|

Driver-less cars are going to change alot, and if you havent been actively reading about this, then its most likely going to happen much faster than youre expecting. At first glance, there may not seem to be much overlap between the auto industry and the real estate industry, but the impacts and infrastructure changes from this technology will be felt by everyone. As investors, its our responsibility to understand changes as far out in advance as possible so we can adapt to progress and mitigate new risks.

Just about everything in this article takes place across the next 1530+ years, which may seem useless to some. However, if youre currently buying 30-year mortgages then youve got commitments that fall well within this transition period, and these changes will affect you. Having a better understanding of the future can be massive risk-mitigation tool against getting caught off guard when changes negatively affect you. Driving Will Change Where People Want to Live Because Cars Will Commute for Us Imagine you could wake up at 6 a.m. and crawl into your car and tell it to head to work while you got back to sleep. In two hours, youre there, youre safe, fully rested, and you arrive at work on time without having to deal with traffic or the monotonous task of driving. This is not science fiction. In fact, based on todays technology, this isnt even far fetched. This is science inevitability. So how does this affect real estate? Well, think of all the people who dont want to live in Washington D.C., Los Angeles, or New York City. What if they could live an hour or two outside the city and commute to work without losing any real time out of their day? How might this affect home values in a city when people can commute there easily without having to live there and without making any sacrifice to do so? It doesnt even have to be this extreme, either. Lots of people would be willing to commute for one hour each way if they didnt have to drive. This creates a lot of space between a city hub and the places people can live without taking on the financial burden of city costs. Might home values in a city go down when the necessity to live close by is reduced? Maybe cities will create an even larger price premium for those who can afford to live there while the masses are forced to commute an hour or two each day from poorer suburbs. Cars Will Be the Next Rental Real EstateOwning a Car Will Be a Luxury Car ownership is going to be a thing of the past before you know it. Sound crazy? Its not even a secret in the auto industry. Did you know that Ford, the oldest car company in America, has announced its going to stop selling cars and just sell trucks and SUVs? How can they do this? Thats a lot of cars to give up on selling unless they dont expect to lose that many sales. Companies who host ride sharing like Uber, Waymo, and Lyft are developing fully autonomous vehicles and are building fleets to replace personal car as we speak. General Motors is building a mass-market, fully autonomous car right now that will not be sold to the public. It will be only be used as part of a ride-sharing platform and available (supposedly) in 2019. That means two of the biggest auto manufacturers are starting to just flat-out not sell their products to the public. This is a signal of really big change. Owning a car isnt really that expensive, but there is zero return on investment. Its only an expense. However, once cars can finally drive themselves 24-hours a day, all while producing income, the value of ownership will go through the roof. The most likely scenario is that Uber will sell unlimited-use passes by the month, and we will all happily give up car ownership in trade. Itll be on-demand, easy, fast, and awesome. It may sound far fetched, but people will happily give up car ownership in the not-so-distant future when the cost savings become obvious. The value of any business is based on its income production. If you think cars are expensive now, imagine how much more they might cost when its a guaranteed profitable purchase. Related:Your Car is an Expensive, Health-Sucking, Time-Wasting Machine. So, Ditch It! Those with means to own their personal cars will create a moat between social classes. These days we might see a Ferrari and say, Oooooh, that person has money! Look at their fancy car! In the future, someone driving a Camry might get similar treatment: Ooooooh, that person has money, they can afford to have a personal car!!! Lots of people in America buy their own homes, and some own an extra house as a rental. The volume of landlords is relatively small because owning a house requires capital, resources, knowledge, risk mitigation, etc. In the future, cars will be the new rental real estate; people with means will still own their cars, and a few will own an extra car. The second car will drive itself around as part of a ride-sharing platform and produce income, just like a taxi, but passive.  Remember That Extra 900 Square Feet Everyone Had to Add to Our Houses to House a Car? What Were They Called? Oh Right, Garages! Why would you need a garage if you dont own a car? What value does a garage provide? Storage, for sure: We get to put our unsightly water heater there, the Christmas decorations, and the treadmill that my wife just had to own. Is that all worth the space and cost that a garage requires? Not likely. So will garages be a premium in the future, or a nuisance? More likely itll fade from importance in middle-to-low-end housing and continue in luxury homes. This problem is already being tackled with large parking garages. It might be a bold claim to say you wont need your garage in 20 years, but the world really wont need massive multi-level parking garages. Efforts are already being made to find out how to convert these spaces into light retail, office, storage and other amenities. Its not going to be feasible to tear down all that concrete, but it will be imperative to find something useful to do with all that space. Currently we pay a premium for garages because they are a highly sought after convenience. However, when the majority of people dont own cars, will that garage command a premium? Or will it be a detriment? Whats the Land Underneath a Gas Station Worth? Some of the most valuable land you can find is sitting underneath a gas station, and for good reason. Corner lots with good road access on busy cross streets serve a lot of cars and provide tons of ancillary needs. (Where else are we supposed to buy Slim Jims?). This infrastructure has been built up over decades and billions of drivers, but at its core it really relies on one thing: the internal combustion engine. Electric cars, however, dont need gasoline (surprise!). Youll charge at your home and probably at work. So how often are we going to need a gas station then? Hard to say, but the fact is, people will use a lot less gasoline, and my assumption is they will use gas stations much less. Now, obviously, some operators will find competitive advantages to survive, but many will not. And in rural areas, we should expect this problem to be much worse. A complete halt on gasoline sales is unlikely, because there are still uses for the product: small engines, generators, non-EV-conformers, etc. Thats a pretty weak position to hold onto though. Lots of industries are long gone, but still have niche support. Walmart will still sell you a CD Walkman (I saw one recently for $30!), but you wouldnt use that example to highlight the value of compact discs. Related:7 Sharing Economy Side Hustles Real Estate Investors Can Use to Earn Extra Cash When gasoline sales do slow, what will gas station owners do? I personally think most will go away, but not before suffering increasingly diminished profits as they experience the decline. Many will sell their businesses because of this, and what will their assets be worth? No one wants to look at a declining income statement trend and then pay top dollar. What about all the stores attached or adjacent to gas stations that capitalize on the heavy traffic? Ive heard of no great solutions to these questions, but that wont stop the impending takeover of autonomous and electric cars. How Long Will All My Daydreaming Take to Come to Fruition? If you dont read often about this topic, then its likely that this transition will happen much sooner than you would guess. People hear about autonomous cars and say, Itll never happen. Well, never will begin in 2020 when both General Motors, Ford, and others start to produce mass-market autonomous cars. What happens when every cab and Uber driver across the country goes jobless in a few short years? Ride sharing platforms will replace car ownership, as I mentioned earlier, and it will start next year. GM has publicly announced plans to build cars not sold to the public. They will only be part of their ride sharing platform.next year.How will home values be affected when waves of mass unemployment start? Take everything Ive mentioned so far and apply it to truck drivers as well. In fact, they will be unemployed first, as autonomous 18-wheelers are already being used in the UK. Unfortunately, I have no good advice for how to adapt to this, but anticipation and being proactive about change should help. For the Itll never happen camp, they will not take any measures to protect themselves and it will cost them dearly. What I dont want to convey here is not to buy a house with a garage because you might not need one in 30 years. Thats silly, but maybe get used to the idea of not needing one in the future. Sleeping in our cars is what poor college kids do when they are really stretching, but in 10 years it might be a feasible temporary option instead of stretching to rent an apartment. Twenty years ago smartphones didnt exist, now I cant go three minutes without touching mine. Its important not to get too confident of what is normal, as you may get caught stuck in the past. You dont need to have an MBA to know that businesses who refuse to participate in new technology go under. The board members at Blockbuster obviously had a strict head-in-the-sand policy. Dont be like Blockbuster. Embrace and adapt to changing technology.  What do you think? Am I on to something? Where do you see the future of garages and personal vehicles? Share below! https://www.biggerpockets.com/renewsblog/stop-building-garages/

0 Comments

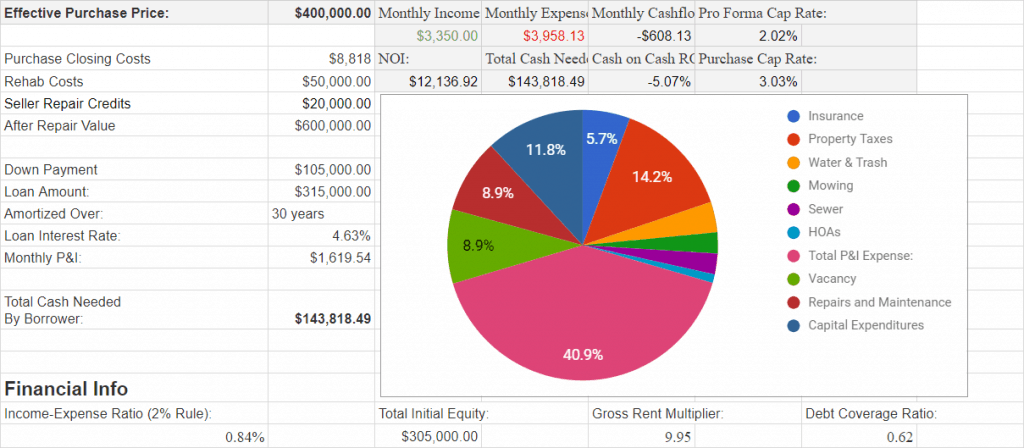

Is this crazy?I sat there with my 23-year-old head spinning looking at the first $400,000 multifamily rehab project that I had just put under contract.

Youve probably asked yourself (at least) a couple times if its crazy to get into real estate, too. If you asked your friends and family instead, they probably immediately answered Yes! followed by a spiel about whatever aspect of managing a real estate business that scares them most: the risk of a market crash, the challenge of dealing with tenants, or the pitfalls of negotiating with contractors. Its only human. We fear risk. We fear risk even when our fears are irrational. Even if you drink the real estate Kool-Aid and know that real estate can be an amazing way to build wealth, the fear probably hits you each time youre about to write an offer on a building. Do I really know what Im getting myself into? Right Before the PlungeOn that night in May 2017, I was on the verge of taking what to many people would look like the biggest risk of my young life. I was 23 years old, had recently graduated from college, and had barely six months of real estate experience. This project would pit me and my business partner against countless situations we were not prepared for, faced with countless questions we didnt know the answers to.  Drilling through foot-deep concrete subfloors was definitely not something college prepared us for. Drilling through foot-deep concrete subfloors was definitely not something college prepared us for.Luckily, as real estate investors, its not our job to know the answers. Its our job to know the numbers. The numbers on our first rehab deal told us that even in our worst-case scenario even if everything that people warned us about went wrong taking the plunge would get us closer to financial freedom than sitting safely on the sidelines ever could. Why are we comfortable losing money, as long as we know how much were going to lose? As a recent grad, most of my college friends ended up in big cities on the coasts. Related:Mastering Turnkey Real Estate: How to Build a Passive Portfolio In 2017, the median rent in Manhattan was $3,150 a month. According to Rent Jungle, the average rent for a one-bedroom apartment in San Francisco was even higher: $3,334 a month. Over the course of a year, that adds up to $40,000 in rent for a one bedroom apartment. For reference, the median family income in the city of Saint Louis is $52,000 a year. In Saint Louis, that money can buy buildings. On the coasts, it buys you the right to spend to 39 percent more than the national average on basic necessities like groceries. The costs are pretty crazy, but the craziest part is that spending a familys annual salary on rent is somehow considered a perfectly normal financial decision for a young person to make. Young people spend that money with no expectation of getting a return. Rent, groceries, and transportation are costs no investments. What is the risk of embarking on a rehab project, compared to the 100 percent certainty of spending $40,000 a year on rent? How We Measure RiskRisk is exposure to uncertainty. Because of this, renting doesnt feel like a risk. Neither does spending a lot to live in a big coastal city. The costs are large, but theyre constant. We know them up front: $40,000, paid in tidy, predictable monthly increments. Or do we? What is the real risk of renting away your twenties and how do you compare it to the risk of a rehab project? Does renting in a big city make your financial future not in 10 months, but in 10 years more certain, or less so? When youre embarking on a rehab project, uncertainty stares you in the face. The risks are all right ahead of you, a landmine of knowns unknowns: Do we have our contractors lined up in the right order? Have we done everything we need to pass inspection? Will we hit our rent targets once all the work is done? Is it cheaper to fix this or replace it? Those seem like hard questions to answer. Small wonder that most people warn you away from real estate. Except when youre following a safe, normal path, uncertainty isnt gone, its just waiting for you out of sight. Five years from now, will I be working at a job I dont like? Or will I be free and doing the things that matter to me most in life? Ten years from now, will I have the resources to protect what I love? To support my family, friends, and community? Those are hard questions to answer. For me, those questions would have been impossible to answer if I lived in a big city on the coast, took a fancy job where I was well-paid but spent most of my salary on rent and groceries, and had to spend most of my time working for someone else. We are conditioned to deal with long-term uncertainty the same way were taught to deal with short-term risk: by avoiding it. But avoiding risks doesnt make them go away. It doesnt teach us anything. It doesnt get us any closer to answering lifes hardest questions. The numbers on our first rehab deal told me two things. In the worst-case scenario, I would come out of the deal not losing any more money than someone who chose to rent in a big city. In the worst-case scenario, I would come out of the deal with an education that would allow me to take control of my financial future. I could live with that. The Numbers Tell The StoryMy business partner, Ben Mizes, and I started our real estate portfolio with an FHA loan. We were only required to put a small down payment on a relatively stress-free, low-maintenance four-plex. Five months later, we were planning to borrow $315,000 from the bank and $105,000 from private family investors, and spend as much of our own time, sweat, and money as it took to come out the other side of our first four-unit rehab. The project would be our first BRRRR, or buy, rehab, rent, refinance, repeat. We were upgrading kitchens, bathrooms, and AC units to bring the rents up from $825 per door to $1400 per door a 70 percent increase. With renovations complete, Ben and I would try to appraise the building for $700,000. Depending on the lender, you can borrow between 70 85 percent of a buildings appraised value. In this range, as long as we hit our numbers, we could completely repay our investors, recoup our costs, and walk away owning a cash-flowing castle.  Out first four-family renovation in Saint Louis. Out first four-family renovation in Saint Louis.The potential upside was clear. Just as important, we looked at our downside. Ben and I modeled a worst-case, do-nothing scenario, trying to understand what would happen to us if we got stuck and couldnt complete the rehab at all. What Could Go Wrong?Well, Plenty. Ben and I had a contract to buy the building for $420,000. At the closing table, the seller would credit us for the $20,000 worth of repairs that had to be done immediately: fixing a collapsed sewer, repainting and sealing damaged windows, and replacing falling fascia boards. Note: we always, always, ALWAYS make our buildings watertight before doing anything else. If they arent watertight when we buy them, we negotiate for repair credits to fix problems on the sellers dime immediately upon closing. The $20,000 repair credit provided by the seller brought our effective purchase price to $400,000. Combined, our mortgage payments, taxes, and insurance came out to $2,277 per month. The numbers told us we could make our mortgage payments comfortably, even in its current (read: very rough) condition, the building was generating income of $3,350 per month, or about $825 per door. Assuming we got completely stuck and had to keep renting the units out for their present value of $825, we would have $1,073 per month with which to pay all of our fixed and variable expenses. Utilities and HOA fees (the building is in a private subdivision with an annual assessment) came out to $380 per month, leaving $693 a month to deal with variable expenses. In a worst-case scenario, we would be self-managing to save on property management fees. That would still leave us with vacancy, repairs, and maintenance costs, and the need to set aside money each month for a capital expense escrow. Was $693 really enough?  Under our most-conservative model, we planned to put aside $10,000 each year for repairs and escrow. After five years, that equals $50,000 put into proactive maintenance enough to deal with a roof, a complete tuck-pointing redo, and major structural repairs. Then we figured 10 percent vacancy cost high for the area, but not impossible if we had hard luck. What was the worst that could happen?  Under our worst-case model, we would be losing $600 every month. Losing $600 a month is a losing deal. Thats not a deal that gets you on a podcast. Its not a deal that successful investors show off in a blog post. Luckily, its not what the deal we ended up with, either. (Spoiler Alert: we came out of this rehab with a lot more paint on our shoes, but a lot more cash in the bank, too.) But when we talk about risk, heres the curveball question: Would this worst-case deal be a step away from, or a step toward, financial freedom? Lets look at those numbers again. The Difference Between Costs and InvestmentsAn investment is any place where you can put your money, such that it creates more wealth over time. In the model above, a lot of the expenses that look like costs that is, look like places where Ben and I would have lost money are actually investments, places where our money helps us build wealth. Related:Why Turnkey Rentals Might Just Be an Ideal Investment for Real Estate Newbies 1. Loan Pay-DownIn our worst-case scenario, we would pay $600 a month (on average) to cover the costs of repairs and build a sizeable rainy-day fund. However, our $1,600-per-month mortgage would be completely paid for by our tenants. In the first year alone, our tenants would pay for our ~$14,000 interest payments, and help us build $5,000 worth of equity in the building.  Break even on rent: you pay thousands. Break even on mortgage payments: you make $300,000. Break even on rent: you pay thousands. Break even on mortgage payments: you make $300,000.Over time, that equity build-up only accelerates. In our thirties, Ben and I will build up $85,000 through principal pay-down alone (pun intended). The amazing part is that would be the case even if the rehab project was a complete failure. Breaking even on mortgage and utilities and scraping out of pocket to cover unexpected repairs, Ben and I would still be positioning ourselves to accumulate passive wealth in the future. 2. Proactive MaintenanceIf you spend $50,000 on a building in five years, it becomes a lot cheaper to maintain. Under our worst-case model, we would have $10,000 a year to deal with maintenance issues before they became more serious. When you budget to deal with problems up front, it makes for a less-impressive pro forma but it also means that maintenance costs get significantly lower over time. If you plow $10,000 every year into it, even a problem-ridden property will get easier and easier to take care of. It might be a painful cost to swallow in the short-term, but you havent lost the money that you spend on a property you own. Youve just re-invested it. By contrast, if you spend $40,000 in one year on rent, the money is out of your hands for good. 3. Hands-On EducationWhen you buy your first rehab, the most important investment you make isnt in the building. Its in yourself. Youre taking out (quite possibly) the only student loan in the world that can pay itself off in less than a year.  Our first kitchen didnt turn out like this. But our second, third, and fourth did. Our first kitchen didnt turn out like this. But our second, third, and fourth did.The most daunting part of diving into a real estate deal the part that makes people say its too risky is that you dont just stand to lose money, but time, too. The time costs on this project would have made this a losing deal for a veteran investor. We spent untold hours painting, fixing plumbing, and (like you saw above) drilling holes through concrete when a contractor dropped the ball on us. But we werent veteran investors (yet!). As Ben and I looked at the numbers together, we realized we were buying ourselves both a building, and an education, too. Even if we broke even, we would come out of the project with an education that in itself was worth hundreds of thousands of dollars. So What Happened?One year ago, I sat looking at the numbers on a $400,000 real estate deal that could either set me on the fast-track for financial freedom or go completely off the rails. In the end, both things happened. My business partner and I got screwed over by not one, but four different contractors before we finished the project. One caused thousands of dollars of water damage to the floors, embroiled us in a months-long insurance claim, and tried to take us to court after he lost. We dealt with an irascible tenant who threatened us and damaged his apartment. Time and again, things took more time, sweat, and money than we had expected. But the age-old mantra of real estate investing held true: you make money when you buy. The numbers of the deal were strong. And now that were done dealing with contractors, tenants, and renovations (at this property), we have a building that rents for $1,400 a door, water-tight with low maintenance costs, and a fair market valuation between $650,000 and $700,000.  The final numbers on the deal The final numbers on the dealNow we are on pace to refinance the building, fully repay our investors in the first year, and walk away with the funds to do it all over again. Taking the Plunge (Again)Is this crazy? Im sitting here with my 24-year-old head spinning, looking at the numbers of a 20-unit deal in Saint Louis. Since starting our renovation project one year ago, weve used the education and cashflow we gained from it to build a 22-unit portfolio and a high-growth startup. Now, with a refinance underway, I am looking at a deal that could double the size of our portfolio overnight, all while working full time. A new project brings new unknowns. More questions we dont know how to answer, and lots more numbers to keep me and Ben busy. Would you have taken this risk? What has your experience taught you? Share below! https://www.biggerpockets.com/renewsblog/for-the-cost-of-a-1-bedroom-apartment-in-new-york-i-built-a-1-3m-real-estate-portfolio-in-st-louis/ Raising rent can be an importantpart of staying profitable as a real estate investor. Still, it comes with risks, such as tenant turnover and increased time commitment. While there is no one-size-fits-allanswer to the should I raise my rent question, you can best inform your actions by assessing your investing priorities, evaluating your relationships with your tenants, studying your local market, and more.

An expert is someone who has succeeded in making decisions and judgements simpler through knowing what to pay attention to and what to ignore. Edward de Bono Your tenants leases are about to expire. Theres a for rent sign on the house down the street, and the owner is trying to rent it for an amount that exceeds your rent. You would also like to raise rent, but the local economy is showing signs of weakness, and your current tenants are great. What should you do? Raise rent and risk losing the tenants? Or maintain rents the way they are and risk missing out on income growth? So, you scoured investment property forums, searched on Google for should I raise my rents, and reached out to your local palm reader for her opinion. You are still unsure what to do, and now youre down $50 bucks for those tarot cards. On the forums, one passionate group says, Raise the rents! and the other group says, No leave them where they are! And you walk away even more confused and puzzled. The clock is ticking, the lease is about to expire. What should you do? How This Guide Will Help You Save Money Reader: Wait a second! Im here to learn how to make money, not save money. Can you provide me with answer to my rent dilemma? Sadly, there isnt a one-size-fits-all policy for deciding to raise rents or not. It all depends on the persons unique situation. Instead of providing a definitive answer, its better if we empower ourselves to make our own decision. This article will discuss the numerous factors involved in raising rents. Usually people narrowly focus on the market rate for rents to determine whether one should raise themor not, but that shouldnt be your prime focus. There are numerous other components at play that should determine our final action. Whenever we arrive at a crossroads in life, be it investing or personal, its always good to stop and reflect on what were trying to accomplish overall. Our values, usually written in a form of a business or hobby plan, will help us to determine the best course of action during uncertain times. This guide will not provide you with a one-size-fits-all answer to your problem. Think of this guide as a decision making process to calculate the risk involved in making rent related decisions, so you dont lose a quality tenant due to a knee-jerk emotional decision. The Goal of Raising Rent: Its Not What You Think Narrowly framing the situation as an either-or dilemma, to raise rents or not, distorts the reality of the situation, which fans the flames of emotion and leads to a potentially bad decision. Making good decisions requires an understanding of all the alternatives so you can properly value the costs and risks involved in the final decision. So lets reframe the question: What are my priorities for this property? Reframing the question creates alternative scenarios, which lead to better decisions because we can weigh the tradeoffs involved. Potential PrioritiesMaximizing profitsMinimizing personal involvementMaintaining a low vacancy rateDecreasing tenant turnover costsStabilizing cash flow Thislist is a starting point to determine your motivations behind aninvestment. Start brainstorming and think to yourself what are your true priorities. Frank: Well, maximizing profits is important to me, but I dont know if its worth risking a higher vacancy rate and spending my weekend showing the property to new tenants. Sue: Come to think of it, I really care about tenant stability and minimizing my time commitment. I have a demanding career, so I dont think raising the rents is the best decision at this juncture. Pete: Actually, maximizing profits is something I would like to proceed with because I can handle the potential risk of tenant turnover and the added time involvement.  Related:How to Successfully Raise Rents Without Risking Costly Vacancies The Power of Anchoring When the tenant signed the original lease agreement, your negotiations for rent didnt end there. It just symbolized the closing of one chapter and the beginning of another in the ongoing negotiation for rent. The original rental price has a powerful anchoring effect on subsequent negotiations. While we might think everyone is perfectly objective, we are emotionally-driven animals. We have strong sense of fairness running through our minds, and if the tenant perceives the rent increase to be unreasonable, they will be compelled to walk. No matter how underpriced the rents are, they will use their original rent as a reference point. Your Relationship With Your Tenant Another factor to consider is your current relationship with your tenant. Having a great tenant is compelling reason to leave rents at current levels or to minimize rent increases. If the tenant is excellent, is it worth the trouble to raise the rent at the risk of losing the tenant? Finding a good tenant can be a tough proposition in any market. Signs of a Great TenantDoes the tenant pay always pay her rent on time?Does the tenant maintain the interior and exterior of the property?Have other tenants complained about this tenant (Noise complaints or property upkeep)?Does the tenant update you on potential issues related to the property? Some investors minimize rent increases in a hot market, and if the tenant leaves, they list the property at a higher market rent so the new tenant doesnt feel heartburn of having massive rent increases after signing the lease. Rent Increase Percentages and Tenant Reactions In the SF Bay Area, rents are anything but affordable, while in other markets rents are affordable. In some markets, tenants expect regular rent increases of 10%+ as status quo, while other markets tenants would consider moving immediately. In general, Ive found that rent increase reactions cluster around three price bands. Rent Increase Reactions (Rule of Thumb)1-5%: Expected increase, its not worth moving unless my rents are severely above market rents.5-10%: I might consider moving, but if the property is well maintained, located in a nice area and has great amenities, I will probably stay put.10%+: Time to consider moving, unless I live in an area where all rents are increasing by 10% and moving would add significant time to my commute. Now, everyone looks at increases differently, but once you start finding yourself in the 7-8% plus range, tenants start to think, Will these increases continue indefinitely? and Maybe its time to start looking for a new place to live. As a landlord, you must be aware of the hidden message youre sending tenants by increasing their rents.  The Hidden Costs of Raising Rent A bird in the hand is worth two in the bush. Proverbs of Ahiqar Before deciding to decrease or increase rents, you should determine the cost benefit analysis of your decisions. Investor Pete has decided his propertys monthly rent should be increased from $600 to $650 (8.3% increase), which would be a gain of $600 per year. Pete asked his property manager to research market rents in the area. The market rate for rents in his area is $500, but Pete is confident that his property is worth the rent premium because of the curb appeal of the unit and amenities. Petes city is going through an economic downturn, and local vacancies have been on the rise. The property down the street has had a for rent sign on it for one month, and the asking rent is $550. One thing Pete should think about is the risk of losing a tenant due to the rent increase and the costs involved in re-renting the unit. Potential CostsOne-Month Vacancy: $650Turnaround Costs: $500Advertising: $50Finders Fee for New Tenant (One Months Rent): $650Total Cost: $1,850 (Pay Back Period: three years and one month)Pete is risking a potential loss of $1,850 for a yearly gain of $600. If Pete is wrong, it will take him at least three years and one month to recoup the costs involved for finding a new tenant. Also, if the lease expires during the winter or when school is in session the vacancy could be longer than one month. Maybe its not a good idea for Pete to increase rents at this juncture. Maybe he should wait until the market strengthens. Related:Is Now a Good Time to Raise Rents? Tenants Previous Earnings An indicator of whether the tenant will be able to afford the rent increase will be the tenants earnings history. Open your tenant file and see what the tenant was earning when they qualified for the property. Now this isnt scientific, but you can make a rough approximation of what their current salary should be a year hence of completing the application. You could either leave the salary as is or you can factor in an inflation adjustment. I use the rent coverage ratio to measure the tenants gross monthly income available to pay the current rent. For my tenants, I require gross monthly income to be at least three times the monthly rent. If your rent increase causes the rent coverage ratio to fall below three, the tenant might leave or fail to pay their rent. Assess the Local Economy No matter how impressive the property, its still subject to market forces. Understanding the local economy will let you know what the market rates are for rents in your area. Questions to determine the health of your local economy include: Whats the unemployment rate for your area?Whats the average vacancy rate in your area? How long are listed properties remaining vacant? You can find this information via multiple sources: Bureau of Labor Statistics, a quick Google search, your local real estate association, business journals, or local property managers. Find Comparable Rentals in Your Area Before you make a decision on rents, you must analyze the current market to determine the market rents for your area. The market rent is what people in your area are paying for rental housing. By determining market rents in the area, you can determine if your increase is within reason. Rental prices for your area arent determined by your gut feeling or by your desired returnthey are determined by market forces. No matter how minor we perceive the rent increase to be, the tenants opinion of the increase will be determined by its proximity to market rents. There are many ways to determine market rents. Here are a few suggestions: Walk around your neighborhood. This is the best way to determine the market rents for your area. Look at rentals in your area and try to arrange a preview of those properties.Speak to the locals. Ask them about how much a certain property was renting for in the area and whether they would be willing to rent the property.Speak to property managers. Ask them about the going rate for rents in your area.Speak to other investors. Youll learn about market rents, expand your network, and you never know if the investor might want to sell their property to you.Using Online Sources to Determine Market Rents Out-of-state investors dont have the luxury to drive through their propertys neighborhood, so they will need to call local experts and review online sources to determine market rents. While online resources are easily accessible, they list rental prices that are aspirational, not the final leasing price (which can be lower than the listing price). Unfortunately most online sources dont have the capabilities to determine the final agreed upon rental price. Sites to find rental comparables include: You can use Rentjungle.com and Zilpy.com to determine rent trends in your area; however, none of these sites should be used as the single point of truth because each site has its own biases. Comparables vs. Your Property Sample size is everything. Try to find as many properties as possible within your propertys neighborhood, and make sure to create a database to track these properties. It doesnt matter if your property is a duplex and the property for rent down the street is an apartmenttenants tend to lump different residential property types into the same category. Now its time to combine the data that you have collected to analyze how your property fairs against the competition. You can add the information into a basic spreadsheet, such as this one, to get a better idea of how the market is determining value. While understanding the market rents for the area is important, these averages exclude the unique features that your property may offer. Make sure to add or subtract the value of the amenities included in the rental. Its hard to precisely determine the true value of amenities, but you can approximate the value by finding comparables. If you see two properties in the same area that have approximately the same square footage, but one unit has one bedroom and the other has two bedrooms, you can approximate the value of an extra bedroom by the difference in prices between both rentals. It isnt a scientific calculation, more of a ballpark measurement. Things to Compensate for When Determining Market RentDoes the property have curb appeal? Are people living there because they want to or because they have to?How many bedrooms and bathrooms?Size of the backyard?Whats the propertys walk score?What utilities are paid for by the tenant?Does the property include garage parking?Does the property allow pets?Is the property furnished? By aggregating the data and refining it based upon your understanding of the market, you will be able to determine the market rent for your property. If youve concluded that your rents are currently above market and that an additional increase wouldnt be worth the hassle, then you may even consider decreasing the rents depending on the state of the local economy. Sometimes it is better to get ahead of a softening economy, and lower your rents to prevent a vacancy. Important: A Message from Lawyer Cat Remember, each state, city, and county has its own rules and regulations regarding rent increases and communicating rental price changes. Please read the rules or consult a human lawyer. According to the State of California, If you have a month-to-month (or shorter) periodic rental agreement, the landlord must give you at least 30 days advance written notice of a rent increase.The landlord must give you at least 30 days advance notice if the rent increase is 10 percent (or less) of the rent charged at any time during the 12 months before the rent increase takes effect.The landlord must give you at least 60 days advance notice if the rent increase is greater than 10 percent of the rent charged at any time during the 12 months before the rent increase takes effect. Last note from Lawyer Cat: If youre raising rent because your tenant filed a complaint against you or are raising rents for any reason that looks retaliatory, STOP! Rent retaliation is illegal. Stop being a slumlord, and be a true landlord. Thanks, Lawyer Cat. Now back to my story. Communicating the Rent Increase If youre lowering rent, the message is usually well-received by the tenant. If youre raising your tenants rent, its a different story. Even if you invoke the rhetorical power of Johnny Cochran via each keystroke on your laptop, it wont change the fact youre taking money out of your residents pocket. Now this isnt something you should feel guilty about because, if you manage a quality property, you deserve to be well-compensated for your work. While I cant tell you how to perfectly construct this message, I can tell you a few dos and donts: Do:Communicate clearly and succinctly.Feel free to express your appreciation for their stay at your property.State the new rent amount and when the new rent changes will take effect.Dont:Make your rent increase letter/email as long as War And Peace.Communicate the increase in person. Sending the increase via email or letter allows the tenant to digest the information before responding. Apologize for increasing the rent. If you were truly sorry, you wouldnt raise it in the first place.Oh, no! My Tenant Has Decided to Leave. Now What? First of all, dont panic! Confirm the reason why the tenant is leaving. If its related to your rent increase, try to negotiate with them. Points of NegotiationGradually phase in the rent increase or minimize the rent increase for a longer lease agreement.If requested by the tenant, consider adding an amenity (air conditioning, garbage disposal, etc.). So long as the amenity provides a reasonable return on investment, consider making the investment in order to keep the tenant and secure the rent increase.Rent Escalation Clauses A rent escalation clause is a provision included in the lease agreement allowing the landlord to increase the rent to a pre-arranged rate based upon a fixed percentage or the consumer price index (CPI). Typically rent escalation clauses are used for multi year commercial lease agreements. Most rental properties dont include a rental escalation clauses in their month to month or year long leases If its a multi-year lease, you can consider pegging the increase to the consumer price index CPI for your area. The rent escalation clause serves two purposes: If the tenant lives in a expensive real estate market, the escalation clause provides the tenant with assurance their rent wont increase more than the prearranged escalation rate. The manager knows they can avoid the difficult rent increase conversation and their rents will increase with inflation.Conclusion The decision to raise your rents cant be based off of just one factor. You need to break the decision down into a series of parts to make sure youre considering all aspects that are influencing your final decision. The process towards making the final decision to increase rents should incorporate the following: Your goalsRelationship with the tenantCost of vacancyHealth of the economy Market rentsComparable propertiesState, county, and city rental lawsHow to communicate the increasePotential rent negotiations Finally, keep in mind that you are taking a calculated risk by raising the rents: trying to get the most rent from your property at the risk of losing a good tenant (and spending time or losing money to replace that tenant). Were republishing this article to help out our newer readers. Do you have any tips for raising rents? Or do you have any questions? Leave your comments below to discuss! https://www.biggerpockets.com/renewsblog/2016/03/17/raising-rent-ultimate-guide/ How many people remember the importance of prerequisites in college?

I can recall being super excited to register for a few classes, and when I was filling out the last page of registration, it denied my paperwork since I did not have the correct prerequisite class. Of course, being young and naive, I thought thisrule of needing prerequisites was stupid and unnecessary! However, as Ive gotten older, I have come to appreciate the need for prerequisites. The purpose of prerequisites is to actually set people up for success. So why am I talking about prerequisites on a real estate investing blog? Well, I am excited to be writing about a very important and popular topic in real estate investingprivate money. I am going to talk about the prerequisites that investors need BEFORE they can begin raising private money. Too many real estate investors simply find a deal and then go on the hunt for a private money partner. I see various forums and posts about this topic all over BiggerPockets. I dont want to say this is a bad strategy; however, there are some critical must have prerequisites before you can begin looking for private money partners and discussing deals with them. Some people might disagree with me and say, Just fake it until you make it or Act as if. Related: The Definitive Guide to Finding Private Money Lenders in Your Network Well, I am all about positive thinking. However, if you are trying to build trust and rapport with private money lenders, you dont want to fake it til you make it. Not with them. In order to increase your success rate with private money lenders, you must have some critical prerequisites.  4 Must Haves BEFOREYou Go On the Search for Private Money1. Gain real estate investing experience. If you decided to invest in the stock market, I would assume you would not feel comfortable handing over your money to a financial planner who has no experience. Well, that being said, this is exactly what happens when potential real estate investors seek private money when they dont have any education or experience under their belt. Let me explain. You and I agree that you must be educated. I am not telling you anything you dont already know. This point has been made time and time again all over the BiggerPockets site. And rightfully so. However, many people underestimate this step and take it for granted. They think learning a few real estate terms like after repair value and debt coverage ratio and taking a few courses equips themto look for deals and to begin raising private money. I would recommend taking it a step further. In addition to getting yourself educated, I would highly recommend gaining real life real estate experience. Get as much experience you can in an actual real estate deal (from the time an offer is made to the time the property is sold or rented). This is the best way to learn the business. This will help you learn the basics of real estate. Attend as many educational opportunities as you can. The key is to learn from people who you respect and want to eventually emulate. When my husband Matt and I got started, we took an entire year to become educated. We attended countless local real estate meetings and took as many courses as we could on the subject of real estate investing. We also gained some real estate investing experience by spending time with a knowledgeable, handy realtor who, in addition to selling properties, also had some investment properties of his own. We learned a lot from him. When we moved from Philadelphia, however, we should have found a mentor in our new home of NJ. We could have continued to gain experience that way. That was a mistake. That is why I am so adamant to newbies to figure out how to gain experience. That way, when you are speaking with a potential private money lender, you can speak about real estate investing in an educated way. You are not trying to impress people with the big terms you know; instead, show them that you know what you are talking aboutand have the team and experience to back it up. 2. Become an ACTIVE part of two types of networks. This one also might seem obvious since you are reading this blog on the BiggerPockets site! However, I dont mean getting involved on the peripheral; I mean really getting involved and becoming an active member of the network. In order to become really involved in a community, you must become a resource and someone willing to help. No one likes the person who attends networking (online or in person) and just takes information and never provides information or helps. Become active in real estate communitiesboth online and in person. Clearly, I am a huge fan of the BiggerPockets community. It is a phenomenal site and community. Honestly, there is nothing out there like it. I also encourage experienced and novice investors to get involved in local real estate investing clubs. Volunteer in these groups, take experienced investors out to coffee, offer to help where you can. There is always help that is needed. Bottom linebe a resource, soak as much as you can up, and surround yourself in the real estate conversation.Become active in non-real estate communities. This is also important to expanding your network and business contacts. Both my husband and I have been involved with various networking groups, referrals groups and business groups (and continue to participate). There are many benefits to these groups, including the abilityto expand your business contacts and network. Most recently, a member of my referral group recommended the bank we ended up refinancing our portfolio with! The worst thing you can do is just surround yourself with other real estate investors. Expand your network, and you will expand your experience. The one caveat I must say: please be aware of protecting your time. Once you begin to volunteer and let these organizations know you are willing to help out, they may suck you in and never let you go! I am part kidding and part serious. Be smart about your volunteering. Make sure you are helping the organization and that it is a role and position that will help you out. Just be careful. Time, as we all know, is the one limited resource.  3. Take a personal inventory (time, assets, skills, personality, why). I have mentioned this in various blog posts; however, this is an important one BEFORE developing partnerships and looking for private money. When I say take a personal inventory, I mean take a look at what you bring to the table first. Time:Become clear on how much time you can put towards real estate investing. Many of our private money partners and investors like the fact that we are full time real estate investors. We are always there if they have a question or even want to walk a property. I am not saying you have to be full time; however, you need to be clear with yourself and your potential money partners regarding the time you do have to put into your real estate investing business. Money:If you are looking for private money, many potential partners will want to know if you are going to put in money (i.e. if you are going to have some skin in the game). Some real estate investors will tell you that they dont put any of their own money into a deal, and other investors will tell you that they do put in money along with the money partner. Regardless, the key is to be clear on your personal financial position. What personal resources do you have the potential to use? Dont let the answer to this question stop you. You can be successful whether you have money to invest or not. Once you have an answer for this, you then will need to establish how much private money you are looking for. One of the best things we have done with most of our private money deals is to use private money to purchase and rehab the building (either for buy-hold or buy-flip). In other words, this has allowed us to do cash deals and then refinance once the project is complete (sold or rented). The deal moves faster this way, which makes everyone happy. Skills:What are your strengths? Every single person reading this blog, on the BP site and in this world has skills and personality strengths. Each of us is great even excellent at something. The key is to identify your strengths and then figure out how to translate these skills and strengths to the real estate investing world. Most, if not all, skills are transferable. Then determine your gaps (i.e. skills that you need that you dont possess). You can deal with these gaps by developing a team, developing partnerships, or even learning the skill through mentoring and surrounding yourself in the real estate conversation. Your Why:This one is fairly simple and straightforward. Become crystal clear (and honest) with the reasons and motivation you are investing in real estate. Make it deeper than simply making money. Every private money lender needs to trust their investor. Related: 3 Important Things to Consider When Raising Private Money for Your Deals Today You build trust by sharing your goals and reasons for getting into real estate investing with people. Bottom line be authentic. 4. Develop your strategy (market, property, financing, team). Before you can look for private money partners, I would suggest developing your investing strategy. Begin to gain clarity around the market you want to invest in and the type of deals you want to do (i.e. buy-hold, buy-rehab-hold, turn-key, wholesale, buy-fix-flip, etc). You also want to gain some relationships with financing partners. Even if you partner with private money lenders, you will need to have relationships with conventional lending institutions, such as banks, credit unions, etc. Lastly, begin to develop your team. It helps to have key people on your team (contractors, title agent, realtor, attorney, and accountant). If you take action from Step #2 above, you should have no problem building a team. Final Thoughts The only reason we have been able to grow from 30 units to over 100 units in a 3-year timeframe is due to raising private money. This has been the key to our growth. Before you begin to raise private money, my hope for you is that you take action on these four steps. Were republishing this article to help out our newer readers.  Are there any steps you would add? Or do you disagree with me and suggest you fake it til you make it? I would love to hear how you applied any of these suggestions! https://www.biggerpockets.com/renewsblog/2014/10/17/4-essential-steps-to-take-before-seeking-private-money/ Building a real estate business can be one of the best ways to achieve financial freedom. The problem for most, however, is money: There simply isnt enough in your hands to get all the deals you want. Thats why todays show might be the most impactful podcast episode youve ever heard. In todays interview with Matt Faircloth, author of the new book Raising Private Capital, shares the steps needed to begin raising money from others to fund your real estate deals. Youll discover the different types of private capital (and how to approach each), how Matt and his wife were able to grow from 30 units to over 300 (!) using other peoples money, and why talking about metrics to a private lender might not be a great idea at first. If you want to 10x your real estate portfolio or build your empire faster, this is one show you cant afford to miss!

Click hereto listen on iTunes. Listen to the Podcast HerePodcast: Play in new window | Download Subscribe: Apple Podcasts | Android | RSS Watch the Podcast Here [embedded content] Help Us Out! Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it! Fire RoundSponsor  Check out SimpliSafe Securitys DIY home security systems; an affordable, wireless, cellular, and customizable system that doesnt require a contract! Check out SimpliSafe Securitys DIY home security systems; an affordable, wireless, cellular, and customizable system that doesnt require a contract!Try it today with a discount:simplisafepockets.com In This Episode We Cover:Who Matt Faircloth isHow theyve reached 380 units to dateTips for building wealth by investing in businessWhat you should know about opportunity costFinding deals versus making good dealsHow to raise private moneyTips for starting a business with friends and familyA role-play call with DavidThe number one question potential cash providers askWhy you should start with debtA new way to look at debtWhen the SEC gets involvedAbout his bookAnd SO much more! Links from the ShowBooks Mentioned in this ShowFire Round QuestionsTweetable Topics:When it comes to raising money, you got to establish trust first. (Tweet This!)People should start with debt. (Tweet This!)Its not about finding good deals, its about making good deals. (Tweet This!)Youve got to squeeze the lemon and make something out of it. (Tweet This!)Connect with Matt https://www.biggerpockets.com/renewsblog/biggerpockets-podcast-289-other-peoples-money-build-real-estate-empire-matt-faircloth/ Without a doubt, everyone has heard that real estate is all about location, location, location. Ive bought in every class of real estate. Ive bought A-class condos that I flipped, and Ive bought D-class homes that Im stuck with to this day. Ive made money in every class.

Even though Ive made money in every class of properties, I will no longer buy D-class properties. I will no longer buy properties based on price alone. This isnt a new rule for me, but every now and again, I get reminders of why I have this rule. Criminal Records, Evictions & Low Credit Scores, Oh My Most recently, the reminder has been a vacancy. We had a tenant move out end of October in one of the few properties I still own in a D-class neighborhood. The property was left in decent shape. We needed to go in, clean it up and paint it. It was a very minor turnover. The unit went back on the market five days later. We got some leads on the property and some applications, but they were terrible. Criminal records, evictions, extremely low credit scores you name it, and it was probably on one of the applications. So the property continued to sit on the market. The cost of getting a bad tenant is much higher than the cost to let the property sit, so it continues to sit until we can find the right tenant.  This isnt uncommon for these few properties that I have. Tenant moves in, stays for a couple years, then moves out, and it takes me a couple months to fill it. The vacancy rate of property management companies and individual properties can be very different, especially if the properties are spread over different classes. Related: Class A, B, C & D Real Estate: How to Know Where YOU Should Invest For instance, our vacancy rate has been sub 3% for a number of years. Our turnovers each year have been minimal. But this handful of properties always has high vacancy rates, and the economic cost has always been high. Thats why it is important to ensure that you understand the difference of vacancies in certain neighborhoods. D-Class Properties Require Twice the Management Work Vacancy is just one of the issues we deal with in these D-class properties. They also require a different level of management. I dont have hard data to back this up, but I would venture to say D-class properties require almost twice the work as compared to other properties. D-class tenants tend to be high maintenance, and that high maintenance comes at a cost. So, if you are buying a D-class property and have a property manager, dont be surprised if your returns are not as good as you thought they would be. I can still make money on D-class properties because I have everything in-house. I have my own leasing agents. I have my own maintenance crew. I have my own property manager. So, my expenses are not the same as someone elses property who is managing everything on his/her own. Too many people make a decision about buying property solely on the price level and the rents. Most of them dont realize until it is too late that the expected returns arent going to be there.  Related: Newbie Investors: Heres the Truth You NEED to Know About $30k Properties Why Id Still Buy Them Apart from all this, I would still like to buy D-class properties in comparison to non-performing notes. Sure, you can make a lot of money out of it, but youll need the help of a professional and experienced team to do that. The risks need to be spread over a large portfolio. But if you are planning to do everything on your own or buying your first investment property, dont get caught up in the low price point properties. The headaches are not going to be worth the returns that you get. Were republishing this article to help out our newer readers. Have you bought any D-class properties? Would you like to share your experiences? Let me know with a comment! https://www.biggerpockets.com/renewsblog/2016/01/16/newbies-dont-buy-d-class-investment-properties/ Personal finance nerds (like myself) spend an inordinate amount of time thinking about retirement.

How much do you need? How can you ensure that you dont run out of money in retirement? Whats the fastest way to get there, and does fast also mean safe? For the last 20 years, the 4% rule (a.k.a. the 25X rule) has been something of an industry standard. At the very least, its been a shorthand to use as a reference point. But for all its simplicity, how true is it? Does it leave room for shortcuts? Is it even still relevant in todays economic environment? And where do rentals fit in? But were getting ahead of ourselves. Lets start at the beginning. How Did the 4% Rule Come About? Back in the 90s, financial advisor Bill Bengen introduced the idea of the 4% rule. Its simple enough: A retiree can afford to withdraw about 4% of their nest egg each year, if they want it to last them 30 years. Bengen proposed this rule after analyzing historical stock and bond market returns and found a 4% withdrawal rate to be safe for retirees. On the simplest level, it makes sense. If your stock portfolio rises in value by an historically-reasonable 7%, and you subtract out 2% of that for inflation, that leaves a real return of 5%. You take 4%, and voila! Your stock portfolios value actually rose by 1% over the course of the year, even though you sold off some of it. The other way of thinking about this rule is by its other name, the 25X rule. It dictates that investors will need a nest egg of 25 times their annual spending if they want to live on 4% of it each year. Thus, if you want to withdraw $40,000/year as income, youll need a $1,000,000 nest egg.  How Does the 4% Rule Hold up in Todays World? First, consider the simplest problem at all: What if you live for more than 30 years after retiring? Americans who reach 60 can expect to live into their 80sand increasingly live into their 90s or even become centenarians. So, this 30-year timeline may not leave every 60-year-old jumping for joy. Related: 7 Achievable Steps to Reach 7-Figure Retirement Savings And hang on a seconddoes it even guarantee you 30 years of income? Of course not. Aside from the possibility that you invested money in the next Enron, the market could crash right after you retire. One T. Rowe Price study found that, moving forward, theres 90% probability that retirees following the 4% rule wont run out of money in 30 years. This means that a troubling 10% of the time, retirees could expect to run out of money. Bonds, interest rates, market crashes, oh my! Some of your retirement portfolio is probably made up of bonds, not stocks. And in the 90s, when Bengen proposed this rule, interest rates were high and bonds paid well. In a low-interest environment (like weve seen in this century), investors cant expect much in the way of returns from them. They also have a fixed lifespan and run out eventually. Still, retirees often still rely on them because of their greater reliability over stocks. That T. Rowe Price study above was based on a 60% stocks/40% bonds allocation, just like Bengens original proposed rule allocation. But not everyone uses this asset allocation. What if you retire with half of your portfolio in stocks and half in bonds? A Vanguard study found that over 35 years, the rule only worked 71% of the time under these conditions. Heres the other big risk with the 4% rule: what if the market crashes right after you retire? If youre only pulling money out when a market crashes and not putting any money back in, then its all downside for you. You lose money on the crash, but dont make any money by investing in the recovery. Sure, the market will eventually recover, but between now and then, you will have had to draw down significantly on your balance. When the recovery comes, your remaining portfolio will be much smaller, leaving less to regain lost ground with. For all that, financial planner Michael Kitces points out that over the last 150 years, there has not been a 30-year period when someone following the 4% rule would have run out of money. The Wild Card: How Rentals Change the Math Heres where things get interesting. What happens when rentals enter the mix? In our earlier example, we decided we wanted $40,000 in income post-retirement in addition to Social Security, which would mean a $1,000,000 nest egg. That comes to $3,333/month. Our imaginary friend Michelle invests $250,000 in a fourplex that rents for $3,600/month. After expenses, lets say she earns $1,800/month on it. Now she only needs another $1,533/month, or $18,396/year, from her stock portfolio. That means a nest egg of $459,900. See what happened there? Michelles total sum needed just dropped from $1,000,000 to $709,900 ($250,000 for the fourplex, $459,900 for stocks). She just trimmed nearly $300,000 off her total necessary assets!  The Balance Between Rentals and Stocks Sometimes stock markets crash. Sometimes rental properties hit their owners with several expenses at once. But thats the beauty of diversificationthose two events almost always remain unrelated. During the Great Recession, U.S. stocks crashed by around 30%, and real estate values dropped similarly. But rents did not drop. Why? Because so many homeowners became renters that the demand for rental housing actually increased. Smart landlords set aside money for repairs, vacancy rate, CapEx, etc. into a property fund each month, so that when a turnover or a $5,000 roof bill comes along, theyre prepared for it. But imagine that several turnovers and a huge roof bill happen to come along all at once. A retiree can draw a little extra from their stock portfolio that month to cover the difference. Related: Want to Retire Early? Sorry, But Much of Your Net Worth May Not Help When landlords see strong performance from their rentals, they can always invest extra in their stock portfolios. Likewise, when their stock portfolio is suffering, landlords might postpone a property upgrade theyd been considering and lean more heavily on their rental income. And theres that little matter of inflation; rents rise alongside (or surpass) inflation. That makes rentals an excellent hedge against it. Diversification is a beautiful thing. The Exponential Impact of Spending Consider this side of the 25X rule: It highlights just how costly each extra dollar of spending is for your bottom line. For every $100/month that you spend, youll need an extra $30,000 in your nest egg, according to the 25X rule. Seriously, $100/month is $1,200/year, which multiplied by 25 is $30,000. Is your cable bill really worth having to invest another $30,000? What about that latte habit? At the risk of sounding like a nag, if you cut that spending now, you can invest it and reach your nest egg goals much, much faster. For a tough (but rewarding!) challenge, try living on half your income and investing the rest. Eyes on the Prize: Financial Independence For me, the point of investing is clear and simple: replacing active income with passive income. On the day when my passive income can cover my expenses, Ill reach financial independence, and every day that I work thereafter will be a choice. Any discussion of withdrawal rates (e.g. the 4% rule) rests on an underlying fear. At its heart, the discussion revolves around how much of my portfolio can I sell in a given year, with a reasonably low risk of running out of money? I dont want to worry about running out of money. I want my portfolio to keep growing even after I retire. And to do that, all I must do is focus on building passive income. Rental properties, stock dividends, and bonds all offer it. You can still sell off stocks in retirement, of course. Selling off 2%, 3%, even 4% will almost certainly leave you in fine shape. But if you can keep that number under 3-4%, and replace a healthy chunk of your monthly income with rents instead, your nest egg will almost certainly grow rather than shrink. Were republishing this article to help out our newer readers. How is your retirement investing coming along? What tips do you have to get there even faster? Leave your thoughts and questions below! https://www.biggerpockets.com/renewsblog/4-percent-retirement-rule Buying a car is a big investment, and if youre living on a budget, you cant afford to make mistakes. Thats why, before you head to the dealership, you need to do your homeworkbecause theres nothing straightforward about buying a car. Car salesmen are masters of the up-sell, and if you dont know what youre doing, youll walk out of there with a dozen add-ons you never meant to buy. You need to arrive with the tools in hand to outsmart the dealers.

These four simple steps will give you a clear sense of what kind of car youre looking for and how much you can spend, and most importantly, theyre designed to give you the upper hand in negotiations. 4 Steps to Buy the Car You Want Within the Budget You Can Afford1. Calculate your costs. The most important data point to establish before seeking to buy a car is how much money you can afford to spend. That means accounting for monthly payments, but also setting aside the funds for a down payment. Youll also want to make sure you have a few months of loan payments set aside in case an emergency strikes because its going to take you a while to pay down your loan; todays average loan is 5.5 years, but many run for 6 or 7 years because base prices on new cars are so high. Related: 5 Advanced Excel Tips for a Better Home Budget In addition to budgeting for car payments, youll also need to account for the cost of insurance, license and registration, and upkeep. These finer details tend to be where first-time buyers slip upthe expenses pile up quickly, and they tend to be front-loaded in the period immediately around the date of purchase. Other costs like taxes that arent included in the ticket price can also throw your initial calculations off, so be sure you know exactly whats going to show up on your bill before you start looking at vehicles.  2. Get your loan. Once you know how much money you can spend on a car, the next step is to get a loanand just like car salesmen, many loan providers will push you up against the limits of what you can afford. Dont let them. Stick to the number youve calculated because when youre approved for more, youll feel obligated to spend it. Its important to get pre-approved for your loan because it gives you control over the negotiation process. If theres a vehicle just out of your price range, salesmen are more likely to try to meet it with a special offer or discount because they know you arent going to spend more just because they put pressure on you. Another advantage to getting pre-approved for a car loan is that it gives you the time to shop around for loans and find the best interest rate. Just because you know how much you can afford doesnt mean every lender will offer it to you the same way. For example, your bank may give you a better interest rate because youre a loyal customer, or another lender may be having a special promotion. You have to compare all the options to minimize extra costs. 3. Research best buying dates. Over the course of the year, there are many major car salesMemorial Day, 4th of July, even New Years day. But when is the best time to buy? This is a surprisingly complex question, but there are plenty of resources that can guide you. If youre thinking across the span of an entire year, many experts say New Years day is the best day to buy. Thats because no one is trying to meet any quotas; its a fresh slate for the dealers and a great opportunity for you. Plus, most dealerships are still trying to clear last years models from the lot, so there will be plenty of great sales happening. Of course, when your decade-old vehicle breaks down in April or youre in need of your first car, you probably arent in a position to wait around until New Years day to snag the best price. Dont worry, because there are plenty of other great days to buy. Almost any holiday sale will allow you to snag a good deal, and on a week-to-week basis, Mondays generally show the greatest price drop. Like anything else, though, you need to research pricing in your area and check additional resources for the best upcoming sales dates.  Related: The Two Best Budget-Building Apps, Compared and Contrasted 4. Focus on function. Finally, as you try to narrow down your options, its time to figure out what features you need in your new car, and that means thinking about its function in your day-to-day life. For example, if youre going to drive for a rideshare to make money, there are generally specific rules you have to follow to qualify, like having a car thats a 2007 model year or newer. Or, if you live in a cold or rugged area, youll need a car with four-wheel drive that can handle challenging roads. Depending on your budget, you may also have a chance to consider what features you want but dont necessarily need. If you have kids, you might want in-car entertainment options or a particular sound system, but you dont need one. Maybe you camp and want a trunk that can handle a lot of equipment. As you plan, you can narrow down the list of models to ones that fit your criteria. When you dont know what you can afford and dont have a plan, its easy to be taken advantage of at your local car dealershipbut youre not going to be their next mark. Now, by following these rules, youre going to be a savvy buyer who gets what you want at the price you want. Have you ever landed a great car deal? Any tips youd add to this list? Comment below! https://www.biggerpockets.com/renewsblog/buy-a-car-within-budget When talking to new private money partners, investors often jump in too quickly and talk about the actual deal they are raising private money for. They talk about the location, the market, where they got the deal, the numbers, and of course, the potential return the private money partner could make if they invest in the deal.

Related:How I Find Private Money Lenders to 100% Fund My Deals (& How You Can, Too) Yes, private money partners do care about the deal and the returns they are going to make. However, this is not the first thing they care about. 5 Things Private Money Partners Care About [embedded content] When presenting and talking to new private money partners, you have to put yourself in their shoes. You have to think about their perspective first. What do they care about? What is important to them? If you want to build long-term relationships in this business, you have to first consider the perspective of the private money partner (verse simply focusing on your own goals and what is important to you). Related:Investors: Dont Be Intimidated by Private Money! Heres What You Need to Know In todays video, I teach that about the details new private money partners care about most: TrustProtectionUse of moneyReturn of capitalThe deal Thanks, as always, for watching my videos! Check out my new book on raising private money (published by BiggerPockets) that is available for pre-order now! What have you found to be areas new private money partners care about? Please comment below! https://www.biggerpockets.com/renewsblog/what-a-private-money-partner-really-cares-about/ Do you remember Elvis? Do you remember all of the excitement and craziness that surrounded this cultural icon at his sold out concerts all over the country? I do. Well, sort of. I have a vague memory of watching lots of old Elvis movies at my grandmothers house as a kid.