|

Whats a better investment, stocks or real estate?And, while were asking this grandiose question, whats a safer investment?

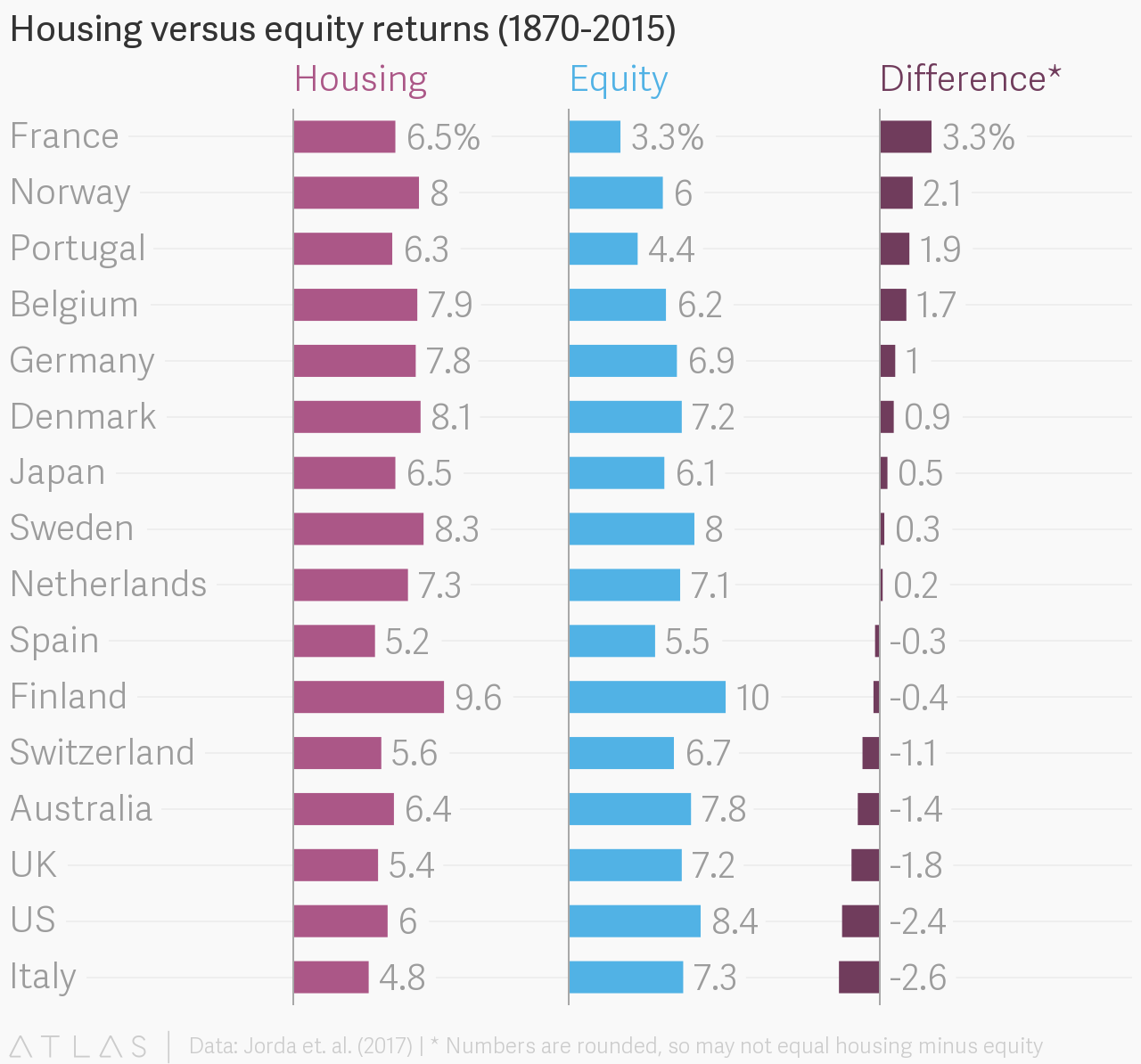

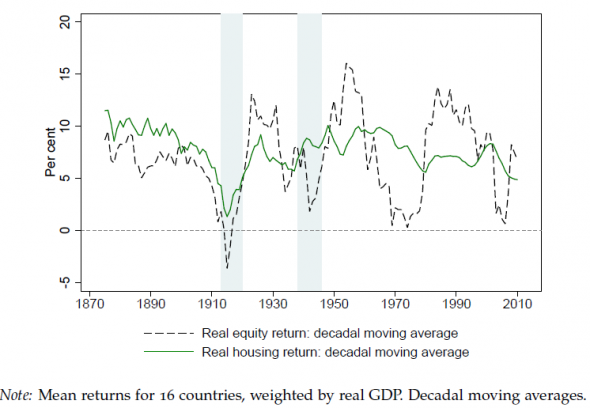

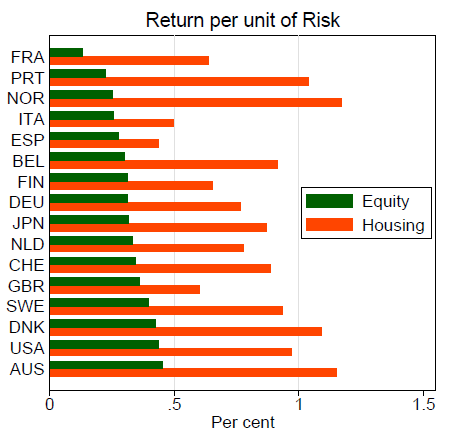

You probably have an opinion already as to the answer to both of these questions. Its good to have opinions about important questions. And these certainly are important questions they directly affect how you grow your wealth. But opinions are never as useful as facts. A team of economists from the University of California, Davis, the University of Bonn, and the German central bank, set out to answer these questions by analyzing a stunning amount of data. Answer it they did. Ready for 145 years of economic data, summarized over the next five minutes for you? The Rate of Return on Everything The lead authors of the study Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor reported the findings of their massive study in a paper entitledThe Rate of Return on Everything, 1870-2015. In it, researchers looked at 16 advanced economies over the past 145 years. Specifically, they compared returns on equities, residential real estate, short-term treasury bills, and longer-term treasury bonds. With each asset type, they adjusted for inflation and included all returns, not just appreciation. Dividend income was included for equities, and rental income was included for residential real estate. Their findings, in short: Residential real estate had the best returns, averaging over 7 percent per annum. Equities werent far behind, at just under 7 percent. Then came bonds and bills, with far lower returns (surprising to no one). Related:Worried About a Stock Market Crash? Prepare for the Bear Without Fear  Equities vs. Real Estate Rental income proved an important factor roughly half of the returns on real estate came from rents, while the other half came from appreciation. Equities and real estate each performed differently in various countries, of course. Heres a comparison of each of the 16 countries when considering equities versus real estate:  Keep in mind, these are long-term averages over the course of many decades. In real time, these returns bounced up, down, sideways, and in circles. Heres a curious little chestnut for you: from 1980-2015, equities have, on average, performed significantly better than real estate. Across the 16 countries studied, equities earned an average annual return of 10.7 percent, decisively beating real estates stolid 6.4 percent. Should we all sell our rentals and buy stocks? Of course not. But the reasons are multiple and a bit nuanced. First, a few outlier countries threw off the average returns from 1980-2015. Japan saw its real estate markets collapse as its population aged and started declining. In Germany, real estate has been stuck in the slow lane for decades. Meanwhile, equities in Scandinavia have exploded. But the most interesting case for real estate lies in its risk-reward ratio. Of Risk and Volatility Lets do a quick stereotype check-in, shall we? Treasury bonds are low-risk, low-return. I dont think anyones prepared to challenge that stereotype after all, stereotypes exist for a reason, right? Equities are high risk, high return. This one gets a little more interesting, but a quick look at how stock markets have gyrated for the last century up 29 percent one year and down 18 percent the next should disabuse anyone of the notion that equities dont come with high volatility and risk. And that brings us to an economic assumption that dates back to, well, the beginning of economic theory. Economists have long held as a given that risk and returns are highly correlated, and that the invisible hand of the market will ensure that remains the case. Why? Because if an asset were low-risk, high-return, everyone and their mother would fling so much money at it that the returns would dry up faster than Lindsay Lohans acting career. Except that assumption hasnt held true for residential rental properties. Rental Properties: Low Risk, High Returns Throughout modern history, residential real estate has actually boasted extremely high returns with low risk. Take a look at volatility for equities versus real estate for the past 145 years:  Brighter economics minds than mine are scratching their heads as to why that is. But since I cant resist offering a (you guessed it!) opinion, here are a few thoughts as to why. First, real estate is expensive. Until the past ten years, with the advent of crowdfunding, you couldnt invest your extra $100 a month in it like you could do with stocks. Even if you leverage to the hilt and borrow the maximum mortgage allowed, that still usually puts you at 20 percent down, plus thousands of dollars in closing costs. Which says nothing of credit requirements, income requirements, and/or lenders requirements for investing experience. In other words, real estate investing has a high barrier to entry. Its also difficult to diversify for those very same reasons. If each asset requires $20,000 in cash to purchase it, then it takes a lot of money to build a broad, diverse portfolio. Real estate is also notoriously illiquid. You cant buy it and sell it on a whim it typically takes months to do either one. But hey, thats also precisely why its so much more stable than equities. Related:The Irrefutable Advantage Real Estate Investors Have Over Stock Investors Sharpe Ratios & Measuring Risk vs. Return How do you measure an investments risk against its return? It turns out, theres a simple way to do this, a literal risk-reward ratio. Its called the Sharpe ratioafter its creator, William Sharpe. You start with an assets return, and subtract out the return of the going with a short-term, risk-free alternative (like U.S. Treasury bills). That gives you a risk premium the extra return the asset delivers, over a risk-free investment. Then you simply divide that risk premium over the assets volatility, as measured by its annual standard deviation in value: Risk Premium ___________________________ Average Annual Standard Deviation If the math is giving you a headache, dont worry about it. Just think of it as return divided by risk. A higher ratio indicates a better investment greater return, relative to the risk. Treasury bonds clocked in at a Sharpe ratio of around .2. Weak sauce. Equities werent much better, at .27. Sure, their returns were strong, but theyre more volatile than plutonium in a mad scientists lab. But residential real estate? It averaged a Sharpe ratio of .7. For everyone who didnt like the look of how real estate returns have compared to stock returns over the past few decades, consider that the Sharpe ratio for real estate has only grown stronger over time. Since 1950, the Sharp ratio for real estate has averaged an impressive .8. Another way of looking at it is return per unit of risk heres how equities have compared to real estate in each of the 16 countries studied:  Returns & GDP Advanced economies tend to have slow economic growth, right? So how have returns done so much better than the GDP growth in these countries?Aside from the obvious issue that these economies looked very different in 1870 than they do today, theres an interesting answer to this query.  It turns out, a countrys returns on its equities and real estate are not tied in a 1:1 relationship with its GDP. Over time, returns on these assets tend to average growth around double the speed of the countrys economy as a whole measured by GDP (see chart at right). It turns out, a countrys returns on its equities and real estate are not tied in a 1:1 relationship with its GDP. Over time, returns on these assets tend to average growth around double the speed of the countrys economy as a whole measured by GDP (see chart at right).If anything, that returns average double GDP growth summary is skewed low, because it includes the weak returns on bonds and bills. On average, equities and real estate perform several times better than GDP growth. This helps explain why income inequality tends to expand over time in advanced economies. The average Joe does not own stock, and if he owns any real estate, its his one individual home a home that he probably only earns appreciation on with no rental income (and remember, rental income makes up half of real estates returns!). So how does Average Joes finances improve? Only through a raise. His raise is tied to how his employer is doing, which, in turn, is tied to how the economy is doing. In other words, Average Joes finances are tied to GDP growth. But Wealth Wise Wendy, whos not nearly so average as Joe, invests as much money as she can in equities and real estate. She builds a portfolio of passive income that earns money even while she sleeps. That income is based on the returns of her investments, not based on the economy. Conservatives and liberals can argue all they want about how much to redistribute wealth. But as an individual, you want to be like Wendy, not Joe. You want your wealth and income tied to the returns of equities and real estate, not tied to GDP. Where Do Bonds Fit in This Discussion? Bonds are boring. No, really. We already talked about how theyre low risk, low return. Why bother with them if you can invest in rental properties, which are low risk, high return? A common opinion I hear people say is, Bonds may not have performed well over the past 15 years, but thats abnormal! Just look at how well they did in the 80s! Interestingly, this new study disproves that notion. The high bond yields of the 1980s were actually the anomaly in fact, if you look at bond returns over the past 145 years, there were many periods where they earned negative returns. Want a few reasons why rental properties are better investments than bonds?  Heres a simple one: bonds expire. They pay out for a specific term, then they stop paying. Rental properties keep paying forever. And not only do they keep paying indefinitely, they pay more over time. With every year that goes by, fixed bond payments become less valuable in real purchasing power due to inflation. But rents rise right alongside inflation. Its actually your fixed mortgage payment that goes down over time in inflation-adjusted dollars!Then one day that mortgage payment disappears, and your rental cash flow explodes. OK; yes, government bonds offer stability. They pay the same amount every month. They never call you about a leaky roof or stop sending payments because they spent too much on cigarettes and Bud Light that month. But at what cost in returns? If retirement looms on the horizon for you, familiarize yourself with sequence riskandhow rentals affect the 4 percent rule so you dont necessarily have to resort to bonds. Should I Stop Investing in Equities and Just Buy Rental Properties? Stocks may be a roller coaster, but in the long run, the good times outweigh the bad. They also balance rental properties well. And as we discussed last week, when equities go down, residential real estate almost always goes up. Equities are liquid. You can buy and sell at a moments notice. Real estate isnt quite so easy to get in and out of. Equities also offer truly passive income. I love talking about passive income from rental properties I teach an entire course about it! But ultimately, rental income can never be as passive as dividend income. Its much easier to diversify with stocks as well. You can spread $500 across thousands of companies, in every region of the world, in every industry, at every market cap. Youd be lucky to get away with only putting down $5,000 on a single rental property! Residential rental properties offer excellent returns with low volatility. I love rental properties. But that doesnt mean theres no place for equities in your portfolio. If you invest well, rental income will start performing for you immediately. Equities will take longer; the stocks you buy today wont produce significant income for you until 10, 20, 30 years from now. But theyll grow in value for you at prodigious rates. Build a portfolio of passive income from rentals and dividends, and when your peers are still working in a decade or two, their incomes tied to GDP growth, you can offer sympathetic words. And then you can go back to playing golf and relaxing with your children, having reached financial independence. Were republishing this article to help out our newer readers.  What are your thoughts on stocks versus residential real estate? Do you disagree with my dismissive attitude towards bonds? How do you decide how to allocate your assets and investments? Bring on the opinions in the comments below! https://www.biggerpockets.com/renewsblog/real-estate-vs-stocks-performance

0 Comments

Chris and Debbie Emick have two daughtersAND are well on their way to financial independence through a combination of local and long distance real estate investing coupled with frugality and conscious spending.

Chris and Debbie are everyday Joes living the dream in small-town Colorado. Debbie home schools their two daughters and manages their rental property business from home, after her 14-year career in teaching. Chris is a passionate leader to his team of network engineers by day and organic gardener/personal finance extraordinaire by night. Their home base is rural Southeastern CO, where they can go for dirt-road runs and trafficless drives while still being able to make quick mountain trips for hiking, backpacking, and skiing. This is the first in a periodic series of interviews with families who are on the path to financial freedom. Click hereto listen on iTunes. Listen to the Podcast HerePodcast: Play in new window | Download Subscribe: Apple Podcasts | Android | RSS Watch the Podcast Here [embedded content] Help Us Out! Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds.Thanks! We really appreciate it! Podcast Sponsor  The all-newFreshBooksis accounting software that makes running your small business easy, fast and secure. Spend less time on accounting and more time doing the work you love. The all-newFreshBooksis accounting software that makes running your small business easy, fast and secure. Spend less time on accounting and more time doing the work you love.For a 30-day unrestricted trial, go toFreshBooks.com/bpmoney In This Episode We Cover:Chris and Debbies personal finance journeyDebbies autoimmune disease diagnosisLifestyle changes and adjustments they made to achieve their objectivesUsing the YNAB app to budget their moneyHow they track all their spendingHow their budget worksWhy they invest their money in real estateThe very first property they purchasedProperties they have purchased sinceThe cash flow they produce from their portfolioHousehold and quality of life improvementsTheir goals for the next few yearsWhat the cash flow quadrant isAnd SO much more!Links from the ShowBooks Mentioned in this ShowTweetable Topics:You find what you are looking for.(Tweet This!)If we can do it, they can do it, too. It is just a matter of taking a look at priorities. (Tweet This!)Connect with the Chris and Debbie https://www.biggerpockets.com/renewsblog/biggerpockets-money-podcast-25-raising-a-family-seeking-financial-freedom-with-chris-and-edbbie-emick The links to third-party products and services on this page are affiliate links, meaning that BiggerPockets may earn a commission (at no additional cost to you) if you click through and make a purchase.

Today were talking about the crappiest of real estate investingproperty management and dealing with tenants and toilets. I reluctantly started my own property management company when I established my turnkey company because I didnt think I could have a successful turnkey company without in-house property management. Now my thoughts have changed, so Im going to be somewhat of a hypocrite and share a different viewpoint with you guys. In all honesty, we have done a great job over the years from an external viewpoint. Everyone has had tremendous success, but from an internal standpoint, it has been tough. Its a tough gig dealing with tenants. Its a tough gig dealing with toilets. Youre kind of spread thin, especially when you start a property management company. In the early days, youre running around like a headless chicken trying to put out all of these fires. When things start to get better and more consistent, you start hitting that critical, massive scale. If you want to run a property management company in a legitimate way, youre not going to make money until you get 300 or more units under management. We have always tried to stay honest and do it the right way, unlike many other property managers out there. [embedded content] With that being said, property management is not a sexy business. Its a tough business. Its customer service. The toughest part is to keep your employees happy, motivated, inspired, and satisfied because theyre constantly dealing with problems. There is always something going wrong, and it is tough working day-to-day in that department.Weve been through the tough times and have gotten to a point now where weve mastered the craft when it comes to property management. First, I want to say this: I think anyone who believes they can successfully manage properties from out-of-state or the country is in for a disaster. I strongly urge you not to do that because youre going to be dealing with the tenants and toilets. Theyre going to be calling you and asking for you to do all kinds of maintenance and complaining about it. You are going to have to coordinate maintenance items to be repaired and access with the tenantsand then theyre not going to be at the property and you have to give a 24 hours notice. Guys, you do not want to manage real estate from afar. You do not even want to manage real estate in your own backyard because that is not passive income, in my opinion. That is not financial freedom; that is a job. You should invest in real estate and pass on property management to the experts. You should not self-manage. That is just my opinion. Im not saying that I am right or wrong. Related: 6 Advantages to Hiring a Property Manager (& Why I Wish I Did Sooner) So, How Do You Find a Good Property Manager? That is the magic question, right? Look, its tough because a lot of them are shady operators, and a lot of them are not doing the right thing. Make sure to ask the right questions when interviewing a property management company. How long have you been in business? What is your fee structure? What do you charge every single month? What is your tenant placement fee? Do you have a leasing renewal fee? Do you have administrative fees? Do you up-charge maintenance? Now, dont get too caught up in these fees because property management is a tough business and they do a lot of work and dont get much money for doing all of that work. So dont crucify them if they charge all of these fees. They have to eat and pay the bills. What you dont want is property management taking advantage of you by up-charging maintenance too much or making up non-existent maintenance charges just to charge you. That is fraud and stealing and not someone you want to do business with. One thing that we havent done for many years is not charge at all and that was not a smart idea. I thought since we had a company that buys and sells houses, we would make money doing that and would manage the properties as a complimentary business to that. But that was a bad idea because businesses have to be profitable to offer a service of value to its customers. So we have changed our policy and introduced different fee structures. Another way you can see if a company is good or not is to go online and check out their reviews, even though a lot of property management companies have bad reviews. This is generally because you cant make tenants happy. Sometimes, no matter what you do, you cant make them happy. They are irrational and get pissed off and frustrated, and then they go online and post bad reviews. Still, I think checking reviews is a good place to get your finger on the pulse of the business and where the property management company stands, but I dont think its a legitimate guide to who is a good operator and who isnt. What I think is very important is communication. I just had an investor at our office say they reached out to a lot of companies who did not even reply. They said they emailed them and inquired but never got a response. I thought that was weird because that is new business. So, if these guys arent replying promptly to someone who is interested in their services, just imagine when it comes to dealing with you and your properties. Its just not a good sign. Related: Why I Fired Property ManagementAnd Began to Manage My Own Investments Another question you could ask is what property management software they use. I think all legitimate property management companies have to have a software like Buildium(to learn more about Buildium, click here), AppFolio, etc. We used Buildium and moved over to AppFolio. They are kind of the same. Regardless, I think all companies should use software where they can onboard you and give you access to your account so you can go on there and see what is going on. Last but not least, ask for a referral to someone who has had their properties under the property management company for an extended period. I think the referral is going to be your most honest critic and tell you how the company really operates. The proof is in the pudding. A companys track record is where you can get the best insight about how that property management company will do. Any property management nightmares out there? If you have any suggestions, questions, or tips, please comment below. https://www.biggerpockets.com/renewsblog/find-property-management-company/ When acquired in the context of a thoughtful strategy, real estate investments can be a great vehicle to help you achieve all your financial goals. A well-constructed real estate portfolio can provide passive income to fund and outlast your retirement. That same portfolio can help you grow your net worth to maximize your investments and allow you to leave a legacy for your loved ones. Also, it can help you reduce risk across all your investments by diversifying your holdings with assets that serve as inflation and interest rate risk hedges. Finally, real estate investments can provide an alternative way to fund college tuition for your kids or grandkids.

The first thing youll want to do before you dive into the strategy isto define the problem you are trying to solve. Some focusing questions you may want to ask yourself: How many years of college education are you funding? Are we talking about a 4-year bachelors eegree or do you want to also fund graduate studies?Are you looking to fund college education in a state university or a private college? The tuition cost can vary dramatically depending on which option.Do you want to fund 100 percent of the tuition cost or some other percentage? Some parents feel that their children will appreciate and make the most out of their degree when they have to cover a portion of the expenses themselves.Are you looking to fund just tuition and books or room and board as well? Again, some parents dont want their children to need to work when attending college, while others feel that working while going to school can keep college distractions at bay. Based on the answers to those questions, you can start to quantify both the total cost of college tuition youre trying to fund and the timing of when each payment is due. Before we go deep into the details of each strategy, lets agree on a set of facts. Lets say youre in your late 30s and youre trying to fund four years of tuition, books, room, and board at University of Texas (public, in-state college) for your two-year-old daughter using real estate investments. Using a free online tool like Vanguard College Cost Projector, we can estimate the future cost to be $198,800. One thing to keep in mind here is that the rate of inflation for college tuition is much higher than normal inflation. I used the 10-year historical rate of 5% for the purposes of this calculation.  Via: Vanguard College Cost Projector Via: Vanguard College Cost ProjectorNow, I want to show you two real estate investment strategies you can use to fund college tuition without exposing yourself further to stock market risk and fluctuations: The Earmarked Asset and the Cash Flow as You Go strategies. The Earmarked Asset Strategy In this strategy, you acquire a property that you earmark for the purpose of funding college tuition. This property is part of your real estate portfolio, but it doesnt contribute to any other financial goals except funding college tuition. The next step is to use its positive cash flow and other savings from your disposable income to pay off the mortgage on the property by the time your daughter is ready to start college. Last but not least, you liquidate the property during the year your daughter starts attending college, and you fund all four years of college at that time. Lets walk through the numbers. Your daughter will attend college in 16 years at which point you will need $198,800 to cover four years of tuition, books, room, and board. If were going to purchase, pay off, and liquidate an asset to cover those costs, we need to make sure that you net $198,800 after-tax from the sale of the property. Lets assume that you will owe 20% to capital gains and depreciation recapture taxes and 7% to sales and closing costs. In order to net $198,800 after-tax, the sales price of the property 16 years from now should be $252,500. If we assume a conservative average property appreciation rate of 2% (less than the rate of inflation), that would mean that we need to acquire a property today for about $184,000. Related: College Tuition Hacks: 9 Alternative Ways to Pay for Schooling Now that you know our target purchase price, you can acquire the property with 25% down a 30-year mortgage for the rest at 5% fixed. (Note: You could get a 15-year mortgage here instead, but it would force you into a higher payment and would not provide enough flexibility in the event any detours that we will discuss later happen along the way.) So your initial investment into this earmarked asset tuition plan is about $48,000. Next, in order to get this property free and clear in 16 years, you will need to make $407 in extra principal-only payments in addition to your regular mortgage of $987. Lets assume that the property conservatively produces $170 per month in positive cash flow. That means you would need to contribute $237 per month from your income savings to get this property free and clear by the time your daughter is ready to attend college. So essentially, a latte and a half a day to fund four years of college for your childnot a bad bargain! Now lets look at the 10,000 ft view. When you acquired the property, you invested $48,000 into the deal, and then you contributed $237 per month for 16 years for another $45,500. So, without going into complicated time-value-of-money calculations, you invested $93,504 and managed to fund $198,000 worth of tuition cost in 16 years without exposing yourself to the bipolar whims and sequence of return risk of the stock market. Also, lets not forget that our assumptions on property appreciation rates were very conservative. If the property you acquired was located in Houston, where the historical appreciation rate is 3.23%, the value of your property 16 years later would be closer to $300,000, which means you could fund a tuition and a half!  The Cash Flow as You Go Strategy If you dont want to earmark a property for the purposes of funding college education and you plan on building a substantial real estate portfolio, you could use the alternative Cash Flow as You Go strategy. With the Earmarked Asset Strategy, you fund college tuition from your balance sheet. With this strategy, you look at tuition cost as an annual expense in the year its due, and you fund it from your income statement. For instance, the cost of tuition for Year 1 is $46,124, Year 2 is $48,430, Year 3 is $50,851, and Year 4 is $53,394. So, instead of purchasing an asset that when liquidated will produce enough proceeds to cover the entire cost of tuition, we would build a portfolio that would produce the required income to cover the tuition expense in each of the four college years. The principal difference is that after you fund college, you still own the assets and can use them to fund other important financial goals. Related: Parents: Stop Contributing to 529 Plans for College. Use This Superior Method Instead. The average cost per year of $49,500 is the starting point to determine the value and makeup of your portfolio. We need to build a portfolio that in 16 years time could produce $49,500 in income to cover the college tuition expense. Assuming a free and clear yield of 6% and a conservative property appreciation rate of 2%, we would need to first acquire a portfolio worth $600k now and get it free and clear in 16 years so that on the first year of college is worth approximately $825,000. Again, assuming a 25% down payment on those purchases, were looking at around $150k in capital required to build this portfolio and deploy this strategy. Obviously, in this scenario, were not just solving college tuition but the whole financial picture puzzle. If we can build a real estate portfolio that can fund $50k a year for tuition for four years, we are also creating $50k in passive real estate income toward your retirement income goals. In Conclusion Thoughtful real estate investments can be an excellent vehicle to fund college tuition for your children without the sequence of returns risk and volatility of the stock market. First, you quantify the tuition funding goal and get very specific about what it will take to accomplish it. Once youve done that, you can earmark a specific property to fund tuition, pay it off in the time available until college starts, and liquidate it that year. Or you can look at tuition as an annual expense and build a portfolio that will create sufficient income to cover it as it arises.  Will you be using either of these strategies to fund your kids schooling? Comment below! https://www.biggerpockets.com/renewsblog/fund-college-tuition-real-estate-investments/ Most consumers do not grasp the difference between the price and the value of a product or service. Price is simply the amount of money paid or charged for something. When we focus on price, we are focusing on the short-term acquisition of a product. Value, on the other hand, focuses on the long-term aspect of the purchase.

Price is what a buyer spends, and value is what they receive in the transaction. When a buyer has received more value from a product than what they spent, this purchase is viewed as possessing great value. If a buyer values your product and can find a solution to his problem with your product more than he values his money, then he will purchase your product. People who focus on cost focus on the total cost of ownership, but people who focus on value focus on the total picture and how the product will create a solution. Now, how can we compute value in real estate and specifically multifamily real estate? There are basically three methods of calculating real estate value: the cost approach, the sales approach, and the income approach. The sales approach is widely used in valuing single family homes, and the cost approach is utilized for properties that have few comps and for new properties (such as a church or school). Lets focus on the income method, which utilizes the net operating income and cap rates to determine the propertys value. This is by far the best method to analyze apartments. Hyperbolic Discounting Before we dive into analyzing the value of a multifamily property, I would like to discuss the term hyperbolic discounting and why I think a significant amount of investors shy away from investing in multis. I was introduced to this term by Gary Keller while reading the book The One Thing, and hyperbolic discounting states that the farther away a reward is, the less motivated an individual is to achieve it. If I have a choice of earning $100 in two weeks or earning $500 in 18months, most people will choose the present reward over the future reward overwhelmingly. This impulse of instant gratification is becoming evermore popular within our society. This may explain why strategies such as wholesaling and fix and flipping are extremely popular to investors. These strategies employ much shorter time horizons than multifamily investments. A wholesaler can earn a profit in a matter of weeks, while a multifamily investor usually needs to dedicate a much longer time horizon to execute his business plan to generate his return. There are other challenges that investors encounter when deciding upon multifamily investments, such as lack of capital or lack of experience, but I feel that not being able to focus on the long-term dissuades many investors from multifamily investing. I sometimes wonder if our society is losing the willpower and the persistence to see things through. If you understand the value and the various benefits that multifamily offers, the decision of delayed gratification will be a no-brainer. So what are the benefits of multifamily, and how do we determine the value?  Related: The 4 Phases of a Real Estate Cycle (& When to Buy a Multifamily for Maximum Profitability) 6 Benefits of Investing in Multifamily Real Estate Here is a list of benefits: Cash flow.Apartments generate monthly income, what I like to refer to as wallet money. I compare cash flow to dividends paid by stocks. The money rolls in every month.Control.You are the captain of your own ship. You have the ability to control every decision that affects your investment.Tax advantages.Its not what you make, its what you keep thats important, and real estate offers tremendous tax benefits. Why would the government create advantages for this tax class? The government realizes it does not have the ability to deliver affordable housing, and by offering these benefits, it is trying to stimulate the private sector to step in and fill the void.Economy of scale:This is a huge advantage when trying to scale your business. I find it much easier trying to collect rent from 30 tenants in my apartment building rather than running all across the city to collect from my single family homes. It is easier and more cost effective to have more units under one roof.Ability to force the appreciation: The value is not as reliant on comps as it is your ability to increase the value through growing the NOI.Velocity of money: This refers to the ability to refinance a property, withdraw the equity, maintain control of the asset, and invest the refinance proceeds into another property. Banks are the ideal example of velocitizing money. They borrow funds from their customers and lend the proceeds out to individuals looking for loans. The faster the money moves, the wealthier you become.Multifamily Valuation: How to Calculate Value in Multifamily Investing Now that youve seen the incredible benefits that the multifamily space provides, how do you calculate value? In multifamily investing, it is all about the net operating income (NOI) of the property and the fact that the investor is purchasing the property based on an income stream. Let me provide you with a few definitions: Operating Expenses Costs that are incurred to maintain and run a property. Some examples include trash, snow plowing, and pest control. Capital Expenditures An expenditure for an asset that will improve or extend the useful life of an existing asset for a period to exceed one year. Some examples include water heaters, driveways, roofs and A/C units. I like to set aside $250 per unit per year in a cap ex account to address these repairs. You may have to set aside a larger amount, depending upon the age and condition of the property. The cap ex figure falls below the net operating income, so it does not affect the value of the asset, but it will certainly affect your cash flow, i.e.the money you put in your pocket! Net Operating Income Annual income generated from a property less total operating expenses. Cap Rate The rate of return on an investment property based on the income. Cap rates are specific to a market and are affected by the type of property class (A, B, C, D) you are investing in. A broker should be able to tell you the cap rate in his market.  Property ClassA Properties: Newest, shiniest asset. They contain many amenities and cater to white-collar workers. Expect low cap rates, around 2-4. This class of asset is poor at cash flowing but has the ability to appreciate greatly. I tend to think that investors choose A properties to maintain their wealth, not create it.B Properties: Built within the last 20 years, this class caters to a mix of white and blue-collar workers. This type of property may show a bit of deferred maintenance, but overall, it has a nice mix of cash flow and potential appreciation. Look for cap rates around 5-7.C Properties: My first real estate brokers defined C properties as crap properties, but loved their ability to generate substantial cash flow. I tend to agree with his candid analysis. These properties are usually 30+years old and have deferred maintenance issues. Cap rates hover between 8-10 on these properties.D Properties: The lowest class of property. They are usually located in inner cities where its difficult to collect the rent and vacancy rates are high. These properties are highly management intensive, and the tenant base is often difficult to deal with. Investors get lured into investing in these properties due to the low prices, but soon realize they got more than they bargained for. The goal is to increase the NOI by either increasing revenues or by decreasing expenses. You are trying to force the appreciation of the asset by increasing the NOI. The term that is thrown around to accomplish this task is reposition. When you reposition an asset, you are adding value by changing the appearance of the property or the operations of the property, all to increase the NOI. You are focusing on the value-adds to a property. Related: The #1 Thing Newbies Should Do to Get Started With Multifamily Investing Example of a Successful Multifamily Reposition Let me give you a quick example of a reposition on one of our assets and different types of value-adds we instituted. We purchased a property that had rents that were well below market, and many units that were vacant. Our goal was to address desperately needed deferred maintenance, while filling the vacant units. We eventually filled all the vacant units and increased the rent rates on the current tenants from $450 per month to $625 per month. In a span of 12months, revenue exploded from $53,000 per month to over $90,000 per month. In this example, we were able to increase the value of the property from $4.1 million to just over $6.3 million in only 12months! Examples of Value-Adds Potential value-add items might include: Adding upscale touches, such astwo-tone paint and upgraded kitchen floorsOfferingamenities, such as a fitness center or clubhouseInstituting Ratio Utility Billing System (RUBS)Changing the zoning on a property to a more favorable useGenerating new sources of revenue, such as laundry, pet fees, late fees, application fees and storage feesRenovating a property to allow the owner to increase rentsIncreasing the quality of the tenant baseRepositioning a C Property into a B property All of the value-adds listed above need to focus on either increasing the revenue or decreasing the expenses. If you decide to install granite countertops, but you realize that this upgrade has failed to increase revenue, this would NOT be a value-add. One of the biggest mistakes investors make is to over-improve a property without focusing on the ability of the improvement to increase revenue. (Ive done that a couple of times. OUCH!) This is the beauty in multifamily real estate. You have the ability to increase the value of your asset by employing sound management principles to increase the NOI, thereby increasing the value.  How to Calculate Multifamily Value Using Cap Rates Now lets tackle how you calculate the value of a property using cap rates. You would take the NOI of a property and divide it by the cap rate. NOI/Cap Rate = Value For instance, if the property had an NOI of $150,000 and the cap rate was 6, the property value would be $2,500,000 (150,000/.06). If the NOI increased to $180,000, the value would increase to $3,000,000. A $30,000 increase in NOI generated a $500,000 increase in value. Cap rates have an inverse relationship with market value. When cap rates compress, as we are witnessing in the current real estate market, the value increases and vice versa. Its fantastic when you own property and cap rates are falling, but a real bummer when you are trying to invest. The formula for cap rates is: NOI/Price= Cap Rate For example, if the property had an NOI of $50,000 and was listed for $500,000, then the cap rate would be 10 ($50,000/$500,000). Our strategy is to purchase assets based on actual numbers. We ask the seller to provide us with the last 12months of income and expense figures, as well as the rent roll. Once you purchase on actuals, your job is to go to work on the NOI. In life, its not what you buy but what you pay that is critical to the success of any investment. My goal in this article has been to describe what value is, why some investors are hesitant to jump into multifamily investing, the benefits of investing in this asset class, how to analyze a multifamily property and how to implement value-adds to an investment. Remember, at the end of the day, its all about the income versus the expenses.  Related: Thinking About Buying a Multifamily? STOP! Wait Until You Read This! Your Task Decide nowthat you are ready to invest in apartments. Seek out websites, such as BiggerPockets, to begin your education. Immerse yourself in podcasts and books that focus solely on multifamily investing. Learn how to properly underwrite (another fancy word for analyze) deals. Begin to visit websites that list multifamily properties, such as Loopnet, Costar, and Realtor.com, to become familiar with your market and the players in the market. Start networking with these individuals and ask them to start sending you deals to analyze. Expect to receive subpar deals in the beginning, but dont quit. Tell them why these deals dont work for you, and continue to analyze more deals. Formulate a business plan and strategy on how you will create value once you begin investing. Were republishing this article to help out our newer readers. Investors: Do you choose to invest in multifamily real estate? Why or why not? Any questions about the valuation process? Leave your questions and comments below! https://www.biggerpockets.com/renewsblog/2016/07/06/multifamily-real-estate-value/ My partner and I have acquired and leased hundreds of rental units. As co-owner at my organization, I still have the final say on approving rental applicants. As much as I want to delegate the task, I am aware it is of pretty high value. Having a great tenant in your property is crucial. A troubled one whois constantly late on payments and complaining about dings on the refrigerator can be a headache. A troubled tenant can eat up your cash flow if theyre not paying and you have to evict and replace them.

Leasing Agent I have an in-house leasing agent who handles collecting the paperwork and necessary documentation from rental applicants. The needed documents include the most recent three pay stubsor current lease and bank statements (if self employed). Once all this is submitted, the agent starts the underwriting process. Be sure to obtain all the necessary documentationfrom the prospect. It is important that you have a clear picture of the prospects history to verify they are qualified to pay rent your properly. If they are not willing to provide all the information, then move on.  Related: 7 Types of Tenants Ill Never Rent to Our Criteria Criteria for screening tenantscan vary depending on what class of property youre in. For example, with a C class property, you may allow 600 credit score tenants, and with an A class require a minimum score of 700. I am mostly dealing with the working class. These professionals tend to have just an OKcredit score. That is the reason why they are paying $700 to $800 in rent. I run their credit through the software Propertywareto make sure there are no outstanding balances from utility companies or judgements from landlords. My tenants must produce gross 3x the monthly rent. This is by far the most important factor in approving a tenant. If they dont have that, they must have a co-signor who does. Additional criteria include having no prior evictions within seven years of the date theyre applying for the home, having at least one year on the job (or proof of prior job stability), and having no felonies within the past five years. Stick to It It is always best to remain objective when underwriting rental applicants. If they do not make enough income or have been at their job only two months, then you simply have to move on. You want to stick to your criteria because you want to treat every applicant the same.  Related: The 11 Most Common Questions Asked by TenantsAnswered Final Approval I am an optimistic person, but Ive seen some interesting stuff in my days of underwriting tenants. I was almost fooled by tenants having a friend pose as their landlord and submitting fraudulent pay stubs. When I get the file from the leasing agent, I look for red flags that may have been missed, such as fraudulent pay stubs. Then I start taking a look at income, landlord references, income, etc. To date, I have not had to evict a single tenant I placed, and I plan to keep it that way. Were republishing this article to help out our newer readers. What is your underwriting criteria? Has it changed over the years? Leave your comments below! https://www.biggerpockets.com/renewsblog/underwrite-rental-applications My partner and I have acquired and leased hundreds of rental units. As co-owner at my organization, I still have the final say on approving rental applicants. As much as I want to delegate the task, I am aware it is of pretty high value. Having a great tenant in your property is crucial. A troubled one whois constantly late on payments and complaining about dings on the refrigerator can be a headache. A troubled tenant can eat up your cash flow if theyre not paying and you have to evict and replace them.

Leasing Agent I have an in-house leasing agent who handles collecting the paperwork and necessary documentation from rental applicants. The needed documents include the most recent three pay stubsor current lease and bank statements (if self employed). Once all this is submitted, the agent starts the underwriting process. Be sure to obtain all the necessary documentationfrom the prospect. It is important that you have a clear picture of the prospects history to verify they are qualified to pay rent your properly. If they are not willing to provide all the information, then move on. Related: 7 Types of Tenants Ill Never Rent to Our Criteria Criteria for screening tenantscan vary depending on what class of property youre in. For example, with a C class property, you may allow 600 credit score tenants, and with an A class require a minimum score of 700. I am mostly dealing with the working class. These professionals tend to have just an OKcredit score. That is the reason why they are paying $700 to $800 in rent. I run their credit through the software Propertywareto make sure there are no outstanding balances from utility companies or judgements from landlords. My tenants must produce gross 3x the monthly rent. This is by far the most important factor in approving a tenant. If they dont have that, they must have a co-signor who does. Additional criteria include having no prior evictions within seven years of the date theyre applying for the home, having at least one year on the job (or proof of prior job stability), and having no felonies within the past five years. Stick to It It is always best to remain objective when underwriting rental applicants. If they do not make enough income or have been at their job only two months, then you simply have to move on. You want to stick to your criteria because you want to treat every applicant the same. Related: The 11 Most Common Questions Asked by TenantsAnswered Final Approval I am an optimistic person, but Ive seen some interesting stuff in my days of underwriting tenants. I was almost fooled by tenants having a friend pose as their landlord and submitting fraudulent pay stubs. When I get the file from the leasing agent, I look for red flags that may have been missed, such as fraudulent pay stubs. Then I start taking a look at income, landlord references, income, etc. To date, I have not had to evict a single tenant I placed, and I plan to keep it that way. Were republishing this article to help out our newer readers. What is your underwriting criteria? Has it changed over the years? Leave your comments below! https://www.biggerpockets.com/renewsblog/underwrite-rental-applications |

Archives

December 2020

Categories |

RSS Feed

RSS Feed