find-rockstar-contractors-and-manage-like-a-boss-andresa-guidelli This article is an excerpt from The Book on Tax Strategies for the Savvy Real Estate Investor by Amanda Han and Matthew MacFarland. Pick up a copy from the BiggerPockets Bookstore!