|

In real estate, there are some rules of thumb that investors can use to quickly screen through deals to make guesses on whether to pursue them or not.

Its important to notice that I did NOT say, There are some rules of thumb that can help investors make purchase decisions. Why? Because rules of thumb are not meant to be hard and fast rules. They simply help an investor get a quick and dirty opinion on some valuable metrics. Always do a thorough, proper analysis. But regardless, these rules of thumb can come in really handy in saving you from analyzing every deal that you come across. In the video below, Ive outlined several of the most common real estate math rules of thumb so you can begin practicing them in your own analysis of properties. [embedded content] The 2% Rule (aka the 1% Rule or the 2% Test) Perhaps one of the most common rules of thumb used by rental property investors is commonly known as the 2% rule. But because its not truly a rule, I like the 2% test better. Essentially, this rule of thumb looks at the monthly rent divided by the value in a percentage form. For those who just got confused, lets make this super simple by considering an example. If a property rents for $2,000 per month, and the value is $200,000, then: $2,000 / $200,000 = 1% In this example, the property does not pass the 2% test, but it does meet the 1% test exactly. Or what if its a property that rents for $1,500 per month and costs $180,000 to buy? $1,500 / $180,000 = .8% This definitely falls short of the 1% test. Or what if the property rents for $1,500 per month but is worth $120,000? $1,500 / $120,000 = 1.25% Related: 2% Rule? 50% Rule? Heres the #1 Real Estate Rule I Use to Assess Property OK, so you get how the math works. But what does it mean? Essentially, the 1% or 2% test gives us a quick and dirty view on whether or not the property will produce positive cash flow. Of course, as its just a rule of thumb, it isnt always precise. But generally speaking, the higher the percentage, the better the cash flow. This also depends greatly on location, price, and how much the expenses truly are on the property. But either way, the rule of thumb can help an investor make some decisions on whether or not to pursue a property. For instance, I know that most properties that fall short of 1% will likely never produce positive cash flow. If its between 1% and 2%, it probably will. And if it is above 2% (which is incredibly difficult to find in todays market), Im almost positive it will. So if my real estate agent tells me that they have a perfect rental house for me to buy, I see that the purchase price is $125,000, and I find that it will rent for $1,000 per month, I can make a very quick decision and know thatmost likelythe deal wont provide cash flow because it falls short of 1%. $1,000 / $125,000 = .8% In a case like this, I probably wont spend much more time looking at the deal if I was only interested in cash flow.  The 50% Rule While the 2% and 1% rules of thumb we just mentioned can help give you a go or no-go decision on looking further into a rental property, it doesnt really tell us how much cash flow we might expect. For that, investors often rely on the 50% rule of thumb. The 50% rule states that, on average and over time, half of the income a property generates is spent on operating expenses. But what are operating expenses!? you ask. Good question! Operating expenses are all of the expenses involved with running a rental property, except the loan payment. It includes taxes, insurance, utilities, repairs, vacancy, and other metrics that leave the landlords checking account each month or year. The 50% rule can help an investor quickly estimate the cash flow of a rental property because it combines all of the expenses, except the loan payment, into one easy numberhalf. So imagine a property that rents for $2,000 per month. The 50% rule says that half of this ($1,000) will be spent on expenses. This means were left with $1,000. But then we need to make a mortgage payment (unless you paid cash for the property). With the $1,000 remaining, lets say the mortgage payment was $600. How much do you have left? $400. $2,000 x 50% = $1,000 $1,000 $600 = $400 The remaining value, or $400, is your estimated cash flow. Of course, that 50% estimate on operating expenses can vary wildly depending on the property. In some areas, taxes and insurance might be incredibly high, but in other areas, it might be much lower. Some properties require that the landlord pay all of the utilities, where other properties allow the tenant to pay their own. These (and other) property-specific details demonstrate the weakness in the 50% rule. But although inherent weaknesses do exist, the 50% rule does have value! When you are looking at a property that rents for $1,200 per month, and you know the mortgage payment would be around $1,000, you can almost guarantee that the property WONT produce a positive cash flow. Why? Because $200 is not a lot of room for all those expenses. $1,200 x 50% = $600 $600 $1,000 = -$400 The 50% rule helps keep real estate investors in check and reminds us that there are numerous expenses that add up over time! Yes, a new roof is only needed every 20 years, but if you divide a $10,000 roof into 240 months, that roof is actually costing you $42 every single month! These operating expenses add up, and as most investors have seen, they tend to settle around 50% given a long enough time frame.  The 70% Rule The previous couple rules of thumb were designed to help rental property owners. But what about house flippers or wholesalers? For them, the 70% rule can be helpful in determining just how much to pay for a property. The 70% rule states that the most you should pay for a potential flip is 70% of the after repair value, or ARV, which is what it would sell for when its all fixed up, minus the repair costs. Heres an example. If a home would sell for $300,000 all fixed up, and the property needed $50,000 worth of work to get it there, then: $300,000 x 70% = $210,000 $210,000 $50,000 = $160,000 According to the 70% rule, the most someone should pay for this property would be $160,000. But there are problems with the 70% rule. This rule of thumb assumes that 30% of the ARV will be spent on holding costs, closing costs (on both the buyers and sellers side, such as commissions, taxes, attorney fees, title company fees, and more), the flippers profit, and any other charges that come up during the deal. This works well in many markets, but it has some severe limitations. For example, the 70% rule doesnt work as well for a property where the ARV is low, such as $50,000. As mentioned earlier, the 30% deducted from the ARV includes the holding costs and closing costs, as well as the profit the investor or flipper wants to make. However, 30% of $50,000 is $15,000. So following the 70% rule, all the fees, costs, and profit add up to only $15,000. If the fees and holding costs were to total $10,000, that would leave just $5,000 in profit for the house flipperand I dont know any house flipper who will take on the risk of flipping for just $5,000. Related: Check out the 70% Rule Calculator from BiggerPockets! So following the 70% rule, a flipper or wholesaler would pay far too much for the property in this case. An investor flipping houses at this level might require far less than 70%perhaps 50% or even lower. A similar problem with the 70% rule exists for more expensive properties. The 70% rule would dictate that a home with an ARV of $700,000 that needs $50,000 worth of work should produce a maximum allowable offer of $440,000. However, in most markets, finding a $700,000 property for $440,000 is simply not feasible. A person who sticks exclusively to the 70% rule will likely never find a good enough deal to ever wholesale or flip a single property. In this case, 80% or even 85% might be good enough. Furthermore, some investors may spend more or less on fees and costs because of their particular life situation or location. For example, in some states, purchasing a home may require $3,000 in closing costs, while in other states, it might be $6,000. Some investors may have a real estate license, which saves them tens of thousands of dollars in commissions, whereas other investors may need to pay commissions when they sell. So, how should the 70% rule be valued? Very carefully. Its a quick and dirty way to guesstimate the approximate amount you should pay for a property. But as with all rules of thumb, no concrete decisions should be made unless youve run a real analysis on a property. ______________________________________________________________________________________  Looking for a plan to achieve financial freedom in just five to 10 years? Even with a full-time job, median income, or negative net worth, you can accumulate a lifetime of wealth in a short period of time. Set yourself up for life with this bestselling book, written by the CEO of BiggerPockets, Scott Trench! Pick up your copy from the BiggerPockets bookstore today! ______________________________________________________________________________________ Do these calculations make sense? Do you have follow-up questions about any of the rules? Ask me in the comment section below! https://www.biggerpockets.com/blog/real-estate-investing-rules-of-thumb

0 Comments

BiggerPockets Podcast 330: How to Ditch Distractions and Get WAY More Done With Cal Newport5/16/2019 Incredible show alert! You dont want to miss this one: Brandon and David sit down with bestselling author Cal Newport (who wrote So Good They Cant Ignore You: Why Skills Trump Passion in the Quest for Work You Love, Deep Work: Rules for Focused Success in a Distracted World, and so on) to discuss just what makes high performers different than the rest.

Cal shares incredible insight based on his research as a professor at Georgetown University, including how boredom can serve a very useful purpose, how to improve your focus to master your craft, and how building career capital can open doors to the life youve always wanted. Cal also shares life-changing advice on how starting the day in monk mode can supercharge your productivity, how to set better expectations with team members, and how to rebuild your digital life in 30 days. This episode is so good youll feel guilty you didnt have to pay.Download it today! Click hereto listen on iTunes. Listen to the Podcast HerePodcast: Play in new window | Download Subscribe: Apple Podcasts | Android | RSS Watch the Podcast Here [embedded content] Help Us Out! Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it! This Show Sponsored By  Fundriseenables you to invest in high-quality, high-potential private market real estate projects. Im talking anything from high rises in D.C. to multi-families in L.A. institutional-quality stuff. And each project is carefully vetted and actively managed by Fundrises team of real estate pros. Fundriseenables you to invest in high-quality, high-potential private market real estate projects. Im talking anything from high rises in D.C. to multi-families in L.A. institutional-quality stuff. And each project is carefully vetted and actively managed by Fundrises team of real estate pros.Their high-tech, low-cost online platform lets you track the progress of every single project, and keep more of the money you make. Oh, and by the way, you dont have to be accredited. VisitFundrise.com/biggerpocketsto have your first 3 months of fees waived. Deep Dive Sponsor  Enjoy all the benefits of Real Estate Investing without all the headache!Rent to Retirementis your partner in achieving financial freedom & long term wealth! Retire on your terms & timeline by investing in passive income properties! Enjoy all the benefits of Real Estate Investing without all the headache!Rent to Retirementis your partner in achieving financial freedom & long term wealth! Retire on your terms & timeline by investing in passive income properties!Learn more by visitingrenttoretirement.comor call 307 421 4049 Fire Round Sponsor CBRE provide a robust range of investor services designed to drive real estate performance and asset value.  They are the number 1 agency lender. They are the number 1 agency lender.Lock in your credit today by visiting their site: cbre.com In This Episode We Cover:Cals storyImprove your focus and remove distractions to increase productivityHow to combine deep work with shallow work to stay mentally energizedBuilding career capitalyou can then invest to build a better lifeWhat successful people do that unsuccessful people dontHow to set better expectations with team membersHow to start your day in monk mode and be insanely productiveHow to give your hours a job and make time work for youHow to use boredom to recharge and motivate youHis thoughts on social media and how it can rob you of timeTaking the information youre learning and letting it sink inDetox and rebuild your digital life in 30 daysAnd SO much more!Links from the ShowBooks Mentioned in this ShowTweetable Topics:Accessibility is not as important as we think. (Tweet This!)Time alone with our own thoughts is crucial. (Tweet This!)Connect with Cal https://www.biggerpockets.com/blog/biggerpockets-podcast-330-ditch-distractions-cal-newport/ Do you want to know how to get your business noticed by reporters and generate positive press? Todays guest has made a career out of doing just that. In this episode, he teaches you exactly how to make a splash through innovative (some would say crazy), outside-the-box techniques.

Brent Underwood is a creative marketer whos done publicity for musical artists, best-selling authors, and his own projectsincluding a ghost town he bought and plans to turn into a high-end resort. Today, Brent tells us how his career began with a cold email and how that led to him working with some of the most talented writers and marketers in the country. Brent also reveals how he gets into the heads of reporters and editorsand how you can do the same. He explains what a handle is, and why you need one to get your message to spread. And you wont want to miss the most important lessons Brent learned after opening his own hostel in Austin, Texas, and how a goat helped boost business. This show is jam-packed with information that will help you generate buzz and get yourself in front of more clients and customers. Download it today, and subscribe to the BiggerPockets Business Podcast so you wont miss an episode! Click hereto listen on iTunes. Listen to the Podcast HerePodcast: Play in new window | Download Subscribe: Apple Podcasts | Android | RSS Watch the Podcast Here [embedded content] This Show Sponsored By  WizeHireis an online recruiting service that fuses recruiting software with the personal service of a hiring coach to help you find the best candidates for the job. They do all the heavy lifting for you so you can stay focused on whats important. WizeHireis an online recruiting service that fuses recruiting software with the personal service of a hiring coach to help you find the best candidates for the job. They do all the heavy lifting for you so you can stay focused on whats important.VisitWizeHiretoday! Mid-Roll Sponsor Fundriseenables you to invest in high-quality, high-potential private market real estate projects. Im talking anything from high rises in D.C. to multi-families in L.A. institutional-quality stuff. And each project is carefully vetted and actively managed by Fundrises team of real estate pros.Their high-tech, low-cost online platform lets you track the progress of every single project, and keep more of the money you make. Oh, and by the way, you dont have to be accredited. VisitFundrise.com/bpbusinessto have your first 3 months of fees waived. In This Episode We Cover:Marketing career and Tucker Max storySending a blind emailThe type of marketing that his company usesThe power of creating an origin storyThe story of having a goat in the hostelCost benefit marketingThe power of word of mouthThe story behind the 300-acre ghost townHis thoughts on paid marketingAnd SO much more!Links from the ShowBooks Mentioned in this ShowTweetable Topics:If you want people to talk about your project, you have to give them something to talk about. (Tweet This!)Word of mouth is the only thing that will sell a product for the long term. (Tweet This!)Connect with Brent https://www.biggerpockets.com/blog/biggerpockets-business-podcast-03-attract-media-attention-turn-publicity-profit-brent-underwood Rental Owners Everywhere Should Be Concerned About California's Push for Rent Control--Here's Why5/15/2019 Its not just the weather that travels from west to east across the continental United States. Everything from Tony Hawks skateboarding to the humble Cobb salad got its start in California, eventually drifting eastward.

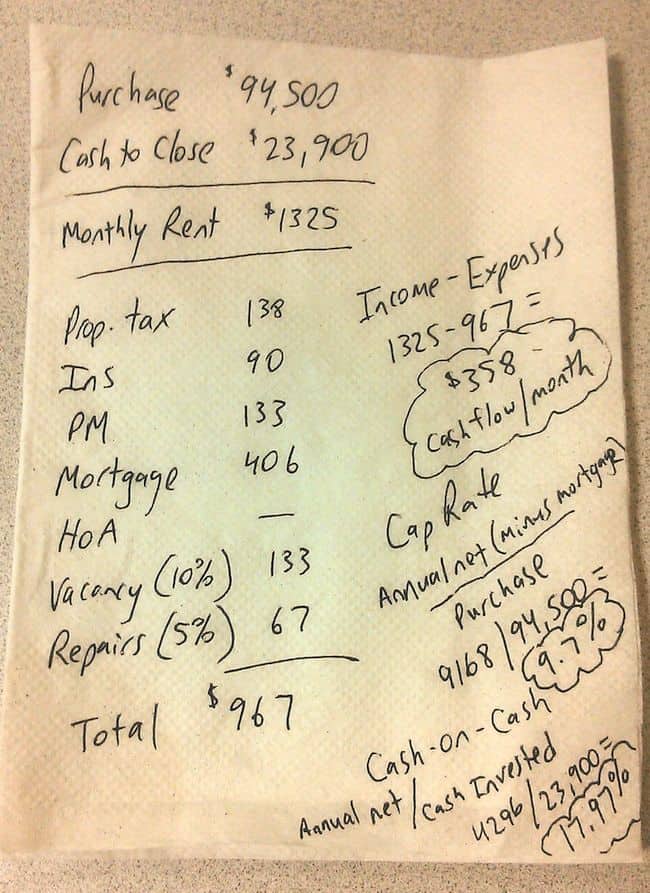

For better or worse, the West Coast has a long history of setting trends and then spinning them out across the country. More recently, California has been pushing its historically low cap rates into neighboring states like Arizona and Nevada, much to the delight of incumbent local investors. The burning question for rental property owners today is: will statewide rent control regimes be the next West Coast export? Oregon Leads the Way in Rent Control In unlikely fashion, its actually Oregon thats leading the charge with a first-in-the-nation statewide rent control bill passed earlier this year. Senate Bill 608 was signed into law in February and immediately capped annual rent increases at the consumer price index (CPI) plus 7 percent. The only exemptions are for buildings less than 15 years old and subsidized below market rentals. In practical terms, that means most Oregon landlords will be limited to raising rents, on average, a maximum of 8 to 10 percent per year. Notably, the new legislation does not include vacancy control, so Oregon rental property owners will retain the right to set rents as they wish once an existing tenant vacates. Whats perhaps most notable about the recent action in Oregon is that while the legislation potentially sets a dangerous precedent for property owners, its also relatively mild in its actual restrictions. Even 8 percent annual rent increases can add up fairly quickly, and with compounding, can result in a 26 percent bump in just three years. All things considered, the result could have been worse for Oregon property owners. Time will tell if the new regulation delivers enough stability to the rental market to short-circuit support for more drastic rent controls. Related: 6 KEY Attributes that Affect the Risk Level of a Rental Market California Starts Down Two Paths to Rent Control Not to be outdone by its slightly damp neighbor to the north, California legislators are now proposing a slew of new regulations aimed at protecting existing tenants and increasing the housing supply across the nations most populous state. AB 1482 advanced out of assembly committee on April 25 and promises to cap annual rent increases at CPI plus 5 percent statewide, except where more restrictive local rent control laws remain in place. In areas with existing rent control, including Los Angeles, San Francisco, Oakland, and other cities, the more restrictive local regulations would continue to prevail. If AB 1482 becomes law, rental property owners from San Diego to Yreka will see their ability to increase rents for existing tenants capped at roughly 6 to 8 percent per year, with no exceptions for single family homes or newer construction. Of all the rent-control or anti-rent gouging bills currently being considered by California lawmakers, AB 1482 is probably the one with the best prospect of becoming law. Taking a slightly different tack, the California Senate is currently considering SB 50, which would wrest control of certain residential zoning regulations from local cities and counties. Its a complicated package of legislation thats designed to force higher density housing construction near rail and bus transit corridors. While there are notable carve-outs for smaller cities and beach towns, many of Californias urban centers would see a significant uptick in higher density new construction near transit. Under a separate provision, communities throughout the state would also be unable to prevent the further subdivision of many existing duplexes and single family homes into three- and four-unit properties.  Whats Behind the New Legislation? Taken together, AB 1482 and SB 50 can be seen as roughly representing two camps of thought regarding solutions to the continuing housing affordability crisis that grips not only California, but also an increasing number of urban areas across the country. On the one side, organized and well-financed tenant advocates are beginning to gain some modest ground in their efforts to bring rent controls to increasingly large swaths of the country. Its likely they will succeed in California, in one form or another before the end of the 2020 election cycle. Early results from the legislative push for more rent control in California will certainly influence what happens in other parts of the country, where rents are rising and tenant rights groups are gaining political influence. On the other hand, housing advocates (and developers) are also gaining traction, advancing the argument that restrictive land use policies are a significant source of upward pressure on housing costs, especially on the West Coast. Many California communities are so united in their distaste for residential growth and its negative perceived impacts on schools and traffic that it has become nearly impossible to get approval for even fully conforming new housing developments. This is likely to change significantly over the next few years, as a direct result of SB 50 or from whatever similar bill rises to take its place should SB 50 falter this year. Taken together, there is a decent chance that this two-pronged approach may yet move the California housing market back toward a more sustainable balance in time to avoid more draconian restrictions on rental property owners. Six years of steadily rising rents and a continued shortage of new home deliveries has resulted in a pressure cooker environment around all things housing related up and down the West Coast. Letting some steam out now may be the best hope for avoiding a major blow up. Related: What Property Owners and Managers Need to Know about Risk Management Emerging Risks for Rental Investors Changing populations and emerging legislation nearly always bring new risks (and rewards) to forward-thinking real estate investors. Lets take a closer look at a few key implications of the forces at work in California, on the assumption that they will eventually impact other markets around the country. First, lets acknowledge that California has not been the most lucrative place to own rental property if youre primarily focused on current income. Cap rates are notoriously low in core urban areas along the coast and are only slightly better inland. If you bought rental property in California from 2009 to 2015 and youve been able to raise rents to market, your yield is probably a bit more respectable now and youve undoubtedly also seen significant appreciation. If you bought more recently or have not raised your rents, its a different story. If your current rents are close to market, then the annual increase caps contemplated under AB 1482 probably wont hurt you much in the near future, given that market rents have now leveled off in nearly all parts of the state. Ironically, its the investors who had the option but chose not to raise rents in recent years that will bear much of the burden of the new legislation in the short run. This may be perhaps the most prescient lesson to landlords in other states, where rent control initiatives are just beginning to gain visibility. (Read: get your rents closer to market while you still can.) What lies ahead is somewhat uncertain. It may take years before we know how the emerging rent control regime will impact investor demand, cap rates, and associated valuations.  Some questions you may want to ponder include: Will the trend of California residents chasing yield beyond the states borders accelerate?Will Chinese and other international investors find other more promising U.S. markets with uncapped upside?How will California (and Oregon) landlords react to the next economic downturn? Will they resist aggressively lowering rents, knowing theyll be restricted on increases once the economy starts growing again? I dont have the answers, but these are all questions worth asking. Savvy investors know that you buy based on where you think the market (and regulation) is goingnot where it is today. Change Brings New Opportunities to Rental Investors, Too While AB 1482 is full of risks for rental investors, SB 50 is mostly opportunity. The express intent of the legislation is to jumpstart residential development and increase the supply of new market rate and affordable housing units as quickly as possible. For investors with an appetite for development, it may be worth taking a hard look at some of Californias transit corridors for new projects. Picking up an existing single family home or duplex at a 4 percent cap rate today might be worthwhile, especially if youre soon able to re-entitle the property for a much larger apartment building. There may also be incidental opportunities to make other real estate plays based on the long-term assumption of increased density in certain areas. For example, neglected or under-utilized commercial properties or even local operating businesses in these areas might see significant upticks in appreciation once higher-density construction breaks ground. For investors outside of California, you could apply a similar long-term buy and hold strategy to areas near public transit in other parts of the country. If Californias legislative approach successfully eases the housing affordability crisis, then other states may eventually follow suit. Promising investing opportunities may present themselves all along the most notoriously congested commuter corridors. Underneath the groundswell in support for measures like SB 50 is the dawning realization that adding new housing units far from where the jobs are is ultimately counterproductive. California is showing an intention to blaze a new path by simply bypassing local control to allow the market to deliver even more housing units on top of existing density. A similar dynamic may already be shaping up in other urban cores in the United States, and state legislators around the country are surely paying attention to whats happening in California. 2020 May Be the Inflection Point If AB 1482 and SB 50 fail to become law this year, the underlying market forces driving the legislation arent likely to go away. SB 50 itself is the reincarnation of a similar statewide initiative that died on the vine in 2018. If these bills dont make it over the finish line in 2019, we can expect a new push for similar regulations on both fronts to reappear during the 2020 election cycle. Political engagement is likely to be high among all camps in 2020, which may help provide rental property owners across the country an early glimpse of whats in store for other markets where housing affordability is nearing a tipping point. Resources: https://leginfo.legislature.ca.gov/faces/billTextClient.xhtml?bill_id=201920200AB1482 https://leginfo.legislature.ca.gov/faces/billTextClient.xhtml?bill_id=201920200SB50  How do you think rental regulations will pan out in California and elsewhere? Id love to hear from you in a comment below. https://www.biggerpockets.com/blog/rental-owners-concerned-rent-control Rental Property Numbers So Easy You Can Calculate Them on a Napkin (With Real-Life Example!)5/15/2019 The numbers. In this industry, you must love the numbers. Love them like they are part of you. For good or for bad, til death do you part, never leave the numbers.

One of the biggest questions Im asked is how I go about evaluating a property once I find it. What do I do, what do I look at, how do I know if its the one? There are several things I do and look at with any new potential property, but the most important is the numbers. If the numbers arent good, I walk. Save yourself some time, and before you do anything else, run the numbers and see if they work. If they dont, awesomeyou didnt waste time on other stuff. What numbers do I run? Well, what should any investor care most about? Cash flow. What determines cash flow? Income and expenses. Simple. People make running numbers out to be so complicated sometimes, its a no wonder more people arent involved in real estate. In fact, the numbers can be one of the easiest parts of shopping for a property. Unless you are a trained psychic on the crystal ball, then predicting appreciation may be easier for you than estimating cash flow. Ready? 4 Steps to Calculate Your Rental Property Numbers (on a Napkin)1. Figure out the monthly income (gross income). This will either be rent the current tenants are paying, the asking rent (confirm this number is realistic), or if you have neither of those, you can talk to a local property manager or real estate agent who can give you a market rent value for the property. Related: How to Use Price-to-Rent Ratio to Analyze a Location 2. Calculate the monthly expenses. These include property taxes, insurance, property management fee (if applicable), mortgage or financing (if applicable), homeowners association fee a.k.a. HOA fees (if applicable), vacancy, and repairs. Dont forget vacancy and repairs! They are a real part of any property investment, and they can drastically affect the cash flow. Still, so many people dont think to include them in the expenses. Property Taxes: Look on Zillow or another online source for the most recent annual tax amount and divide by 12.Insurance:Get a quote from an insurance provider.Property Management Fee:Usually around 10% of the monthly rent.Mortgage: Use an online mortgage calculator, like the one here on BiggerPockets, to calculate the monthly payment. Confirm with your lender what your down payment and interest on the loan will be to ensure you are using accurate numbers for your calculations.HOA: This can be tough to find sometimes. The seller or agent may know the number already, but if not, you will have to call the HOA of the neighborhood. If you only know the annual fee, divide by 12. Dont skip out on finding out what the actual HOA is! The HOA can absolutely kill a propertys cash flow.Vacancy: I conservatively estimate 10% of the monthly rent towards vacancy expenses. In situations where you have a rockstar property manager or your tenants are under a lease option, the actual percentage should be much less. I still use 10% no matter what just to be sure I have a conservative margin.Repairs: Again, this is an estimate, but it should not be left out. Just like with vacancy, I err on the side of conservative. If a house is a turnkey property or recently rehabbed and gets a good report from the inspector, I use 5% of the monthly rent. If the property is not in top shape, conservative could mean closer to 25%. Use your judgment on deciding what percentage to use for your estimate, but dont overestimate the quality of your property and estimate too low. 3. Subtract the monthly expenses from the monthly rent (= net income). This is your monthly cash flow. Yay! Hopefully its positive. If its not positive, run. Related: The Top 8 Real Estate Calculations Every Investor Should Memorize 4. Calculate the returns. Two numbers I want to see on any property I evaluate are the cap rate and the cash-on-cash (COC) return. Cap Rate This gives you an idea if you are buying the property at a good deal. It basically compares the return on investment (ROI) to the purchase price. The cap rate equation: Net Annual Income / Purchase Price = Cap Rate NOTE: I dont include the mortgage payment in this calculation. The lowest cap rate I would ever want to see for any property, whether residential or commercial, is 6%. The lowest I would want to see on a residential rental property in this market is 8%, and even then, there better be a good reason its that low (property in a sexy market, highly desirable area, etc.). Anything over 8%, and you are doing well in my opinion. Cash-on-Cash Return This number is how much return you are getting on the money you invest. If you pay all cash for a property, this number will be the same as the cap rate. If you are financing, this number is the most accurate way to see the actual return you are getting on your cash-in and the leverage. Here is the equation (and remember to include the mortgage payment since this one is totally focused on financing): Net Annual Income / Total Cash Invested = Cash-on-Cash Return Understand the difference? One is a measure of how good of a deal you are getting on the purchase price, and the other tells you the exact return on your money you are getting. They are the same for an all-cash buy, but can be very different for a leveraged purchase. Pro Tip: If you compare the cash-on-cash returns of an all-cash buy versus a financed buy, you may quickly see the benefit of leveraging! Way more bang for your buck! Try it out on a napkin sometime. Practice Problem, on an Actual Napkin Apply these steps to an actual property? On a real napkin? You got it. Even more fun, Im going to use a property that I bought for myself in Atlanta.  What do you think? Good deal? Absolutely! Im pocketing $358/month in cash flow (the actual number when there are no vacancies and repairs is $558!), the cap rate is 9.7%, and the cash-on-cash return is 17.97%. Not only are the returns great, but the tenants are under a three-year lease, and the property is in a great area. Score! Running the numbers on a potential rental property purchase is easy. If you can remember what numbers you need to know, it will take you no time at all to do this for every property you look at. Jot down the list of expenses on a scrap sheet of paper, fill in the numbers, and calculate your cash flow. Done. Ive done this on multiple napkins in the past. Write everything out, and look for positive cash flow. If its not there, ditch the property and move on to the next. The only trick to this version of running numbers is that the calculation doesnt include any expenses for rehabs or any work that may have to be put into a property once you purchase it. I usually only deal with turnkeys, which are fully rehabbed when I buy them, so this formula works because there is no work required on the houses. At the end of the day, numbers are just thatnumbers. The reality of a property after you buy it may give you far different numbers than what you initially calculated. For instance, Detroit. Oh, Detroit. On the surface, the numbers are out of this world. In reality, because of several key market factors, those initial numbers often turn out to be so far from reality (in a bad way). If you are a Detroit investor, rock on, and I wish you well. Its just not my thing. The point is, dont ever just go off the numbers on a property, but the numbers are an important first step in evaluating a deal. If you dont have solid reason to believe you will be getting positive cash flow consistently out of a property, dont bother with it.  Any horror stories? If you initially calculated that a property would have great returns and then the reality was something totally different, what caused it? Weigh in with a comment! https://www.biggerpockets.com/blog/2013/01/19/real-estate-math/ Learning how to calculate cash-on-cash return and when to use this equation is vital for investing success. While the equation itself is simple, the numbers that go into it are a little more involved. Investors should also understand the best applications, as well as a few of the limitations, of this common equation.

An investor came to me not too long ago seeking advice regarding the performance of his portfolio. He figured his portfolio was performing soundly, but wisely decided to seek a CPAs analysis tohelp him make investment decisions. While this investor was sophisticated, he was analyzing his returns on his current properties and returns on potential deals using the cash-on-cash metric. There is, of course, nothing wrong with using the cash-on-cash return metric; the problem arises when its the only metric, or the primary metric, used in making investment decisions. This article is going to go overthe conversation I had with this investor so that you may benefit from it. Ill discuss how to calculate the cash-on-cash return, the good qualities, the bad qualities, and how investors can use the metric to help aid investment decisions. Before we get started, lets first define what the cash-on-cash return is. The cash-on-cash return is a quick way to analyze an investments cash flow. Specifically, it will produce a percentage rate that measures the received pre-tax cash flow relative to the amount of money invested to acquire the asset. How to Calculate Cash-on-Cash Return Calculatingcash-on-cash return is simple. We simply divide the received net cash flow for the year by the amount of cash invested.  The overarching equation isnt bad at all. Its the variable, such as annual pre-tax cash flow and actual cash invested, that can become somewhat tricky.  Annual Pre-Tax Cash Flow The formula to calculate your annual pre-tax cash flow is as follows: Annual Pre-Tax Cash Flow = Gross Scheduled Rent + Other Income Vacancy Operating Expenses Annual Debt Service Lets break each of these variables down. Gross Scheduled Rent When you are evaluating a propertys performance, gross scheduled rent will be the propertys gross rents, multiplied by 12. This reflects the maximum amount of income you can expect to receive from a property. Other Income Think about all of the other earning opportunities the property may present. Will you allow pets and receive pet income and non-refundable deposits? Do you have parking spaces available? Do you get reimbursed for utilities or charge a flat rate regarding such? All of this miscellaneous income will be included in other income for our cash-on-cash return analysis. Related: Your Complete Guide to Analyzing a Property in Just 10 Minutes Vacancy If you already own the property and you are wanting to produce the cash-on-cash return to understand your propertys performance, you will want to use actual vacancy here. The actual vacancy should be measured by the numbers of days your property was vacant multiplied the daily rental rate. Essentially, this is the rental income you lost, on a daily basis, due to a tenant not being in place. If instead you are analyzing a propertys potential performance, you will want to use potential vacancy. This should always be a conservative number. You can guesstimate potential vacancy by calling up property management firms in the area or asking a real estate agent to run an analysis on how long a unit stayed on market. You will be able to generate a percentage rate of vacant days compared to the entire year. Whatever that rate is, Id go ahead and add 2%. This will help create a small buffer as you learn the ins and outs of the market and what tenants expect a rental unit to look like. For example, if a unit sat unrented on the market for 45 days, then the vacancy rate is 12.33% (45/365). Go ahead and round up to 14% for your projected vacancy rate. Now well take that vacancy rate and multiply it by the gross scheduled rent. The result will be the amount of rental income you expect to not collect due to the unit not being rented. This can also be considered your opportunity cost. Operating Expenses Operating expenses will range from insurance, taxes, maintenance, HOA and bank fees, property management, and repairs. Operating expenses do not include debt service (principal and interest), nor do they include depreciation or amortization. There are plenty of articles on BiggerPockets providing insight on how to estimate operating expenses. I recommend checking them out if you dont know how to already. Annual Debt Service For the purposes of learning how to calculatecash-on-cash return, this number will be your monthly payment to cover both principal and interest related to your loan. This does not include insurance and taxes.  Actual Cash Invested OK, now that we know how to calculate the annual pre-tax cash flow, lets figure out how to calculate the actual cash invested. Actual Cash Invested = Down Payment + Closing Costs + Pre-Rental Improvements/Repairs Lets also break each of these variables down. Down Payment This has nothing tricky to it. It will simply be the amount of money you pay as required by your lender to obtain the property. Very simple. Closing Costs Closing costs are also somewhat simple. Basically, you will add up your net closing costs associated with obtaining the property. To do this, add up all of the costs you paid (not including your down payment) and then subtract from that any seller or lender credits given to you. Pre-Rental Improvements/Repairs Remember, we really only want to use cash-on-cash return to analyze a return based on the cash we have actually invested into the property. I suggest only using pre-rental improvements and repairs because I think the cash-on-cash return should really only be utilized in the first year of ownership. More on that later. Related: NEW Annualized Total Return Estimate on the BiggerPockets Rental Property Calculator Pre-rental improvements/repairs will include anything you pay out-of-pocket to fix prior to renting the units out. This is the part where the cash-on-cash return loses some of its value, as it doesnt do a good job of analyzing returns when you are injecting more cash into the asset after renting out the property. So there you have it. I explained how to calculate cash-on-cash return in just 800 words. Is your head spinning yet? No? Good. Time to move on to the theory and application of using cash-on-cash returns. Why the Cash-on-Cash Return is a Good Metric The cash-on-cash return is a great metric and is widely used throughout the real estate industry both investors and real estate agents. The primary reason for this is due to the metrics simplicity in calculating the percentage return. The cash-on-cash return specifically drills down in the return on the capital invested. It does so by only considering returns that are driven by the propertys net cash flow. It is an essential part to value investing because it does not take into account asset appreciation. Because the cash-on-cash return is only looking at the net cash flow and comparing it to the actual amount of cash invested, its a great indicator for the effect of leverage. Using leverage will decrease your cash-on-cash return, which makes the metric a good way to measure different levels of financing. Many investors are not sophisticated enough to use things like the Internal Rate of Return (IRR) or Modified Internal Rate of Return (MIRR). These two metrics can be quite encumbering to learn and fully understand. And even though they provide much more insight, they also require much more work. On the other hand, its easy for everyone to understand how cash-on-cash returns are calculated. Its simply the physical cash you have in hand after 12 months, divided by the physical cash youve invested. Since investors can easily understand the calculation, thats what sellers and agents use when discussing potential returns on the properties they are marketing. Because of its simplicity, its also a great way to run a back of the napkin analysis. I personally use it as a screening tool when evaluating potential deals. The calculation can be run in literally 10 minutes or less and will likely get you within 2-5% of the actual return on equity in most situations. If youre analyzing hundreds of deals a week, something like the cash-on-cash return makes a lot of sense. The cash-on-cash return also allows you to easily compare different investments. You can compare rental property to lending, investing in stocks or bonds, and even starting a business. Granted, risk factors are not considered (which is a limitation well discuss in a minute), but the cash-on-cash return does allow for a universal comparison between different investments.  Why the Cash-on-Cash Return is a Bad Metric The number one limitation, in my opinion, to the cash-on-cash return is that it doesnt indicate your actual return. There are two reasons for this: (1) taxes and (2) loan pay down. Did you really think you were going to get through an entire article, written by a CPA, without discussing taxes? Your tax situation is unique to you and will greatly impact your actual return on investment. Many investors argue that your tax situation doesnt impact the assets performanceit is independent of you. Therefore, taxes should not be taken into account. However, the tax impact of investment decisions should absolutely be assessed. While your tax situation may not impact the assets performance, the assets performance will directly or indirectly impactyour tax situation. The effect can greatly increase or decrease your actual returns. For instance, lets say your annual pre-tax cash flow is $10,000, resulting in a 10% cash-on-cash return (assuming you invested $100,000). If you are in the 25% tax bracket, your after-tax cash flow is $7,500 resulting in a 7.5% actual return. Further, we have to take depreciation and amortization into account. In the example above, if your depreciation and amortization amounts to $8,000 annually, then only $2,000 of cash flow is remaining to be taxed. At the same 25% rate, our tax liability is $500. Since depreciation and amortization are phantom expenses, our after-tax cash flow is $9,500 ($10,000-$500), resulting in a 9.5% actual return. But then theres another wrinkle to all of this. The cash-on-cash return doesnt take into account the equity added from the principal portion of your loan payment. It also assumes the entire mortgage payment is an expense, which we know the principal portion of your loan payment cannot be expensed for tax purposes. As you can see, because the cash-on-cash return uses pre-tax numbers and doesnt account for principal payments, the return suggested should not be trusted. Another limitation is the simple fact that the cash-on-cash return doesnt take into account appreciation. As I stated a bit earlier, this supports the view that the cash-on-cash return is used for value investing and not used for speculation. Depending on how you invest, this could be a good or bad thing. The cash-on cash-return ignores the risk associated with investments. It doesnt take into account opportunity costs, which more sophisticated investors will find alarming. It also ignores the effect of compounding interest. The problem here is that the cash-on-cash return may make short-term investments look more appealing while making longer-term investments with a lower cash-on-cash return unappealing. If the investor were to invest in an investment that compounds (or appreciates), then the investor may be better off taking the currently smaller cash-on-cash return in the long-run.  How You Should Use the Cash-on-Cash Return Coming full circle, the conversation I was having with this investor led him to believe that the cash-on-cash return is a pointless metric. He then became anxious that he had been missing out on potentially better returns for the past several years. Related: The Definitive Guide to IRR (Internal Rate of Return) But I told him not to worry because the cash-on-cash return is a great metric if used appropriately. First, I wouldnt suggest using the cash-on-cash return to evaluate the performance of a property you have held for more than 12 months. It should really only be utilized to evaluate the first years performance or project a propertys first year performance. After that, the cash-on-cash return begins to lose its value. The reason being that your denominator (actual cash invested) will be constantly changing as you pay down the loan and make improvements and repairs to the property. A better metric to use in this case is the IRR. Second, use the cash-on-cash return as a screening tool to compare other investments. Many people claim the 1% and 2% rules are pointless, and Id agree. But everyone needs a good screening tool, and the cash-on-cash return will allow you to compare investments efficiently and effectively. Lastly, use other metrics to supplement the information that the cash-on-cash return provides you. Specifically, the IRR and the MIRR. Again, these two metrics require a bit more work but provide you with much more insight into the performance of the property. So while the cash-on-cash return certainly has weaknesses, its a great metric for value investors and serves as a solid screening tool. Using it in tandem with other metrics will provide you with plenty of information to place an offer on a property. And thats what were all about, enabling you to grow your portfolio. How often do you use the cash-on-cash return formula when evaluating properties? Any questions about this equation? Leave your comments below! https://www.biggerpockets.com/blog/2016/06/10/cash-on-cash-return-2/ Lets talk about how to deal with a tenant who abandons your property.

Before we get into the nitty-gritty of what you should do if your tenant abandons your property, you need to reduce your risk of that ever happening. You do that by having a really good tenant qualification process. Practice Prevention: Screen Tenants Well Something we do at our property management company when we evaluate tenants that you should do is check their income. Their income has to be three times the monthly rent. Call the employer to make sure that the paystub figures are accurate. Another thing you need to do is an eviction history check. If anyone has any kind of eviction on their record, in my opinion, that should be an automatic fail. This is because the likelihood of them doing that again is pretty high. Last but not least, you need to do a background check. Anyone with criminal activity from a felony standpoint or along those lines, in my opinion, you should not rent to. They just tend to come with a lot of problems. If they have minor criminal activity thats years and years old, we try and work out a deal. I suggest that you do, too. I always like to joke around and say that money speaks every language. So if someone is willing to put down three to six months of rent in advance or a large deposit, that should minimize your risk because youll have that buffer of capital. Again, give yourself the best chance before you put a tenant in that property if you want that tenant to stay and pay. Related: The Tenant Screening Process: Credit Check & Background Check [embedded content] What to Do If a Tenant Disappears Now once you have gone through that and placed a tenant in your property, its all fairytales and butterflies, right? Then after two months, they tend to disappear. Guys, its real estate and its a rollercoaster of a ride. Im here to tell you now, if you think its not going to happen to you, it probably will. So you always have to base everything on the worst case scenario. Something that I like to tell investors is underestimate your income and overestimate your expenses when youre investing in buy and hold properties. Something will always go wrong, and you need to expect that to happen. Weve placed a lot of great tenants in propertiesat least we thought they were great. But then they pack up and leave. They just disappear; they abandon the property, and they move out of state. We cant talk to them even though we call them, we text them, and we email them. Theyre just M.I.A. These things happen. Weve also had a lot of tenants that stop paying after two or three months for no apparent reason. They just stop communicating, and we have to evict. So what do you do? Do you hold a grudge and file for eviction? Go to court? Succumb to that negative energy?  Related: Tenants Bailed: Pursue an Eviction or Let It Go? When to Let That Tenant Go and Move On Look, in my opinion, there is enough crap that happens in real estate as it is. Youre dealing with people, and when youre dealing with people, youre dealing with problemsfrom employees to contractors to realtors to everyone. So I think that whenever something negative happens you should learn from the experience, let go of it, and move on as quickly as you can. You have to focus on positive energy. My point is sometimes it can be tough to be motivated in an industry where a lot of negativity can happen. So you have to feed yourself with as much positivity as you can. Holding a grudge against a tenant that vacated after three months, and trying to collect the rest of the rent, filing an eviction, and going through the court process is going to be extra costs and extra time. Time is money, guys. Its just not worth what you can potentially get from it. The likelihood of ever collecting anything is very low, so I just think that you should let it go, honestly. Get that property turned as fast as you can, re-list it for rent, and try to get another tenant in there. Learn from the mistake, let it go, and move on. When to Go After a Missing Tenant Now, if they cause significant damage to the property and a lot of capital has to be spent to turn that property around, then yes, file for the eviction. Go for second cause and hope you can get a judgment and collect something on that money. But still, move on. Its something I have done and will keep doing. I have lost $2 million over the last five years in my real estate endeavors, from tenants to employees to contractors to sour businesses. Its just the cost of doing business. As long as you make more money than you lose, youll always be ahead, right? I remember I got some great advice from a business person back home in Australia. He said, You cant go wrong making a profit. If its $1 or $100,000, it doesnt matteras long as youre making a profit. What do you think? Do you agree with me or do you disagree? Let me know in a comment below. https://www.biggerpockets.com/blog/deal-tenant-abandons-property/ To BRRRR, or not to BRRRR, that is the question

The general consensus in many real estate circles is that buy and hold investors must choose between cash flow or appreciation. If you want cash flow, then the opinion is you have to settle for second tier or tertiary markets away from major coastal cities. In this scenario, youll likely get decent to good cash flow. However, this may come at the expense of appreciation. Likewise, the thinking is that if you want significant long-term appreciation (in my opinion, this is where the real money is), then you have a better chance in tier one markets (e.g., in and around major coastal cities). In this scenario, history suggests you have a greater chance of appreciation; however, this will require you accept lower cash flowsif any! Well, I disagree. If the goal is financial independence, then I say why settle for one out of two? The aim should be to get both cash flow and appreciation! Through trial, error, and 30 years real estate investing experience, Ive figured out a way to get the best of both worlds in one of the most expensive real estate markets in the United States: Washington D.C. How? BRRRRwith a Section 8 twist! Being the nations capital, Washington D.C. has weathered economic downturns quite well, especially when compared with other major cities. Federal Reserve and other economic data clearly support this. With that said, similar to other major cities, Washington D.C. is struggling with affordable housing, gentrification, and other challenges. The bottom line is theres a housing crisis that appears to have no end in sight. This situation in turn has created opportunities for astute real estate investors. How to Generate Cash Flow While Forcing Appreciation So how am I actually acquiring these properties, getting them rent ready, and finding quality tenants who will pay high rents and stay for a long time (i.e., 5, 10, 15, or 20 years)? Heres my secret: I look for rundown, ugly houses in desirable, up-and-coming neighborhoods, where the local housing authority pays rents at market rates. First, I know what types of properties I want, and I know what I dont want. In short, my buying criteria are focused and very targeted. Buying anything just because its a good deal is a major mistakeone that will derail the strategy Im attempting to convey. Where do I find these houses? I get them from a variety of sources: word-of-mouth, wholesalers, Realtors, or partners in my joint venture program. Given the highly competitive D.C. market, I buy these houses with cash ($400K to $500K) using a combination of private lenders, bank lines of credit, and my personal funds. Same goes for how I fund my rehabs, which range from $75K to $150K. Related: How I Find Private Money Lenders to 100% Fund My Deals (& How You Can, Too) How to Land Deals in Competitive Markets I know. You can pick your jaw up off the floor. I get that these numbers are eye-popping if you live in a less expensive market. But in markets like D.C.or San Francisco, Seattle, Boston, L.A., etc.this is what it takes to buy and get these deals done. A critical part of my strategy is to add value, force appreciation, and create equity by: Only buying in neighborhoods where after repair rents are high.Only buying houses where I have the potential to add at least one (but preferably two) bedrooms as part of the rehab. (For example, I often turn three-bedroom houses into five-bedroom homes.) By focusing my rehabs on amenities that add value and force appreciation, I have built-in equity after rehabs are completea critical part of my BRRRR strategy. This ensures my refinance appraisals come in as expected, or sometimes slightly higher. Coupled with the high market rents, when I refinance, Im able to recoup most of my expenses and dont have to leave much of my own cash in the deal. But how can I cash flow? By understanding how much rent local housing authorities pay (rents are publicly advertised), the guesswork is eliminated from the equation. In short, I know up front what rent will be approved and whether this amount will allow me to meet my cash flow targets. By working backward, I know how much I can pay for a house, how much I should spend on the rehab, and more importantly, how much cash flow I can realize after all is said and done and all expenses are paid. I encourage you to learn more about this powerful, profitable, and often-overlooked niche. Before and After BRRRR Photos Before I go, Ill leave you with these photos from one of my recent deals: Exterior   Living Room   Kitchen   Bedroom   Bathroom   What do you think of my strategy? Comments? Questions? Lets talk in the comment section below! https://www.biggerpockets.com/blog/big-city-brrrr-cash-flow-appreciation We have all heard that two-thirds of business startups fail in the first decade. If youre like me, you encountered this statistic but dismissed it, telling yourself, That wont be me!

Now, a couple of months or years later, you may be wondering why things havent taken off like you thought they would. This issue could be plaguing your real estate business, social media platforms, a startup business maybe even your personal brand. Why Youre Struggling to Become Successful Here are the six reasons I find most people struggle to find successand how to fix them! 1. Youre not setting goals Would you depart friendly lines with a convoy without knowing your checkpoints? No. Would you step off on a hike without knowing your mission? No. So why would you walk through life without goals? The short answer is you shouldnt. The Marine Corps teaches the importance of setting S.M.A.R.T. goals. The acronym refers to: Specific: Rather than saying get in shape, define what you specifically want to achieve, such as losing weight, toning up, etc.Measurable: Rather than saying lose weight, say lose 10 pounds in two months. This is a quantifiable goal and can be tracked.Attainable: Ensure your goal can be accomplished.Realistic: Be honest with yourself, and keep in mind any obstacles you may need to overcome.Time-bound: Set a deadline. Deadlines are key to accomplishing your goals, but you must adhere to them!  2. You dont practice accountability Nobody is perfect. We all know this to be true. For that reason, it is extremely helpful to have someone holding you accountable to your goals. Going back to our fitness example above, even the most motivated person will eventually have a day where they dont want to work out. A good workout partner will hold you accountable and not let you skip. This works the same with any goal. Accountability can take many formsit could be a weekly mastermind meeting, your spouse, a friend who you ask to hold you accountable, etc. The important piece is to have checks and balances in your life that ensure when your moment of weakness comes, you can resist it! 3. Youre making excuses Nobody cares about your success more than you do. So stop making excuses, and start doing. Stop worrying about problems, and start finding solutions. It is imperative that you do something every day in order to move the needle forward. Making excuses will accomplish nothing; its simply wasting your time (and anyone unfortunate enough to be listening). This is why I have friends like Alex Felice, who are so quick to tell me when Im starting to make excuses. We are all human, and it is natural to make excusessometimes without realizing it. Much like accountability, a friend who can see through your B.S. is invaluable! There is a popular phrase in the military, Excuses are like a**holes, everybody has one, and they all stink! While crude, this is the way you need to think of excuses. They dont move the needle forward, they dont make you feel better (in the long run), and they have no place in your life! Related:6 Ridiculous Excuses That Are Holding You Back From Real Estate Success  4. Your network sucks It is said that your wealth is the average of the five people you spend the most time with. If youre the smartest person in your network, you need to find a new network. These statements might sound clich, and Im sure you have heard them before. But there is a reason they are repeated often: they are true! You dont need to cut all of your friends out of your life, but there is nothing wrong with ditching the negative Nancys for some positive Pauls (pretty sure I just made that up). Seriously, if the people around you arent helping you grow as a person and accomplish your goals, you need to improve your network. A good way to do this is to attend real estate investor meetups and get busy meeting people with similar goals! Every time I attend a real estate investor meetup, I am amazed by the growth I experience. Improving your network is (in my opinion) the most important thing you can do to become successful! 5. You arent learning You need to learn something new every day. Formal education is great and all, but that isnt what I mean. You need to learn something every day that will help you achieve your definition of success. For real estate investors, this could mean reading a book on real estate, listening to a podcast, or having lunch with a mentor. Search Google for useful blog posts or YouTube videos during your free time!  The point is that you need to set aside time every day for personal development. I believe that the best investment you can make is in yourself! Dont overlook opportunities for growth. Daily growth compounded over time will make you into a very successful person. Conferences and seminars offer a bonus perk: they are an excellent way to combine personal development and networking! I love attending these events to grow personally and build my network, while simultaneously getting a motivational boost! Related:The 4 Levels of Learning in Real Estate Investment 6. Youre not taking extreme ownership Everything is your fault! Much like making excuses, failure to take responsibility for your situation is a waste of time and not conducive to improvement. In his book Extreme Ownership: How U.S. Navy SEALS Lead and Win, Jocko Willink uses the example of being five minutes late to work. Is being late to work because of traffic your fault? Yes. Because if you had left the house 10 minutes earlier, you would not have been late. Will Smith has a great motivational video about the difference between fault and responsibility. In his short clip (which I recommend that you watch by searching Fault vs. Responsibility on YouTube), he states that whether or not something is your fault, it is still your responsibility. An example is that its not your fault if your significant other cheats on you, but it is your responsibility to decide how youre going to react. It is also not your fault if somebody passes away, but it is your responsibility to cope with it. The main theme with both of these resources is that we need to act less on a woe is me because X, Y, or Z happened mentality, and instead think in terms of this happened, so how do I fix it? or this happened, so how can I ensure it doesnt happen again? It isnt easy to take extreme ownership when things go wrong, but it is much more productive. This mindset shift will open a lot of doors to you as a leader, and the better I get at this, the more successful I become as a leader of Marines. Conclusion Now that you are aware of these six reasons youre not succeeding, it is time to utilize extreme ownership and change! Knowing your deficiencies will always give you an edge over the competition. But that edge is useless if you dont constantly improve. That is why you need to constantly work on all six of these issues, and look for ways to grow.  What are you currently working on for personal development? Share in a comment below! https://www.biggerpockets.com/blog/success-struggles-reasons-fixes The number of dwellings approved in the country slid by 0.6% in March, in trend terms, according to data released by the Australian Bureau of Statistics (ABS) today.

Among the states and territories, total dwelling approvals fell in Victoria (3.5%) and Queensland (1.4%) in trend terms. On the other hand, the Australian Capital Territory (4.8%), the Northern Territory (3.9%), Western Australia (3.8%), New South Wales (0.8%) and South Australia (0.4%) recorded increases. Tasmania was flat. The overall decrease was driven by private-sector houses, said Justin Lokhorst, director of construction statistics at the ABS. Approvals for private-sector houses fell 1.4% nationally in trend terms. Declines were posted by the three largest states: New South Wales (3.4%), Victoria (1.8%) and Queensland (0.9%). Tracking the opposite direction, Western Australia (1%) and South Australia (0.9%) rose over the month, ABS also found that approvals for private dwellings excluding houses climbed by 0.8%. In seasonally adjusted terms, total dwellings declined by 15.5% in March, largely driven by drops in New South Wales (27.4%) and Victoria (27%). The decline was led by private dwellings excluding houses, which fell by 30.6%, while private house approvals fell by 3.2%. The value of total building approved was flat in March, in trend terms. The value of residential building rose by 0.4%, while non-residential building slid by 0.6%. The annualised rate of dwelling approvals has been above 200,000 for almost five years. The latest data pulls us below this watermark. The downwards trend is set to continue over the remainder of 2019, with negative leads still coming through from property prices, turnover rates, housing finance, and land sales, said Tim Hibbert, principal economist, building and construction for BIS Oxford Economics. Do you have more than $200k in your super fund? You could use your super to buy property - Find out how https://www.yourinvestmentpropertymag.com.au/news/new-dwelling-approvals-tumble-262571.aspx |

Archives

December 2020

Categories |

RSS Feed

RSS Feed